You might also like

- Midterm Examination Educ 108Document2 pagesMidterm Examination Educ 108Joshua Kevin SolamoNo ratings yet

- Constructing Table of SpecificationDocument5 pagesConstructing Table of SpecificationAlphred Jann NaparanNo ratings yet

- Appropriateness of Assessment Methods Assessment Instruments AppropriatenessDocument3 pagesAppropriateness of Assessment Methods Assessment Instruments AppropriatenessJaysonNo ratings yet

- Assessment of Learning LET 2 PDFDocument32 pagesAssessment of Learning LET 2 PDFroderic v. perezNo ratings yet

- General Characteristics of Curriculum Development ModelsDocument2 pagesGeneral Characteristics of Curriculum Development ModelssetiawanNo ratings yet

- What Is Rubrics?Document2 pagesWhat Is Rubrics?Elhaine MadulaNo ratings yet

- Components of Formative AssessmentDocument2 pagesComponents of Formative AssessmentEric CabreraNo ratings yet

- The New Bloom's Taxonomy: An Interactive Quiz GameDocument28 pagesThe New Bloom's Taxonomy: An Interactive Quiz GameSaymon Casilang SarmientoNo ratings yet

- Lesson 3 Creating EPortfolio As A Technology ToolDocument18 pagesLesson 3 Creating EPortfolio As A Technology ToolKelly Danielle Quiton100% (1)

- Assessment of Learning UpdatedDocument240 pagesAssessment of Learning UpdatedDar M GonzalesNo ratings yet

- CCEDocument55 pagesCCEacer.kumud469750% (2)

- Ict in Various Content Areas: Unit 4Document10 pagesIct in Various Content Areas: Unit 4Jessa Melle RanaNo ratings yet

- Chapter 10Document4 pagesChapter 10April Jade MendozaNo ratings yet

- Unit 04 8602Document23 pagesUnit 04 8602maheen rasheedNo ratings yet

- The Concept of Education and Social ResearchDocument278 pagesThe Concept of Education and Social ResearchMuhammad Nawaz Khan AbbasiNo ratings yet

- WTL and Mini AMTBDocument23 pagesWTL and Mini AMTBAhmet Selçuk AkdemirNo ratings yet

- Assessment of Learning HandoutDocument9 pagesAssessment of Learning HandoutBlaze QuibanNo ratings yet

- PPST-RPMS BasedDocument33 pagesPPST-RPMS BasedJoselito Requirme AguaNo ratings yet

- Teaching Mathematics Using Blended Learning Model: A Case Study in Uitm Sarawak CampusDocument6 pagesTeaching Mathematics Using Blended Learning Model: A Case Study in Uitm Sarawak CampusfairusNo ratings yet

- ASSESSMENT OF LEARNING VaDocument5 pagesASSESSMENT OF LEARNING VaMagongcar hadjiali0% (1)

- C) Methods of Assessing Affective TargetsDocument26 pagesC) Methods of Assessing Affective TargetsHadassa ArzagaNo ratings yet

- Teaching Learning MaterialsDocument5 pagesTeaching Learning MaterialsOzelle PoeNo ratings yet

- Components of Daily Lesson PlansDocument1 pageComponents of Daily Lesson Plansapi-357377076No ratings yet

- Diagnostic and Remedial TeachingDocument12 pagesDiagnostic and Remedial TeachingYeit Fong TanNo ratings yet

- Why Students Resist Learner-Centered Teaching?Document5 pagesWhy Students Resist Learner-Centered Teaching?Z. A. AbdulJaleelNo ratings yet

- Implementationplan Chris ConnorsDocument3 pagesImplementationplan Chris ConnorstrushalvoraNo ratings yet

- GE 8 (Activity 1)Document2 pagesGE 8 (Activity 1)Myla GuabNo ratings yet

- Assure Model Lesson PlanDocument5 pagesAssure Model Lesson Planapi-318891614No ratings yet

- Curriculum DevelopmentDocument21 pagesCurriculum DevelopmentJolina Mamaluba BakuludanNo ratings yet

- National Curriculum Framework 2000Document17 pagesNational Curriculum Framework 2000Navneeta AvniNo ratings yet

- 4 Situation Analysis - HTMDocument18 pages4 Situation Analysis - HTMLucila Delgaudio (Lady Lemonade)No ratings yet

- Traditional and Alternative AssessmentDocument34 pagesTraditional and Alternative AssessmentCaro MoragaNo ratings yet

