You might also like

- Bank Reconciliation StatementsDocument3 pagesBank Reconciliation StatementsPatrick Prem GomesNo ratings yet

- FABM2 Q1 Mod1 Statement-of-Financial-PositionDocument21 pagesFABM2 Q1 Mod1 Statement-of-Financial-PositionAestherielle MartinezNo ratings yet

- Interest-Bearing Notes ReceivableDocument2 pagesInterest-Bearing Notes Receivablewarsidi100% (1)

- Theories of EquityDocument1 pageTheories of EquityJavian Negrón100% (1)

- Business Finance: Mrs. Leah O. RualesDocument28 pagesBusiness Finance: Mrs. Leah O. RualesCleofe Sobiaco100% (1)

- Buss 203 Business FinanceDocument2 pagesBuss 203 Business FinanceTevin67% (3)

- GaapDocument18 pagesGaapsujan BhandariNo ratings yet

- Basic Finance - Credit Instruments P9Document29 pagesBasic Finance - Credit Instruments P9Raymart L. Maralit100% (1)

- Fiscal Policy MeaningDocument47 pagesFiscal Policy MeaningKapil YadavNo ratings yet

- Contra AccountsDocument6 pagesContra AccountsRaviSankarNo ratings yet

- Module 1 Statement of Financial PositionDocument4 pagesModule 1 Statement of Financial PositionWella LozadaNo ratings yet

- 03 Special Types of Customers of A Bank CasesDocument4 pages03 Special Types of Customers of A Bank CasesVikashKumarNo ratings yet

- Statement of Cash FlowDocument25 pagesStatement of Cash FlowKylie TarnateNo ratings yet

- A Short Review On Basic FinanceDocument4 pagesA Short Review On Basic FinanceJed AoananNo ratings yet

- Accruals and AdjustmentsDocument14 pagesAccruals and AdjustmentsNepal Bishal Shrestha100% (1)

- 1. Current Asset2. Current Asset 3. Noncurrent Asset4. Current Asset5. Noncurrent Asset6. Current AssetDocument19 pages1. Current Asset2. Current Asset 3. Noncurrent Asset4. Current Asset5. Noncurrent Asset6. Current AssetMylene SalvadorNo ratings yet

- Chapter 3 Adjusting The AccountsDocument19 pagesChapter 3 Adjusting The AccountsKabeer Khan100% (1)

- Chap 6 - Financial Statements With AdjustmentDocument24 pagesChap 6 - Financial Statements With AdjustmentEli Syahirah100% (1)

- APPENDIX 1 AC Budget Narrative Sample Template 2016Document5 pagesAPPENDIX 1 AC Budget Narrative Sample Template 2016ASQIRIBANo ratings yet

- Understand financial statements with income statement & balance sheetDocument19 pagesUnderstand financial statements with income statement & balance sheetJeff Lacasandile100% (2)

- Fundamentals of Accountancy, Business and Management 1Document10 pagesFundamentals of Accountancy, Business and Management 1atriaheisleyNo ratings yet

- Module 1C - ACCCOB2 - Conceptual Framework For Financial Reporting - FHVDocument56 pagesModule 1C - ACCCOB2 - Conceptual Framework For Financial Reporting - FHVCale Robert RascoNo ratings yet

- Elements of Financial StatementsDocument3 pagesElements of Financial StatementsMargNo ratings yet

- Fundamentals of Accountancy, Business and Management 1Document20 pagesFundamentals of Accountancy, Business and Management 1Gel MeNo ratings yet

- FAR 2 NotesDocument3 pagesFAR 2 NotesMARK RANIEL ANTAZONo ratings yet

- Fundamentals of Accounting I The Accounting EquationDocument10 pagesFundamentals of Accounting I The Accounting EquationericacadagoNo ratings yet

- 2 Income and Business Taxation Midterm Slides 1 To 41Document41 pages2 Income and Business Taxation Midterm Slides 1 To 41Pathy PenidNo ratings yet

- 03 20 WDocument1 page03 20 WSteven SandersonNo ratings yet

- Generally Accepted Accounting PrinciplesDocument12 pagesGenerally Accepted Accounting PrinciplesMARIA ANGELICA100% (1)

- Journal Entries ExamplesDocument9 pagesJournal Entries Examplesmoon_mohi50% (2)

