You might also like

- International Business 16th Edition Daniels Test BankDocument24 pagesInternational Business 16th Edition Daniels Test BankCynthiaWangeagjy100% (31)

- C1-Maharlika Yolk-Part 1-PanesDocument4 pagesC1-Maharlika Yolk-Part 1-PanesMary R. R. PanesNo ratings yet

- Frozen Fruit & Juice Production: Brain Freeze: Low Demand For Frozen Juice Is Expected To Limit Revenue GrowthDocument47 pagesFrozen Fruit & Juice Production: Brain Freeze: Low Demand For Frozen Juice Is Expected To Limit Revenue GrowthArnu Felix CamposNo ratings yet

- Accorhotels' Digital TransformationDocument11 pagesAccorhotels' Digital TransformationRitik Maheshwari100% (1)

- Contemporary Business Mathematics For Colleges 17th Edition Deitz Test BankDocument16 pagesContemporary Business Mathematics For Colleges 17th Edition Deitz Test Bankhelgahue0g4i100% (25)

- Working: Lunch Dinner Sales Units 7800 20280 Sales Price 12 25 93600 507000Document8 pagesWorking: Lunch Dinner Sales Units 7800 20280 Sales Price 12 25 93600 507000kudkhanNo ratings yet

- Profit Planning: Asic Framework of Budgeting AccountingDocument5 pagesProfit Planning: Asic Framework of Budgeting AccountingMichaela CruzNo ratings yet

- AKMEN Pertm 4, 5Document127 pagesAKMEN Pertm 4, 5UJI TESTNo ratings yet

- ACT4105 - Class 05 06 07 (Printing)Document24 pagesACT4105 - Class 05 06 07 (Printing)Wong Siu CheongNo ratings yet

- Budgeting Basics and Beyond Ver. 4.0Document46 pagesBudgeting Basics and Beyond Ver. 4.0Ana Mae Tayoan Castro100% (1)

- Chapter 9 Garrison 13eDocument88 pagesChapter 9 Garrison 13efarhan MomenNo ratings yet

- Chapter - 8 - Master BudgetingDocument92 pagesChapter - 8 - Master Budgetingshamsirarefin275285No ratings yet

- F2-12 Budgeting - Nature, Purpose and Behavioural AspectsDocument12 pagesF2-12 Budgeting - Nature, Purpose and Behavioural AspectsJaved ImranNo ratings yet

- A181 Bkam3023 Topic 2 - Master Budget Flexible BudgetDocument107 pagesA181 Bkam3023 Topic 2 - Master Budget Flexible BudgetJagethiswari RajahNo ratings yet

- Chap 009Document21 pagesChap 009Đức LộcNo ratings yet

- IPPTChap 008Document92 pagesIPPTChap 008AnasChihabNo ratings yet

- Pma3143 Chapter 4 Budgeting 0422Document23 pagesPma3143 Chapter 4 Budgeting 0422SYIMINNo ratings yet

- BUDGETINGDocument7 pagesBUDGETINGMarjorie ManuelNo ratings yet

- Lecture Notes: Learning Objective 1: Understand Why Organizations Budget and The Processes They Use To Create BudgetsDocument40 pagesLecture Notes: Learning Objective 1: Understand Why Organizations Budget and The Processes They Use To Create BudgetsPang SiulienNo ratings yet

- A222 - Topic 4 MacsDocument29 pagesA222 - Topic 4 MacsfiqNo ratings yet

- BR 3Document8 pagesBR 3b23014No ratings yet

- Budgetary Control and Standard CostingDocument15 pagesBudgetary Control and Standard CostingPratyay DasNo ratings yet

- FinmanDocument4 pagesFinmanMycah ManriqueNo ratings yet

- GNB - 09 - 12e Profit PlanningDocument89 pagesGNB - 09 - 12e Profit PlanningAhmed Mostafa ElmowafyNo ratings yet

- Functional and Activity Based BudgetingDocument5 pagesFunctional and Activity Based BudgetingBrithney ButalidNo ratings yet

- Chap009 Profit PlanningDocument15 pagesChap009 Profit PlanningThida WinNo ratings yet

- Budget F MacDocument94 pagesBudget F MacAkshat ShuklaNo ratings yet

- BudgetingDocument13 pagesBudgetingUditha Muthumala100% (1)

- Budgeting: Basics and Beyond: Continuing Professional Development ModuleDocument46 pagesBudgeting: Basics and Beyond: Continuing Professional Development ModuleNarissa Mae QuijanoNo ratings yet

- Guru Ghasidas Vishwavidyalaya: Department of Management Studies Mba 1St SemesterDocument39 pagesGuru Ghasidas Vishwavidyalaya: Department of Management Studies Mba 1St SemesterDivyansh Singh baghelNo ratings yet

- Module 006 BudgetingDocument12 pagesModule 006 BudgetinggagahejuniorNo ratings yet