- Old Curriculum Old Curriculum New CurriculumDocument1 pageOld Curriculum Old Curriculum New CurriculumAGUIRRE, CATHERINE S.No ratings yet

- AssessmentDocument26 pagesAssessmentCristita Carmona100% (1)

- RationaleDocument2 pagesRationaleapi-317910994100% (1)

- Harriet Amihere Multimedia Audio or Video Lesson Idea Template2022Document3 pagesHarriet Amihere Multimedia Audio or Video Lesson Idea Template2022api-674932502No ratings yet

- Contextualizing Assessment TasksDocument38 pagesContextualizing Assessment TasksJoel MagbanuaNo ratings yet

- Educ 203 SyllabusDocument8 pagesEduc 203 Syllabusjasron09ryNo ratings yet

- Parent Teacher Meeting PDFDocument5 pagesParent Teacher Meeting PDFNada JamusNo ratings yet

- VergaraDocument6 pagesVergaraMichael Xian Lindo MarcelinoNo ratings yet

- Social Studies Grade 9Document8 pagesSocial Studies Grade 9Robert McleanNo ratings yet

- The Nature of Curriculum EvaluationDocument8 pagesThe Nature of Curriculum EvaluationDinesh MadhavanNo ratings yet

- Web 2 0 Lesson PlanDocument2 pagesWeb 2 0 Lesson Planapi-173648336No ratings yet

- 13 HMEF5053 T9 (Amend 14.12.16)Document22 pages13 HMEF5053 T9 (Amend 14.12.16)kalpanamoorthyaNo ratings yet

- Lesson 4 The Assure ModelDocument6 pagesLesson 4 The Assure ModelJeff Beloso BasNo ratings yet

- Grading Student EvaluationDocument69 pagesGrading Student EvaluationEddy White, PhDNo ratings yet

- Tos-Teacher-Made-Test-Group-3Document10 pagesTos-Teacher-Made-Test-Group-3Maestro MotovlogNo ratings yet

- The Nature, Goals and Content of The Language Subject AreasDocument3 pagesThe Nature, Goals and Content of The Language Subject Areas'Jhames Concepcion100% (1)

- Ahmed Amer M TH 2016 PHDDocument307 pagesAhmed Amer M TH 2016 PHDMUHAMMADNo ratings yet

- Performance in Language LearningDocument6 pagesPerformance in Language LearningDedeh KurniasihNo ratings yet

- Parameters Measurement Evaluation: Kind of DataDocument5 pagesParameters Measurement Evaluation: Kind of DataelsajacintoNo ratings yet

- Business Management RubricDocument4 pagesBusiness Management RubricJerzyAlferezNo ratings yet

- Gagne's Hierarchical Theory of InstructionDocument2 pagesGagne's Hierarchical Theory of InstructionManas Beck100% (1)

- Adeyemo, A. (2012) .The Relationship Between Effective Classroom Management and Students' Academic Achievement.Document15 pagesAdeyemo, A. (2012) .The Relationship Between Effective Classroom Management and Students' Academic Achievement.Fera Asmarita100% (1)

- Induction Training Manual For PrimaryDocument377 pagesInduction Training Manual For PrimaryKallo KalliNo ratings yet

- The Definition of Action ResearchDocument4 pagesThe Definition of Action ResearchAdelia PuspaNo ratings yet

- Free Sample: What Are The Disadvantages of Teacher Made Test?Document2 pagesFree Sample: What Are The Disadvantages of Teacher Made Test?Suleiman Abubakar AuduNo ratings yet

- CH 12 Student Handout 8e PDFDocument12 pagesCH 12 Student Handout 8e PDFTrường HuỳnhNo ratings yet

- Lecture Note-Ch 10-02-07-2018Document43 pagesLecture Note-Ch 10-02-07-2018Dogacan BoztepeNo ratings yet

- Opinion On Tax Residency Certificate Recipient: RECIPIENT NAME Date - 15th Mar, 2023Document4 pagesOpinion On Tax Residency Certificate Recipient: RECIPIENT NAME Date - 15th Mar, 2023Akash BagrechaNo ratings yet

- Adeyinka Oluwafunsho (134) $693.5 Thu Sep 03 11 48 00 EDT 2020 PDFDocument1 pageAdeyinka Oluwafunsho (134) $693.5 Thu Sep 03 11 48 00 EDT 2020 PDFGrace AdeyinkaNo ratings yet

- Income Tax Law & Practice Unit 4Document8 pagesIncome Tax Law & Practice Unit 4MuskanNo ratings yet

