You might also like

- Lecture 3 - InterestRatesForwardsDocument10 pagesLecture 3 - InterestRatesForwardsscribdnewidNo ratings yet

- DRM-CLASSWORK - 11th JuneDocument2 pagesDRM-CLASSWORK - 11th JuneSaransh MishraNo ratings yet

- Term Structure of Interest Rates: For 9.220, Term 1, 2002/03 02 - Lecture7Document20 pagesTerm Structure of Interest Rates: For 9.220, Term 1, 2002/03 02 - Lecture7tiamojuanNo ratings yet

- EFB344 Lecture07, FRAs and SwapsDocument35 pagesEFB344 Lecture07, FRAs and SwapsTibet LoveNo ratings yet

- FM Ch-3 Time Value of MoneyDocument40 pagesFM Ch-3 Time Value of MoneyMifta ShemsuNo ratings yet

- Para Sa Mga Anak NG DiyosDocument26 pagesPara Sa Mga Anak NG DiyosJohn Michael M. Montarde0% (1)

- Bonds ValuationsDocument57 pagesBonds ValuationsarmailgmNo ratings yet

- L5 - Farm Investment AnalysisDocument57 pagesL5 - Farm Investment Analysischampikadeshappriya152No ratings yet

- Forward Rate Agreements 517Document10 pagesForward Rate Agreements 517stannis69420No ratings yet

- Interest Rate DerivativesDocument58 pagesInterest Rate DerivativesIndia Forex100% (2)

- Basics of Bond Valuation: Government Securities (G-SEC, or GS) / Treasury BondsDocument39 pagesBasics of Bond Valuation: Government Securities (G-SEC, or GS) / Treasury BondsVrinda GargNo ratings yet

- CCRA Session 6Document17 pagesCCRA Session 6Amit GuptaNo ratings yet

- Forward Rate AgreementDocument17 pagesForward Rate AgreementSumit SharmaNo ratings yet

- Test Your Knowledge: 2.2.4.2 Pricing of SwaptionsDocument11 pagesTest Your Knowledge: 2.2.4.2 Pricing of SwaptionsRITZ BROWNNo ratings yet

- 2 Forward Rate AgreementDocument8 pages2 Forward Rate AgreementRicha Gupta100% (1)

- International Financial Management PgapteDocument30 pagesInternational Financial Management Pgapterameshmba100% (1)

- Bootstrapping Spot RateDocument37 pagesBootstrapping Spot Ratevirgoss8100% (1)

- Duration of BondDocument9 pagesDuration of BondUbaid DarNo ratings yet

- Time Value of MoneyDocument5 pagesTime Value of Moneysmwanginet7No ratings yet

- Chapter 3Document19 pagesChapter 3GODNo ratings yet

- Module II Capital BudgetingDocument43 pagesModule II Capital BudgetingSrinibashNo ratings yet

- Business Finance 7Document25 pagesBusiness Finance 7Trisha ElecerioNo ratings yet

- What Are FMPS??: Fixed Maturity Plans (FMPS) Are Back in VogueDocument2 pagesWhat Are FMPS??: Fixed Maturity Plans (FMPS) Are Back in VogueShravan KumarNo ratings yet

- Forward & Futures PricingDocument41 pagesForward & Futures Pricingasifanis100% (3)

- The Structure of Interest RatesDocument72 pagesThe Structure of Interest RatesMarwa HassanNo ratings yet

- Forward and Futures ContractsDocument55 pagesForward and Futures Contractsben tenNo ratings yet

- SM 714 ME The Time Value of MoneyDocument39 pagesSM 714 ME The Time Value of MoneyAnushka DasNo ratings yet

- DHA-BHI-404 - Unit4 - Time Value of MoneyDocument17 pagesDHA-BHI-404 - Unit4 - Time Value of MoneyFë LïçïäNo ratings yet

- Module 7. Annuities: 1. Simple AnnuityDocument19 pagesModule 7. Annuities: 1. Simple AnnuityMori OugaiNo ratings yet

- Term Structure of Interest RatesDocument21 pagesTerm Structure of Interest RatestoabhishekpalNo ratings yet

- Interest Rates Chapter: Key ConceptsDocument6 pagesInterest Rates Chapter: Key ConceptsAn HoàiNo ratings yet

- Determinants of Interest Rates (Revilla & Sanchez)Document12 pagesDeterminants of Interest Rates (Revilla & Sanchez)Kearn CercadoNo ratings yet

- Interest Rate Risk I (CH 8)Document13 pagesInterest Rate Risk I (CH 8)Mahbub TalukderNo ratings yet

