You might also like

- Financing Handbook for Companies: A Practical Guide by A Banking Executive for Companies Seeking Loans & Financings from BanksFrom EverandFinancing Handbook for Companies: A Practical Guide by A Banking Executive for Companies Seeking Loans & Financings from BanksRating: 5 out of 5 stars5/5 (1)

- Purpose of Loan & Amount Information of ApplicantDocument5 pagesPurpose of Loan & Amount Information of ApplicantNecky SairahNo ratings yet

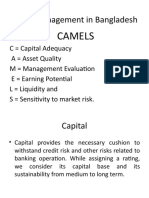

- Credit Management in BangladeshDocument13 pagesCredit Management in BangladeshPrasenjit SahaNo ratings yet

- Gurpreet Singh Cibil ReportDocument13 pagesGurpreet Singh Cibil Reportmahalbarinder77No ratings yet

- Theory Assignment 1Document22 pagesTheory Assignment 1Akshay RathiNo ratings yet

- Short QuestionDocument25 pagesShort Questionuttamdas79No ratings yet

- What Is Credit Appraisal?Document4 pagesWhat Is Credit Appraisal?maniyarasanNo ratings yet

- Credit MonitoringDocument166 pagesCredit Monitoringjananidhanasekaran26No ratings yet

- TrainingDocument51 pagesTrainingrafajr189No ratings yet

- ÁIFM Terms and ConditionsDocument3 pagesÁIFM Terms and Conditionspizza nmorevikNo ratings yet

- Debt Funding Proposal - Dubai CompaniesDocument5 pagesDebt Funding Proposal - Dubai CompaniesKunal SoniNo ratings yet

- NBFC Nov-23 Amended NotesDocument9 pagesNBFC Nov-23 Amended Notesrtaxhelp helpNo ratings yet

- Credit AppraisalDocument31 pagesCredit AppraisalSudershan Thaiba100% (1)

- LBSIM, New Delhi: - Group 7 Gaurav Gupta Vivek Sharan Amrita Pattnaik Anand Wardhan Srikant SharmaDocument35 pagesLBSIM, New Delhi: - Group 7 Gaurav Gupta Vivek Sharan Amrita Pattnaik Anand Wardhan Srikant SharmazvaibhavNo ratings yet

- Adv - NBFCDocument7 pagesAdv - NBFCrshyams165No ratings yet

- Trade Credit Insurance Presentation - HDFC ERGO 05012016Document22 pagesTrade Credit Insurance Presentation - HDFC ERGO 05012016BOC ClaimsNo ratings yet

- Tip TopDocument8 pagesTip Topmani samiNo ratings yet

- Credit Policy Version 1.2Document157 pagesCredit Policy Version 1.2Amit SinghNo ratings yet

- Investment Form 1Document4 pagesInvestment Form 1Ahmed KhanNo ratings yet

- Delinquency Resolution and LearningsDocument18 pagesDelinquency Resolution and LearningsWhats going on indiaNo ratings yet

- DRM 1 - Credit Derivatives V2Document41 pagesDRM 1 - Credit Derivatives V2Mukul BaviskarNo ratings yet

- BlueVine Small-Business Loans - 2020 Review - 1 NerdWalletDocument5 pagesBlueVine Small-Business Loans - 2020 Review - 1 NerdWalletfosamorNo ratings yet

- IDFC LAP Agreement Bucket 5Document92 pagesIDFC LAP Agreement Bucket 5madhukar sahayNo ratings yet

- Ruff Spirits - Eportfoltio PresentationDocument13 pagesRuff Spirits - Eportfoltio Presentationapi-509845050No ratings yet

- Risk ManagementDocument14 pagesRisk ManagementMichelle TNo ratings yet

- Securitization CDO CDS Subprime CrisesDocument81 pagesSecuritization CDO CDS Subprime Crisesshwetata986No ratings yet

- Importance of Consumer Durable Loan For Keralites: SL - No ParametersDocument8 pagesImportance of Consumer Durable Loan For Keralites: SL - No ParametersSandeep MishraNo ratings yet

- FinPRO Final Assessment and Quiz Competition Question BankDocument37 pagesFinPRO Final Assessment and Quiz Competition Question Bankfahimafathima492No ratings yet

- Your Auto Loan Search Results: $49,089 60 MonthsDocument1 pageYour Auto Loan Search Results: $49,089 60 MonthsDustin NashNo ratings yet

- CHR Report - 28 August 2023Document12 pagesCHR Report - 28 August 2023Alok G ShindeNo ratings yet

- KMA Sacco Loan Application FormDocument4 pagesKMA Sacco Loan Application FormDr. philemon mwongeraNo ratings yet

- Post-Dated Cheques in The UAE - The Pros and ConsDocument4 pagesPost-Dated Cheques in The UAE - The Pros and Consfortune xiuNo ratings yet