- SPPTChap 008Document17 pagesSPPTChap 008Farhan RabbehNo ratings yet

- Chapter 9 - Profit PlanningDocument5 pagesChapter 9 - Profit Planningjoseph planasNo ratings yet

- © 2015 Mcgraw-Hill Education Garrison, Noreen, Brewer, Cheng & YuenDocument115 pages© 2015 Mcgraw-Hill Education Garrison, Noreen, Brewer, Cheng & YuenJoshua JojoNo ratings yet

- Master Budgeting Master Budgeting: The Basic Framework of BudgetingDocument9 pagesMaster Budgeting Master Budgeting: The Basic Framework of BudgetingArisha KhanNo ratings yet

- Kuliah 1 MANAGEMENT - CONTROL - SYSTEMS - 1Document24 pagesKuliah 1 MANAGEMENT - CONTROL - SYSTEMS - 1Ismail MuhammadNo ratings yet

- Budgets and Budgetary ControlDocument42 pagesBudgets and Budgetary ControlBishnu S. MukherjeeNo ratings yet

- The Budgeting FrameworkDocument47 pagesThe Budgeting FrameworkRecruit guideNo ratings yet

- ACCA Integrated Workbook F5 Chapter8Document20 pagesACCA Integrated Workbook F5 Chapter8Sunny Kumar10No ratings yet

- Chapter 9 - Profit PlanningDocument15 pagesChapter 9 - Profit PlanningAmitav BaruaNo ratings yet

- Master BudgetingDocument3 pagesMaster BudgetingmiglapadaNo ratings yet

- Chapter One Master BudgetingDocument89 pagesChapter One Master BudgetingFidelina CastroNo ratings yet

- Operating and Financial Budgeting FinalDocument10 pagesOperating and Financial Budgeting FinalKharen SantosNo ratings yet

- MAS.2906 - Short-Term BudgetingDocument9 pagesMAS.2906 - Short-Term BudgetingEyes SawNo ratings yet

- Profit Planning: Mcgraw-Hill/IrwinDocument88 pagesProfit Planning: Mcgraw-Hill/IrwinRahamat UllahNo ratings yet

- Mepl CostingDocument303 pagesMepl CostingVinay KumarNo ratings yet

- Udgets Udgetary Ontrol: Learning OutcomesDocument84 pagesUdgets Udgetary Ontrol: Learning OutcomesRAJIB HOSSAINNo ratings yet

- Udgets Udgetary Ontrol: Learning OutcomesDocument85 pagesUdgets Udgetary Ontrol: Learning OutcomesRishabh Jain100% (1)

- BudgetingDocument22 pagesBudgetingAashikkhan50% (2)

- Cima Budget and Standard CostsDocument102 pagesCima Budget and Standard CostsLitha MushianaNo ratings yet

- Lesson 7Document103 pagesLesson 7henielh965No ratings yet

- Budgetary ControlDocument12 pagesBudgetary ControlAhesan AnsariNo ratings yet

- Unit 3 Section 2Document4 pagesUnit 3 Section 2Babamu Kalmoni JaatoNo ratings yet

- Operating and Financial Budgeting (Final)Document7 pagesOperating and Financial Budgeting (Final)Mica R.No ratings yet

- Budgetary Control and Standard Costing2Document45 pagesBudgetary Control and Standard Costing2Pratyay DasNo ratings yet

- Budgetary Control and Standard Costing2Document45 pagesBudgetary Control and Standard Costing2Pratyay DasNo ratings yet

- Budget and Budgetary ControlDocument10 pagesBudget and Budgetary Controlzeebee17No ratings yet

- Budgeting: by Rosemarie Kelly, PHD, Fca, MBS, Dip Acc, Examiner, F2 Management Accounting, January 2019Document6 pagesBudgeting: by Rosemarie Kelly, PHD, Fca, MBS, Dip Acc, Examiner, F2 Management Accounting, January 2019Godfrey MakurumureNo ratings yet

- Long Term PlanningDocument11 pagesLong Term PlanninghelperforeuNo ratings yet

- Lecture 2. Budgets - 1 CPTG 149Document44 pagesLecture 2. Budgets - 1 CPTG 149NamitBhasinNo ratings yet

- Chapter 4 - BudgetingDocument9 pagesChapter 4 - BudgetingVuong PhamNo ratings yet

- Budgetary ControlDocument15 pagesBudgetary Controlstephie18No ratings yet

- Production Budgets: Understand Why Organizations Budget and The Processes They Use To Create BudgetsDocument74 pagesProduction Budgets: Understand Why Organizations Budget and The Processes They Use To Create BudgetsRoman AliNo ratings yet

- CH - 2 For TeacherDocument11 pagesCH - 2 For TeacherEbsa AdemeNo ratings yet

- LJD 1204 Final ExamDocument12 pagesLJD 1204 Final ExamMary R. R. PanesNo ratings yet