- Analysis of Financial Statements Mix RatioDocument30 pagesAnalysis of Financial Statements Mix RatioBianca Angela Camayra QuiaNo ratings yet

- FSA 8e Ch07 SMDocument60 pagesFSA 8e Ch07 SMdesy nataNo ratings yet

- 04 Trade Accounts ReceivableDocument7 pages04 Trade Accounts Receivablesharielles /No ratings yet

- Book of Accounts WD ActivityDocument3 pagesBook of Accounts WD ActivityChristopher SelebioNo ratings yet

- Chapter 6 Terms and DatingsDocument26 pagesChapter 6 Terms and Datingshtagle0% (1)

- Financial StatementsDocument1 pageFinancial Statementsaashir chNo ratings yet

- Financial Statement PreparationDocument60 pagesFinancial Statement PreparationAngel Anne De JuanNo ratings yet

- The Financial Plan: Serjoe Orven Gutierrez - Mmed ReporterDocument41 pagesThe Financial Plan: Serjoe Orven Gutierrez - Mmed ReporterSerjoe GutierrezNo ratings yet

- Lesson 1 CFASDocument14 pagesLesson 1 CFASkenneth coronelNo ratings yet

- Bookkeeping Single Entry and Double EntryDocument4 pagesBookkeeping Single Entry and Double Entryvijjiji100% (1)

- Acct TutorDocument22 pagesAcct TutorKthln Mntlla100% (1)

- Financial Statements As A Management ToolDocument20 pagesFinancial Statements As A Management TooldavidimolaNo ratings yet

- Metrobank Loan RequirementsDocument2 pagesMetrobank Loan RequirementsKate BautistaNo ratings yet

- Accounting Fundamentals: The Accounting Equation and The Double-Entry SystemDocument70 pagesAccounting Fundamentals: The Accounting Equation and The Double-Entry SystemAllana Mier100% (1)

- Financial Statement AnalysisDocument33 pagesFinancial Statement AnalysisMelissa BattadNo ratings yet

- Analysis of C&F Store's Financial StatementsDocument1 pageAnalysis of C&F Store's Financial Statementsmarissa casareno almueteNo ratings yet

- Financial Leverage and Operating Leverage ExplainedDocument13 pagesFinancial Leverage and Operating Leverage ExplainedMohsin KhanNo ratings yet

- Global Finance With Electronic Banking - Prelim ExamDocument5 pagesGlobal Finance With Electronic Banking - Prelim ExamAlfonso Joel GonzalesNo ratings yet

- Accounting - Instructor-1Document154 pagesAccounting - Instructor-1karimhisham100% (1)

- Analyzing Transactions in Service BusinessesDocument8 pagesAnalyzing Transactions in Service BusinessesUnamadable UnleomarableNo ratings yet

- Bank Deposits Documents and Transactions GuideDocument20 pagesBank Deposits Documents and Transactions GuideAlyssa Nikki VersozaNo ratings yet

- Loan RestructuringDocument22 pagesLoan RestructuringNazmul H. PalashNo ratings yet

- FABM1 Lesson8-1 Five Major Accounts-LIABILITIESDocument13 pagesFABM1 Lesson8-1 Five Major Accounts-LIABILITIESWalter MataNo ratings yet

- Financial IntermediationDocument14 pagesFinancial IntermediationKimberly BastesNo ratings yet

- Non Current AssetsDocument8 pagesNon Current AssetsJennifer EdwardsNo ratings yet

- I Am Sharing 'UPDATED' With YouDocument258 pagesI Am Sharing 'UPDATED' With Youjessamae gundanNo ratings yet

- Investment Risk ManagementDocument20 pagesInvestment Risk Managementthink12345No ratings yet

- Accounting 2 - 4rd ModuleDocument4 pagesAccounting 2 - 4rd ModuleJessalyn Sarmiento TancioNo ratings yet

- Chapter 4Document4 pagesChapter 4mayhipolito01No ratings yet

- Chapter 4 (Ratio Analysis)Document20 pagesChapter 4 (Ratio Analysis)Brylle LeynesNo ratings yet

- Environmental Scanning: Swot and Pest AnalysisDocument13 pagesEnvironmental Scanning: Swot and Pest AnalysisBrylle LeynesNo ratings yet

- Chapter 3 (Financial Statement Ratio Analysis)Document11 pagesChapter 3 (Financial Statement Ratio Analysis)Brylle LeynesNo ratings yet