- Ch5 Interest RatesDocument25 pagesCh5 Interest Rateszey9991No ratings yet

- Project Financial Analysis StepsDocument42 pagesProject Financial Analysis StepsAsnake MekonnenNo ratings yet

- Mathematics of FinanceDocument25 pagesMathematics of FinanceJulianna CortezNo ratings yet

- Accounting and Audit for Financial Sector - Understanding Bank Interest and its CalculationsDocument19 pagesAccounting and Audit for Financial Sector - Understanding Bank Interest and its CalculationsTanay ShahNo ratings yet

- Financial Management: Lecture#11Document21 pagesFinancial Management: Lecture#11SULEMAN BUTTNo ratings yet

- TVM Concepts ExplainedDocument15 pagesTVM Concepts ExplainedIstiaque AhmedNo ratings yet

- FINC4101 Term Structure AnalysisDocument28 pagesFINC4101 Term Structure AnalysisAjeet YadavNo ratings yet

- Long Term Debt and Preferred Stock Financing ExplainedDocument8 pagesLong Term Debt and Preferred Stock Financing ExplainedSuvash KhanalNo ratings yet

- Fixed Maturity Plans (FMP) : Retail ResearchDocument2 pagesFixed Maturity Plans (FMP) : Retail Researcharun_algoNo ratings yet

- Interest Rates and Bond Valuation: All Rights ReservedDocument28 pagesInterest Rates and Bond Valuation: All Rights ReservedFahad ChowdhuryNo ratings yet

- TVM Seminar 3 NotesDocument34 pagesTVM Seminar 3 Notes朱艺璇No ratings yet

- Interest Rate FutureDocument19 pagesInterest Rate FutureDivyesh GandhiNo ratings yet

- 4 - Term Structures TheoriesDocument15 pages4 - Term Structures Theoriesmajmmallikarachchi.mallikarachchiNo ratings yet

- Chapter 3 FMDocument79 pagesChapter 3 FMHananNo ratings yet

- Topic 4 Mathematics of FinanceDocument66 pagesTopic 4 Mathematics of FinanceAndrew PillayNo ratings yet

- Valuation of Bonds and SharesDocument21 pagesValuation of Bonds and ShareszlnpjbcckbeqwnzgojNo ratings yet

- GENERAL MATHDocument7 pagesGENERAL MATHAleah TulauanNo ratings yet

- NPVDocument7 pagesNPVJowelYabotNo ratings yet

- Chapter 5: Interest Rate Risks: Lecturer: Amadeus GABRIEL La Rochelle Business SchoolDocument25 pagesChapter 5: Interest Rate Risks: Lecturer: Amadeus GABRIEL La Rochelle Business SchoolJuana BoresNo ratings yet

- Time Value of Money - Part1Document28 pagesTime Value of Money - Part1Alex JavierNo ratings yet

- Understanding the Term Structure of Interest Rates and DurationDocument31 pagesUnderstanding the Term Structure of Interest Rates and DurationBraulio GarayNo ratings yet

- 03 How To Calculate Present Values-2Document23 pages03 How To Calculate Present Values-2melekkbass10No ratings yet

- Interest Rate Models and Derivatives 2019Document69 pagesInterest Rate Models and Derivatives 2019Elisha MakoniNo ratings yet

- 5 Simple Interest and DiscountDocument69 pages5 Simple Interest and DiscountJUSTIN HECTOR BRENT SAJULGANo ratings yet

- Rowe Lawler CookeDocument10 pagesRowe Lawler CookeDesi DiPierroNo ratings yet

- Derivatives and Risk Management: Session 1 - Introduction Prof. Aparna BhatDocument22 pagesDerivatives and Risk Management: Session 1 - Introduction Prof. Aparna BhatMayankSharmaNo ratings yet

- Forward Rate Agreements: Session 3 - Derivatives & Risk MGTDocument15 pagesForward Rate Agreements: Session 3 - Derivatives & Risk MGTMayankSharmaNo ratings yet

- Swaps: Derivatives & Risk ManagementDocument17 pagesSwaps: Derivatives & Risk ManagementMayankSharmaNo ratings yet

- Forward Rate Agreements: Session 3 - Derivatives & Risk MGTDocument15 pagesForward Rate Agreements: Session 3 - Derivatives & Risk MGTMayankSharmaNo ratings yet

- Derivatives Risk ManagementDocument61 pagesDerivatives Risk ManagementMayankSharmaNo ratings yet

- Derivatives Risk ManagementDocument61 pagesDerivatives Risk ManagementMayankSharmaNo ratings yet

- Swaps: Derivatives & Risk ManagementDocument17 pagesSwaps: Derivatives & Risk ManagementMayankSharmaNo ratings yet