- Beylis TagalogDocument122 pagesBeylis TagalogMary R. R. PanesNo ratings yet

- FINAL UPDATED - Working - Paper - PanesDocument76 pagesFINAL UPDATED - Working - Paper - PanesMary R. R. PanesNo ratings yet

- Property Plant and Equipment 266,372.00: Total Project CostDocument80 pagesProperty Plant and Equipment 266,372.00: Total Project CostMary R. R. PanesNo ratings yet

- FINAL Working Paper Bien GonzalesDocument83 pagesFINAL Working Paper Bien GonzalesMary R. R. PanesNo ratings yet

- January February March Cash SalesDocument13 pagesJanuary February March Cash SalesMary R. R. PanesNo ratings yet

- Sales FinPart2Document2 pagesSales FinPart2Mary R. R. PanesNo ratings yet

- The Project Planner: Marketing Management GMB 724 - 1S Saturday Class Room - 208Document50 pagesThe Project Planner: Marketing Management GMB 724 - 1S Saturday Class Room - 208Mary R. R. PanesNo ratings yet

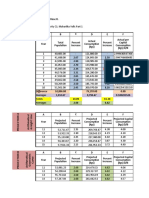

- Learning Activity C2: Maharlika Yolk: Part 2: Difference Averages Totals AveragesDocument4 pagesLearning Activity C2: Maharlika Yolk: Part 2: Difference Averages Totals AveragesMary R. R. PanesNo ratings yet

- Reflection On Cost of Capital FM 8.23.19Document2 pagesReflection On Cost of Capital FM 8.23.19Mary R. R. PanesNo ratings yet

- Overview of Green PlantsDocument49 pagesOverview of Green PlantsMary R. R. PanesNo ratings yet

- Salesdistribution: SalesDocument7 pagesSalesdistribution: SalesMary R. R. PanesNo ratings yet

- UE Midterms Persons 2021Document8 pagesUE Midterms Persons 2021Mary R. R. PanesNo ratings yet

- Reflection On Capital Budgeting FM 8.23.19Document3 pagesReflection On Capital Budgeting FM 8.23.19Mary R. R. PanesNo ratings yet

- Principals of A CrimeDocument4 pagesPrincipals of A CrimeMary R. R. PanesNo ratings yet

- First Periodical Test in Biology IIDocument5 pagesFirst Periodical Test in Biology IIMary R. R. PanesNo ratings yet

- CELYNs MonologueDocument4 pagesCELYNs MonologueMary R. R. PanesNo ratings yet

- Managing Stress and The Work-Life Balance: By: Valerie CoDocument16 pagesManaging Stress and The Work-Life Balance: By: Valerie CoMary R. R. PanesNo ratings yet

- Chapter 29 LectureDocument69 pagesChapter 29 LectureMary R. R. PanesNo ratings yet

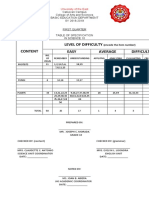

- Content Level of Difficulty Easy Average Difficult: University of The EastDocument2 pagesContent Level of Difficulty Easy Average Difficult: University of The EastMary R. R. PanesNo ratings yet

- Quiz #1Document1 pageQuiz #1Mary R. R. PanesNo ratings yet

- Organizational Change and DevelopmentDocument18 pagesOrganizational Change and DevelopmentMary R. R. PanesNo ratings yet

- Chapter Four: Motivation in OrganizationsDocument20 pagesChapter Four: Motivation in OrganizationsMary R. R. PanesNo ratings yet

- Legal Wrinting PDFDocument16 pagesLegal Wrinting PDF1706848296No ratings yet

- Introduction To Capital BudgetingDocument20 pagesIntroduction To Capital BudgetingMary R. R. PanesNo ratings yet

- HBO PPT CHAPTER 6Document13 pagesHBO PPT CHAPTER 6Mary R. R. PanesNo ratings yet

- Changing Environment of Organizations ReportDocument17 pagesChanging Environment of Organizations ReportMary R. R. PanesNo ratings yet

- Anagement OF Cash: Dr. Neeraj Chitkara Assistant Professor Samalkha Group of InstitutionsDocument57 pagesAnagement OF Cash: Dr. Neeraj Chitkara Assistant Professor Samalkha Group of InstitutionsMary R. R. PanesNo ratings yet

- PCG Credential Ver2.0 - GeneralDocument26 pagesPCG Credential Ver2.0 - GeneralDimas CindarbumiNo ratings yet

- Master List of Registered Cooperatives in The PhilippinesDocument1,324 pagesMaster List of Registered Cooperatives in The PhilippinesJahanna MartorillasNo ratings yet

- Coca Cola (KO) Financial RatiosDocument4 pagesCoca Cola (KO) Financial RatiosKhmao SrosNo ratings yet

- Documentation - Cascading The Local Road Governance Reforms in The Component Cities and MunicipalitiesDocument36 pagesDocumentation - Cascading The Local Road Governance Reforms in The Component Cities and Municipalitieskcp4btqm7pNo ratings yet

- