You might also like

- Determination of Solids in WaterDocument7 pagesDetermination of Solids in WaterManoj KarmakarNo ratings yet

- Universiti Teknologi Mara Common Test 1: Confidential AC/AUG 2015/MAF151Document4 pagesUniversiti Teknologi Mara Common Test 1: Confidential AC/AUG 2015/MAF151Nurul AinNo ratings yet

- The Usability Metrics For User ExperienceDocument6 pagesThe Usability Metrics For User ExperienceVIVA-TECH IJRINo ratings yet

- BMS533 Practical Lab Report (Group 6)Document37 pagesBMS533 Practical Lab Report (Group 6)YUSNURDALILA DALINo ratings yet

- Website Evaluation Ims556Document11 pagesWebsite Evaluation Ims556Fatin NazihahNo ratings yet

- Petronas Website Ims 556Document15 pagesPetronas Website Ims 556Luqman AriefNo ratings yet

- Work Immersion at Coffee ConnectDocument10 pagesWork Immersion at Coffee ConnectCrizalynn BantocNo ratings yet

- Kindergarten DLL MELC Q4 Week 10Document6 pagesKindergarten DLL MELC Q4 Week 10Regine QuinaNo ratings yet

- (Group Project - Marketing Plan) Group 10Document21 pages(Group Project - Marketing Plan) Group 10Tghusna FatmaNo ratings yet

- Final Executive SummaryDocument13 pagesFinal Executive SummaryDeon SmithNo ratings yet

- Blocher8e EOC SM Ch15 Final StudentDocument53 pagesBlocher8e EOC SM Ch15 Final StudentKatelynNo ratings yet

- SS Mar22 PDFDocument8 pagesSS Mar22 PDFuser mrmysteryNo ratings yet

- ANIMATION11 3rd QuarterDocument3 pagesANIMATION11 3rd QuarterNerissa TabuyanNo ratings yet

- Lab 1 Fst606Document12 pagesLab 1 Fst606fatiniNo ratings yet

- CT Question April 2018Document4 pagesCT Question April 2018Nabila RosmizaNo ratings yet

- Azrul Ikhwan Bin Azmi (2020414356) - Self ReflectionDocument8 pagesAzrul Ikhwan Bin Azmi (2020414356) - Self ReflectionAZRUL IKHWAN AZMINo ratings yet

- Universiti Teknologi Mara Common Test: Confidential 1 AC/MAY 2021/FAR270Document4 pagesUniversiti Teknologi Mara Common Test: Confidential 1 AC/MAY 2021/FAR270Lampard AimanNo ratings yet

- Individual Assignment MKT 558 Ahmad HaikalDocument11 pagesIndividual Assignment MKT 558 Ahmad HaikalAhmad HaikalNo ratings yet

- FAR270 Common Test 1 QuestionsDocument4 pagesFAR270 Common Test 1 Questionssharifah nurshahira sakinaNo ratings yet

- Tutoria 4 BKAL1013 A111Document3 pagesTutoria 4 BKAL1013 A111Izal ArfianNo ratings yet

- Accounting For Receivables Practice SolutionsDocument3 pagesAccounting For Receivables Practice SolutionsNgân GiangNo ratings yet

- Solution Maf603 - Jun 2018Document9 pagesSolution Maf603 - Jun 2018anis izzatiNo ratings yet

- AUD679 - Tutorial: ExplainationDocument3 pagesAUD679 - Tutorial: ExplainationMunNo ratings yet

- PBL 2 Mac 2020Document4 pagesPBL 2 Mac 2020Ummu UmairahNo ratings yet

- ISF 1101 Islamic Finance Profit Computation ExamplesDocument5 pagesISF 1101 Islamic Finance Profit Computation ExamplesPrashant VishwakarmaNo ratings yet

- Fin358 Chap 4 BondDocument5 pagesFin358 Chap 4 Bondsyaiera aqilahNo ratings yet