- Slide No. 3Document94 pagesSlide No. 3Clumpsy GuyNo ratings yet

- Chapter Three: Ethics and Social ResponsibilityDocument30 pagesChapter Three: Ethics and Social ResponsibilityBrylle LeynesNo ratings yet

- Personal Selling and Sales Management: Slide 20-2Document14 pagesPersonal Selling and Sales Management: Slide 20-2Brylle LeynesNo ratings yet

- International TradeDocument27 pagesInternational TradeBrylle Leynes100% (1)

- Chapter 1 Intro To Business FinanceDocument25 pagesChapter 1 Intro To Business FinanceBrylle LeynesNo ratings yet

- Sales Management ModuleDocument86 pagesSales Management ModuleBrylle Leynes100% (1)

- FDIC Module4Eng PPTDocument23 pagesFDIC Module4Eng PPTBrylle LeynesNo ratings yet

- Sales Management TechniquesDocument22 pagesSales Management TechniquesBrylle LeynesNo ratings yet

- Personal Selling and Sales Management: Slide 20-2Document14 pagesPersonal Selling and Sales Management: Slide 20-2Brylle LeynesNo ratings yet

- Chapter 3Document15 pagesChapter 3Brylle LeynesNo ratings yet

- GW App Econ Online Mar 1 2017Document59 pagesGW App Econ Online Mar 1 2017Leonelson CorralNo ratings yet

- Introduction To Economics: The Economic Problem Opportunity Cost Production Possibility FrontiersDocument8 pagesIntroduction To Economics: The Economic Problem Opportunity Cost Production Possibility FrontiersSaad AhmedNo ratings yet

- Chapter 1Document10 pagesChapter 1Brylle LeynesNo ratings yet

- Creating and Sustaining Customer Value Through Cross-Functional Team SellingDocument18 pagesCreating and Sustaining Customer Value Through Cross-Functional Team SellingBrylle LeynesNo ratings yet

- Personal Selling and Sales Management: Slide 20-2Document14 pagesPersonal Selling and Sales Management: Slide 20-2Brylle LeynesNo ratings yet

- Sales Management TechniquesDocument22 pagesSales Management TechniquesBrylle LeynesNo ratings yet

- Sales Management ModuleDocument86 pagesSales Management ModuleBrylle Leynes100% (1)

- Universal College of Parañaque New Market Development Course SyllabusDocument2 pagesUniversal College of Parañaque New Market Development Course SyllabusBrylle LeynesNo ratings yet

- A Subject Requirement in Risk ManagementDocument28 pagesA Subject Requirement in Risk ManagementBrylle LeynesNo ratings yet

- Creating and Sustaining Customer Value Through Cross-Functional Team SellingDocument18 pagesCreating and Sustaining Customer Value Through Cross-Functional Team SellingBrylle LeynesNo ratings yet

- Chapter 3Document15 pagesChapter 3Brylle LeynesNo ratings yet

- Personal Finance Syllabus :)Document13 pagesPersonal Finance Syllabus :)Jocelyn P. Balasuela100% (1)

- Am 23Document6 pagesAm 23Anissa Negra AkroutNo ratings yet

- ValuesDocument14 pagesValuesmcheche12No ratings yet

- ManageMoney Class ENDocument52 pagesManageMoney Class ENBrylle LeynesNo ratings yet

- Industrial RevolutionDocument6 pagesIndustrial RevolutionBrylle LeynesNo ratings yet

- HW2 - Preparing Statement of Cash FlowsDocument2 pagesHW2 - Preparing Statement of Cash FlowsDeepak KapoorNo ratings yet

- Chapter 6Document71 pagesChapter 6Messa Marianka80% (5)

- Chap 2 Financial Analysis & PlanningDocument108 pagesChap 2 Financial Analysis & PlanningmedrekNo ratings yet

- Humpuss Intermoda Transportasi TBK - Bilingual - 31 - Dec - 2018 - Released PDFDocument132 pagesHumpuss Intermoda Transportasi TBK - Bilingual - 31 - Dec - 2018 - Released PDFAyu Krisma YupitaNo ratings yet

- Skywalker Co Journal Adjustments Income StatementDocument3 pagesSkywalker Co Journal Adjustments Income StatementZhida PratamaNo ratings yet

- Exercise On Csofp - Associates Paloma Fuego Delmara - FellowDocument2 pagesExercise On Csofp - Associates Paloma Fuego Delmara - FellowNoor ShukirrahNo ratings yet