- Forward Rate Agreements: Session 3 - Derivatives & Risk MGTDocument15 pagesForward Rate Agreements: Session 3 - Derivatives & Risk MGTMayankSharmaNo ratings yet

- Test FileDocument1 pageTest FileghanshyamNo ratings yet

- Guidelines 1702-EX June 2013Document4 pagesGuidelines 1702-EX June 2013Julio Gabriel AseronNo ratings yet

- PACER - Leber vs. Konigsberg - Konigsberg ResponseDocument9 pagesPACER - Leber vs. Konigsberg - Konigsberg Responsejpeppard100% (1)

- Single Index ModelDocument4 pagesSingle Index ModelNikita Mehta DesaiNo ratings yet

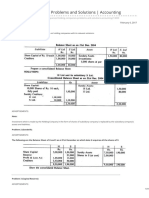

- Holding Companies Problems and Solutions AccountingDocument11 pagesHolding Companies Problems and Solutions AccountingGenarul IslamNo ratings yet

- Investing Options for Inherited MoneyDocument7 pagesInvesting Options for Inherited MoneyDaphne ManalastasNo ratings yet

- Basics of Share Market OperationsDocument8 pagesBasics of Share Market Operationslelesachin100% (2)

- Investment TrackerDocument12 pagesInvestment TrackerJoe VincentNo ratings yet

- Vol-6 CFD Trading Guide PDFDocument19 pagesVol-6 CFD Trading Guide PDFمحمد سفيان أفغوليNo ratings yet

- Guidelines For Foreign Exchange Transactions - Bangladesh BankDocument441 pagesGuidelines For Foreign Exchange Transactions - Bangladesh BankAshiq RayhanNo ratings yet

- Everett V Asia BankDocument2 pagesEverett V Asia BankEM RGNo ratings yet

- Analysis of Demat Account & Online Trading Karvy Stock Brocking Limited (M.Com Project)Document64 pagesAnalysis of Demat Account & Online Trading Karvy Stock Brocking Limited (M.Com Project)VRUKSHITNo ratings yet

- Russia M&ADocument48 pagesRussia M&Adshev86No ratings yet

- Commissioner of Internal Revenue v. Covanta Energy Philippine Holdings, Inc. DigestDocument3 pagesCommissioner of Internal Revenue v. Covanta Energy Philippine Holdings, Inc. DigestCharmila Siplon100% (1)

- Business Combinations - PPADocument83 pagesBusiness Combinations - PPAAna SerbanNo ratings yet

- Macroeconomic & Industry Fundamental AnalysisDocument27 pagesMacroeconomic & Industry Fundamental AnalysischarymvnNo ratings yet

- Financial Statement Analysis of Fauji Fertilizer Company FFC Vs Engro CorporationDocument6 pagesFinancial Statement Analysis of Fauji Fertilizer Company FFC Vs Engro Corporationqurban balochNo ratings yet

- Exercise A3 - AnswersDocument12 pagesExercise A3 - AnswersCorinne Kelly100% (1)

- Msci Indonesia Esg Leaders Index Usd GrossDocument3 pagesMsci Indonesia Esg Leaders Index Usd GrossputraNo ratings yet

- General Angel FundDocument8 pagesGeneral Angel FundinforumdocsNo ratings yet

- Motilal Oswal ProjectDocument54 pagesMotilal Oswal Projectmathibettu100% (2)

- Abhishek Tiwari (Stir)Document84 pagesAbhishek Tiwari (Stir)himanshu sethNo ratings yet

- Issue of SharesDocument11 pagesIssue of SharesRamesh KumarNo ratings yet

- Citi Bank Internship ReportDocument74 pagesCiti Bank Internship ReportMajid YaseenNo ratings yet

- Chapter 8Document37 pagesChapter 8AparnaPriomNo ratings yet

- Futures West 1998Document30 pagesFutures West 1998Muh Akbar ZNo ratings yet

- Company Name Company Stages Website Geographic LocationsDocument4 pagesCompany Name Company Stages Website Geographic LocationsPriyanshu BhattacharyaNo ratings yet

- MRAT Mustika Ratu Tbk Company Report and Share PriceDocument3 pagesMRAT Mustika Ratu Tbk Company Report and Share PriceFebrianty HasanahNo ratings yet

- CHAPTER 2.1 Strategic Financial ManagementDocument23 pagesCHAPTER 2.1 Strategic Financial ManagementKarl BarnuevoNo ratings yet

- Special Report - Gas Dispute NewDocument10 pagesSpecial Report - Gas Dispute NewInternational Business Times100% (1)