- Factoring: Presented ByDocument24 pagesFactoring: Presented ByswatigouravNo ratings yet

- Sources of Working CapitalDocument17 pagesSources of Working CapitalAyush ShrimalNo ratings yet

- Classification N ProvisionDocument37 pagesClassification N ProvisionNur AlahiNo ratings yet

- KWP/ADV/2022/ Date: 14/04/2022: REF NO: BOB/KAWEMPE/ADV/2022-65 Dated 14/04/2022Document2 pagesKWP/ADV/2022/ Date: 14/04/2022: REF NO: BOB/KAWEMPE/ADV/2022-65 Dated 14/04/2022BalavinayakNo ratings yet

- CreditQ MSME Services - B2B Services - CIRDocument12 pagesCreditQ MSME Services - B2B Services - CIRJyoti GuptaNo ratings yet

- TBergin-2018 New York Idea ContestDocument33 pagesTBergin-2018 New York Idea ContestConstantin WellsNo ratings yet

- Credit Rating AND Term Loans: Presented By: Hemant Kumar Upadahyay Pawan Kumar Ravi Kumar Sonika SharmaDocument28 pagesCredit Rating AND Term Loans: Presented By: Hemant Kumar Upadahyay Pawan Kumar Ravi Kumar Sonika SharmaSush KaushikNo ratings yet

- CHR Report - 06 August 2023Document30 pagesCHR Report - 06 August 2023Venella PatrickNo ratings yet

- Original: Your Credit Score and The Price You Pay For CreditDocument26 pagesOriginal: Your Credit Score and The Price You Pay For CreditMaritza CardonaNo ratings yet

- Investment FormDocument4 pagesInvestment FormArslan ButtNo ratings yet

- Types of Accounts, Bank Guarantee, LC, Line of CreditDocument44 pagesTypes of Accounts, Bank Guarantee, LC, Line of Creditkaren sunilNo ratings yet

- CDD Form IndividualDocument1 pageCDD Form IndividualArslan ButtNo ratings yet

- Credit Rating Credit RatingDocument37 pagesCredit Rating Credit Ratingrakesh288No ratings yet

- Helix Bond - Privilidge - Wealth PDFDocument12 pagesHelix Bond - Privilidge - Wealth PDFhyenadogNo ratings yet

- SWATI SBI - OrganizedDocument5 pagesSWATI SBI - OrganizedVinod MNo ratings yet

- Captive Insurance Collateral OptionsDocument15 pagesCaptive Insurance Collateral OptionsMuhammad SaleemNo ratings yet

- Credit Rating in India - JBIMSDocument8 pagesCredit Rating in India - JBIMSSidhi AgarwalNo ratings yet

- Bonitetno Porocilo - RS - ENDocument11 pagesBonitetno Porocilo - RS - ENAgit SipkaNo ratings yet

- Group 3 PresentationDocument38 pagesGroup 3 PresentationCherie Soriano AnanayoNo ratings yet

- Cred and BudgDocument26 pagesCred and BudgAndrea SesennaNo ratings yet

- What Affects Your Credit ScoreDocument7 pagesWhat Affects Your Credit ScoreAlpa DwivediNo ratings yet

- Macroeconomic (Saving and Investment)Document110 pagesMacroeconomic (Saving and Investment)Sheillie KirklandNo ratings yet

- Chapter 13: Commercial Bank Operations 3edDocument26 pagesChapter 13: Commercial Bank Operations 3edMarwa HassanNo ratings yet

- CH - 1 - Introduction To Financial System and Types of RisksDocument20 pagesCH - 1 - Introduction To Financial System and Types of RisksApra khediNo ratings yet

- AnalytixWise - Risk Analytics Unit 3 Credit Risk AnalyticsDocument29 pagesAnalytixWise - Risk Analytics Unit 3 Credit Risk AnalyticsUrvashi Singh100% (1)

- CHR Report - 24 August 2023Document27 pagesCHR Report - 24 August 2023jyotirajeshlicNo ratings yet

- Letter of CreditDocument4 pagesLetter of CreditaldryNo ratings yet

- Tips On Starting A Garment BusinessDocument24 pagesTips On Starting A Garment BusinessmoidulmktduNo ratings yet

- Financial Statement Analysis Ratio Analysis, CRR, SLRDocument16 pagesFinancial Statement Analysis Ratio Analysis, CRR, SLRmoidulmktduNo ratings yet

- How To Solve Case StudyDocument12 pagesHow To Solve Case Studyburhan_qureshiNo ratings yet

- IB ManualDocument466 pagesIB ManualSunpreet Singh100% (3)

- Taxation of Business Entities 2017 8th Edition Spilker Solutions ManualDocument11 pagesTaxation of Business Entities 2017 8th Edition Spilker Solutions Manualotisviviany9zoNo ratings yet