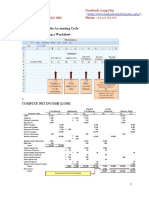

- Chapter 4: Completing The Accounting Cycle 1. Steps in Prepareing A WorksheetDocument8 pagesChapter 4: Completing The Accounting Cycle 1. Steps in Prepareing A WorksheetNguyễn Quỳnh AnhNo ratings yet

- Dragon Oil plc Annual Report highlights record revenues and productionDocument102 pagesDragon Oil plc Annual Report highlights record revenues and productionfaizulramliNo ratings yet

- The Frequency of Revaluation May Be:: B), Plant and Equipment With Only Insignificant Changes in Fair ValueDocument2 pagesThe Frequency of Revaluation May Be:: B), Plant and Equipment With Only Insignificant Changes in Fair ValueAlexander DimaliposNo ratings yet

- Product CostDocument2 pagesProduct Costmba departmentNo ratings yet

- Capital Gains Tax and Documentary Stamp Tax: Multiple Choice: Choose The Best Possible AnswerDocument16 pagesCapital Gains Tax and Documentary Stamp Tax: Multiple Choice: Choose The Best Possible AnswerMaryane AngelaNo ratings yet

- Africa Horizons: A Unique Guide To Real Estate Investment OpportunitiesDocument18 pagesAfrica Horizons: A Unique Guide To Real Estate Investment OpportunitiesJonathan MahengeNo ratings yet

- Chap 2 - Business ExpensesDocument185 pagesChap 2 - Business Expenseshippop kNo ratings yet

- MileIQ Ultimate Guide Mileage DeductionDocument19 pagesMileIQ Ultimate Guide Mileage DeductionjazzyzNo ratings yet

- Inventory ManagementDocument8 pagesInventory ManagementMike Padilla IINo ratings yet

- MULTIPLE CHOICE-ComputationalDocument5 pagesMULTIPLE CHOICE-Computationaljie calderonNo ratings yet

- Dabur Healthcare valuation reportDocument58 pagesDabur Healthcare valuation reportUmangNo ratings yet

- Study of Comparative Ratio AnalysisDocument68 pagesStudy of Comparative Ratio Analysisbalu mughalNo ratings yet

- Financial Statement AnalysisDocument31 pagesFinancial Statement AnalysisbilalahmedbhuttoNo ratings yet

- Ar6017 Urban Housing Unit 01 - NoDocument64 pagesAr6017 Urban Housing Unit 01 - Nosiva ramanNo ratings yet

- CRI - Solved Valuation Practical Sums - CS Vaibhav Chitlangia - Yes Academy, PuneDocument37 pagesCRI - Solved Valuation Practical Sums - CS Vaibhav Chitlangia - Yes Academy, Punegopika mundraNo ratings yet

- This Spreadsheet Supports Analysis of The Case, "Coleco Industries Inc." (Case 60)Document6 pagesThis Spreadsheet Supports Analysis of The Case, "Coleco Industries Inc." (Case 60)kashanr82No ratings yet

- LaporantahunanDocument231 pagesLaporantahunanelisa christianaNo ratings yet

- Solved Simple and Compound Interest ProblemsDocument44 pagesSolved Simple and Compound Interest ProblemsGlyzel Dizon0% (1)

- Barclays PDD PDD Holdings Inc. - Q4 Results Were Strong But Street ExpDocument12 pagesBarclays PDD PDD Holdings Inc. - Q4 Results Were Strong But Street Expoldman lokNo ratings yet

- Bank Account of The Living' Dead - Business, News, The Philippine Star - PhilstarDocument2 pagesBank Account of The Living' Dead - Business, News, The Philippine Star - PhilstarJon P CoNo ratings yet

- Mar 2019 SGVDocument24 pagesMar 2019 SGVBien Bowie A. CortezNo ratings yet

- Chapter 13 IAS 20 Govt GrantDocument11 pagesChapter 13 IAS 20 Govt GrantKelvin Chu JYNo ratings yet

- Strategic Purchasing For Universal Health CoverageDocument23 pagesStrategic Purchasing For Universal Health CoverageJorge Armando Arrieta ArrietaNo ratings yet

- FA VI Model Answer KeyDocument13 pagesFA VI Model Answer KeyAtharva SherkarNo ratings yet