- Radical PolymerizationDocument9 pagesRadical PolymerizationAtie Iekah100% (1)

- Maf651 S1 Supply Chain ManagementDocument19 pagesMaf651 S1 Supply Chain ManagementMOHAMMAD ASYRAF NAZRI SAKRINo ratings yet

- GoodDocument30 pagesGoodDaus NohNo ratings yet

- Test FAR 570 Feb 2021Document2 pagesTest FAR 570 Feb 2021Putri Naajihah 4GNo ratings yet

- ISP565 Data Mining Assignment 2Document21 pagesISP565 Data Mining Assignment 2Yana AliNo ratings yet

- Universiti Teknologi Mara Suggested Solution For Students Common Test 1Document5 pagesUniversiti Teknologi Mara Suggested Solution For Students Common Test 1Nabila RosmizaNo ratings yet

- Solution Far560 - Jun 2015 (S)Document7 pagesSolution Far560 - Jun 2015 (S)MUHAMAD MUKHAIRI MUHAMAD HANIFAHNo ratings yet

- HV1Document20 pagesHV1Izwan AzrinNo ratings yet

- Solution FAR270 APRIL 2022Document6 pagesSolution FAR270 APRIL 2022Nur Fatin AmirahNo ratings yet

- Financial Statements 2, ModuleDocument4 pagesFinancial Statements 2, ModuleSUHARTO USMANNo ratings yet

- Past Year Far460 - Dec 2014Document7 pagesPast Year Far460 - Dec 2014Alief Zazman100% (1)

- Tutorial MAF661Document6 pagesTutorial MAF661Nur SyahidahNo ratings yet

- 13 Types of Consumer Personalities AdvertisementsDocument30 pages13 Types of Consumer Personalities AdvertisementsChi Xuan KanNo ratings yet

- TEST FAR670 - OCT2022 (NACAB10B) - 10 Dec 2022Document3 pagesTEST FAR670 - OCT2022 (NACAB10B) - 10 Dec 2022Fatin AqilahNo ratings yet

- I. Payback Period Same CF Project A Different CF Project BDocument6 pagesI. Payback Period Same CF Project A Different CF Project Bzh12w8No ratings yet

- Fin552 Topic 5 Homework ExercisesDocument3 pagesFin552 Topic 5 Homework ExercisesHardy MercurialNo ratings yet

- Topic 4 - Time Value of MoneyDocument64 pagesTopic 4 - Time Value of MoneyHisyam SeeNo ratings yet

- Financial Planning and Forecasting From Brigham & EhrhardtDocument52 pagesFinancial Planning and Forecasting From Brigham & EhrhardtAsif KhanNo ratings yet

- Read The Following Excerpt From A Complaint Filed by TheDocument1 pageRead The Following Excerpt From A Complaint Filed by TheLet's Talk With Hassan0% (1)

- Tutorial 2 Capital Allowances - Q&ADocument8 pagesTutorial 2 Capital Allowances - Q&AKamal JabriNo ratings yet

- Topic: Effect of Covid19 Toward Bank Islam Malaysia Berhad (BIMB) ProfitabilityDocument7 pagesTopic: Effect of Covid19 Toward Bank Islam Malaysia Berhad (BIMB) ProfitabilityLuqmanulhakim JohariNo ratings yet

- Practical 1: Determination of Reducing Sugar Using The Dinitrosalicylic (DNS) Colourimetric MethodDocument8 pagesPractical 1: Determination of Reducing Sugar Using The Dinitrosalicylic (DNS) Colourimetric MethodNurSyazaHaniNo ratings yet

- Lab 4 Logic Gate (Lab Report)Document4 pagesLab 4 Logic Gate (Lab Report)Izzat IkramNo ratings yet

- Taxation I Tutorial: Tax ReliefDocument2 pagesTaxation I Tutorial: Tax Reliefathirah jamaludinNo ratings yet

- Chapter 5 3rd Ed Supply Chain by WisnerDocument33 pagesChapter 5 3rd Ed Supply Chain by WisnerHassanSheikhNo ratings yet

- Chapter 1 IAS 36 Impairment of Assets PDFDocument11 pagesChapter 1 IAS 36 Impairment of Assets PDFGAIK SUEN TANNo ratings yet

- Bpc1123 Principles of Economics s2 0818Document13 pagesBpc1123 Principles of Economics s2 0818Nur Zarith HalisaNo ratings yet

- Solution Maf 635 Dec 2014Document8 pagesSolution Maf 635 Dec 2014anis izzatiNo ratings yet

- PPTDocument33 pagesPPTanis solihah0% (1)

- Chicken Run Case Study G3Document28 pagesChicken Run Case Study G3miejahNo ratings yet

- Financial statements analysis limitationsDocument2 pagesFinancial statements analysis limitationsNurul Shafirah0% (1)

- Solution Maf653 - Dec 2019 - StudentDocument7 pagesSolution Maf653 - Dec 2019 - Studentdini ffNo ratings yet

- QMT425 - Assignment 1Document5 pagesQMT425 - Assignment 1Azwan AyopNo ratings yet

- Capital Budgeting: Most Important in Corporate FinanceDocument35 pagesCapital Budgeting: Most Important in Corporate Financevibhu01No ratings yet

- IBA Workshop - DAY1Document62 pagesIBA Workshop - DAY1Navid GodilNo ratings yet

- Cousre OutlineDocument3 pagesCousre OutlineNavid GodilNo ratings yet

- Legal Frame Work of PakistanDocument6 pagesLegal Frame Work of PakistanNavid GodilNo ratings yet

- Legal NotesDocument20 pagesLegal NotesNavid GodilNo ratings yet

- Law Assignment 1Document8 pagesLaw Assignment 1Navid GodilNo ratings yet

- Law - EnvironmentDocument12 pagesLaw - EnvironmentNavid GodilNo ratings yet

- Lambeth Custom CabinetsDocument5 pagesLambeth Custom CabinetsNavid GodilNo ratings yet

- Assignment - Land Lease AgreemntDocument3 pagesAssignment - Land Lease AgreemntNavid GodilNo ratings yet

- Rules For ProspectusDocument3 pagesRules For ProspectusNavid GodilNo ratings yet

- 3 - Initial Analysis - Reliability AnalysisDocument13 pages3 - Initial Analysis - Reliability AnalysisNavid GodilNo ratings yet

- Snack Consumption Value LR MappingDocument1 pageSnack Consumption Value LR MappingNavid GodilNo ratings yet

- Company Write-Up and Problem Identification: Managing Operations Under CrisisDocument10 pagesCompany Write-Up and Problem Identification: Managing Operations Under CrisisNavid GodilNo ratings yet

- Risk & Return NG HA AnnexDocument1 pageRisk & Return NG HA AnnexNavid GodilNo ratings yet

- 4 - Initial Analysis - DimensionalityDocument70 pages4 - Initial Analysis - DimensionalityNavid GodilNo ratings yet

- 2.cost of Capital - 14-1-2020Document12 pages2.cost of Capital - 14-1-2020samreen iqbalNo ratings yet

- 10.cap+budgeting Cash Flows-1Document20 pages10.cap+budgeting Cash Flows-1Navid GodilNo ratings yet

- PDI 111 Mar24Document40 pagesPDI 111 Mar24xen101No ratings yet

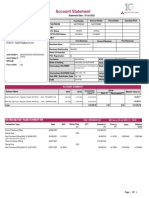

- Account StatementDocument3 pagesAccount Statementsia kamathNo ratings yet

- MalluDocument176 pagesMalluMallappaNo ratings yet

- RTM7Document7 pagesRTM7Sanchit ShresthaNo ratings yet

- Tax Minimization PlanDocument87 pagesTax Minimization Plan918JJonesNo ratings yet

- History of Economic ThoughtDocument56 pagesHistory of Economic ThoughthoogggleeeNo ratings yet

- Bloomberg For Sustainable Finance Analysis: A Bloomberg Terminal OfferingDocument16 pagesBloomberg For Sustainable Finance Analysis: A Bloomberg Terminal Offeringjuan camilo FrancoNo ratings yet

- Executive SummaryDocument41 pagesExecutive SummaryAhsAn Shafique100% (1)

- Leverage AnalysisDocument29 pagesLeverage AnalysisFALAK OBERAINo ratings yet

- Christa Clothing InternationalDocument15 pagesChrista Clothing Internationalaquib ansariNo ratings yet

- Olam InvestorPresentation Aug2018Document49 pagesOlam InvestorPresentation Aug2018Trade NerdNo ratings yet

- AFA 100 - Chapter 1 NotesDocument4 pagesAFA 100 - Chapter 1 NotesMichaelNo ratings yet

- Selby Jennings - Year in Review and 2022 Outlook With Salary Guide (South East Asia)Document23 pagesSelby Jennings - Year in Review and 2022 Outlook With Salary Guide (South East Asia)BIN LUNo ratings yet

- Working Capital Management ReportDocument43 pagesWorking Capital Management Reportsunny2311986100% (1)

- Model Financial Corpn. Ltd.Document13 pagesModel Financial Corpn. Ltd.srk1606No ratings yet

- Polycab India Balance Sheet Analysis March 2021Document4 pagesPolycab India Balance Sheet Analysis March 2021Kshitij SinghNo ratings yet

- Spectra Notes Tax Law 1 Compilation - Updated PDFDocument124 pagesSpectra Notes Tax Law 1 Compilation - Updated PDFBong OsorioNo ratings yet

- Corporate Governance Under The Provisions of The Companies Act, 2013Document10 pagesCorporate Governance Under The Provisions of The Companies Act, 2013Editor IJTSRDNo ratings yet

- Vodafone IntroductionDocument10 pagesVodafone IntroductionVishal JainNo ratings yet

- MXP 3 M9 F ITSh BNVK7911Document52 pagesMXP 3 M9 F ITSh BNVK7911Noshaba MaqsoodNo ratings yet

- Silabus PA - Genap2021-22 - Non-AkuntansiDocument4 pagesSilabus PA - Genap2021-22 - Non-AkuntansiGea CherlitaNo ratings yet

- FEL Aplication in Mining Capital ProjectsDocument36 pagesFEL Aplication in Mining Capital ProjectsWilliam CurieNo ratings yet

- Chapter 7 Advance Accounting Volume 1 2008Document15 pagesChapter 7 Advance Accounting Volume 1 2008andrewhomil_17199886% (7)

- Powerpoint in Entrep 1-3Document376 pagesPowerpoint in Entrep 1-3Joeferson Baguio Dancel100% (4)

- BarcalaysDocument61 pagesBarcalaysNikhil Khurana0% (1)

- Baran Sweezy Monopoly Capital An Essay On The American Economic and Social Order OCRDocument212 pagesBaran Sweezy Monopoly Capital An Essay On The American Economic and Social Order OCRTeresa CarterNo ratings yet

- Notice: Self-Regulatory Organizations Proposed Rule Changes: SSgA Funds Management, Inc., Et Al.Document7 pagesNotice: Self-Regulatory Organizations Proposed Rule Changes: SSgA Funds Management, Inc., Et Al.Justia.comNo ratings yet

- Financial Performance Analysis of TeslaDocument20 pagesFinancial Performance Analysis of TeslaDaniel WambuaNo ratings yet

- CHAPTER 12 Liquidation Partnership (Depreciation)Document6 pagesCHAPTER 12 Liquidation Partnership (Depreciation)nashNo ratings yet

- FA1 Chapter 3 EngDocument24 pagesFA1 Chapter 3 EngNicola PoonNo ratings yet