- A Comparative Study of Bancassurance Products in Banks - SynopsisDocument8 pagesA Comparative Study of Bancassurance Products in Banks - Synopsisammukhan khan100% (1)

- Cnc-Mc-And-Automation 5th Sem121755-May-2019Document2 pagesCnc-Mc-And-Automation 5th Sem121755-May-2019Lovelysingh LovelyNo ratings yet

- Draft (POM Netflix)Document11 pagesDraft (POM Netflix)Jesveena JassalNo ratings yet

- How To Create An Employee in Oracle Fusion R13Document5 pagesHow To Create An Employee in Oracle Fusion R13shashankNo ratings yet

- MOS Case StudyDocument3 pagesMOS Case StudySakshi AgarwalNo ratings yet

- It Is The Final Stage in The Strategic Management ProcessDocument66 pagesIt Is The Final Stage in The Strategic Management ProcessnathalieNo ratings yet

- SOCIAL SCIENCE - Practice PaperDocument8 pagesSOCIAL SCIENCE - Practice Paperkhushaliramani02No ratings yet

- Joint Affidavit of UndertakingDocument1 pageJoint Affidavit of UndertakingMarlon RondainNo ratings yet

- AKPI Annual Report 2017Document198 pagesAKPI Annual Report 2017firaNo ratings yet

- Inmarsat-C DNID Management Tool User Manual: Version 4.0 July 2010Document19 pagesInmarsat-C DNID Management Tool User Manual: Version 4.0 July 2010HaddNo ratings yet

- 3i Chapter 1Document7 pages3i Chapter 1Raoul Julian S. SarmientoNo ratings yet

- Eric Tsui - Technology in Knowledge ManagementDocument148 pagesEric Tsui - Technology in Knowledge ManagementDhimitri BibolliNo ratings yet

- Running Head: SEGMENT REPORTINGDocument6 pagesRunning Head: SEGMENT REPORTINGRajshekhar BoseNo ratings yet

- Rent Agreement-1Document2 pagesRent Agreement-1ishan srivastava100% (2)

- Business Model CanvasDocument2 pagesBusiness Model Canvasapi-567132652No ratings yet

- Together We Fight Society Vs AppleDocument20 pagesTogether We Fight Society Vs AppleLia JoseNo ratings yet

- Bandwidth Pricing and Its EconomicsDocument20 pagesBandwidth Pricing and Its EconomicsGarvit SharmaNo ratings yet

- Mobile Virtual Network Operators in The Sultanate of OmanDocument9 pagesMobile Virtual Network Operators in The Sultanate of Omanknpsingh7092No ratings yet

- Understanding Sustainable Consumption in An Emerging Country: The Antecedents and Consequences of The Ecologically Conscious Consumer Behavior ModelDocument10 pagesUnderstanding Sustainable Consumption in An Emerging Country: The Antecedents and Consequences of The Ecologically Conscious Consumer Behavior ModelgbendiniNo ratings yet

- Shaik Saleem PMP® & PGMP®: Sr. Project'S (Portfolio) Control Manager / Senior Program ManagerDocument5 pagesShaik Saleem PMP® & PGMP®: Sr. Project'S (Portfolio) Control Manager / Senior Program ManagerShaik SaleemNo ratings yet

- The Emergence of K-Beauty Rituals and Myths of Korean Skin Care PracticeDocument2 pagesThe Emergence of K-Beauty Rituals and Myths of Korean Skin Care PracticeArdhia Mutiara Cahyaning PutriNo ratings yet

- WSCSS - Worksheets 3 Parent 2023 01Document6 pagesWSCSS - Worksheets 3 Parent 2023 01mom2asherloveNo ratings yet

- Controversies in Digital EthicsDocument393 pagesControversies in Digital EthicsAlyssa Marie SantosNo ratings yet

- 26208-Article Text-30589-1-10-20181210Document10 pages26208-Article Text-30589-1-10-20181210mrizzqi22No ratings yet

- BSC Template: Instructions & CautionsDocument5 pagesBSC Template: Instructions & CautionsAllan VillagonzaloNo ratings yet

- Chapter 8.2Document44 pagesChapter 8.2naseelaidNo ratings yet

- IHRM in The Host-Country Context: Chapter EightDocument21 pagesIHRM in The Host-Country Context: Chapter EightXahra Mir100% (1)

- Resume Frank Rothaermel - Strategic Management Chapter 5Document3 pagesResume Frank Rothaermel - Strategic Management Chapter 5Dani YustiardiNo ratings yet

- Lecture 17 BH CH 9 Stock and Their Valuation Part 1Document30 pagesLecture 17 BH CH 9 Stock and Their Valuation Part 1Alif SultanliNo ratings yet