- Chapter 10 International Taxation: Multiple Choice QuestionsDocument16 pagesChapter 10 International Taxation: Multiple Choice QuestionsLara QalanziNo ratings yet

- Chapter 7 MCQs On Assessment of Partnership FirmDocument5 pagesChapter 7 MCQs On Assessment of Partnership FirmAmrendra MohanNo ratings yet

- Solved Englesbe Company S Futa Tax Liability Was 289 50 Futa Tax ForDocument1 pageSolved Englesbe Company S Futa Tax Liability Was 289 50 Futa Tax ForAnbu jaromiaNo ratings yet

- 7 CIR V PhoenixDocument1 page7 CIR V PhoenixFrancesca Isabel MontenegroNo ratings yet

- Taxation Comex1 CoverageDocument3 pagesTaxation Comex1 CoverageOwncoebdiefNo ratings yet

- Individual Assignment Public Finance and TaxationDocument3 pagesIndividual Assignment Public Finance and TaxationSahal Cabdi AxmedNo ratings yet

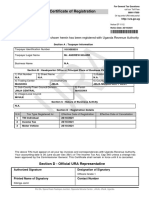

- Certificate of RegistrationDocument1 pageCertificate of RegistrationTechnicians SIMNo ratings yet

- Depreciation - WikipediaDocument10 pagesDepreciation - Wikipediapuput075No ratings yet

- Amit Dec 2020 PayslipDocument1 pageAmit Dec 2020 PayslipAmit GhangasNo ratings yet

- Lifetime Giving AND Inter Vivos Gifts: Greenfield Stein & Senior LLP New York, Ny Updated and Co-Authored byDocument30 pagesLifetime Giving AND Inter Vivos Gifts: Greenfield Stein & Senior LLP New York, Ny Updated and Co-Authored byVlad ZernovNo ratings yet

- Illustration On Special Revenue FundDocument2 pagesIllustration On Special Revenue FundJichang Hik0% (1)

- Accounting - UEB - Mock Test 2 - STDDocument14 pagesAccounting - UEB - Mock Test 2 - STDTiến NguyễnNo ratings yet

- Mint Company SFP PDFDocument3 pagesMint Company SFP PDFRengeline LucasNo ratings yet

- Vijayawada Sri Lakshmi Narasimha Ramanuja Kutam TrustDocument4 pagesVijayawada Sri Lakshmi Narasimha Ramanuja Kutam Trustbharath289No ratings yet

- TAX 667 Topic 8 Tax Planning For CompanyDocument63 pagesTAX 667 Topic 8 Tax Planning For Companyzarif nezukoNo ratings yet

- Towr LK TW I 2020Document153 pagesTowr LK TW I 2020cyndi noviaNo ratings yet

- Unit 2 (Income From House Property)Document3 pagesUnit 2 (Income From House Property)Vijay GiriNo ratings yet

- CIR Vs Isabela Cultural CorporationDocument2 pagesCIR Vs Isabela Cultural CorporationLauren KeiNo ratings yet

- Foreign Tax Credit: (Individual, Estate, or Trust)Document2 pagesForeign Tax Credit: (Individual, Estate, or Trust)Tanasha FlandersNo ratings yet

- D.T.L (2006 Pattern)Document14 pagesD.T.L (2006 Pattern)KuNdAn DeOrENo ratings yet

- The Organizational Plan: Hisrich Peters ShepherdDocument22 pagesThe Organizational Plan: Hisrich Peters ShepherdNisar Ahmed s/o Ameer BuxNo ratings yet

- 06 Withholding Tax On Compensation IncomeDocument13 pages06 Withholding Tax On Compensation IncomeZatsumono YamamotoNo ratings yet

- 2021 Tax Year - Virtual Tax Solutions LLCDocument14 pages2021 Tax Year - Virtual Tax Solutions LLCgregNo ratings yet

- 0 Control Sheet - Charge of Tax & 4 Key ConceptsDocument1 page0 Control Sheet - Charge of Tax & 4 Key ConceptsArman KhanNo ratings yet

- Cambridge Ordinary Level: Cambridge Assessment International EducationDocument12 pagesCambridge Ordinary Level: Cambridge Assessment International EducationBEeNaNo ratings yet

- Relic Spotter StatementsDocument6 pagesRelic Spotter StatementsArpit AgarwalNo ratings yet

- Rahbar Infotech Solutions PVT - LTD.: Salary Slip For The Month ofDocument1 pageRahbar Infotech Solutions PVT - LTD.: Salary Slip For The Month ofSalman KhanNo ratings yet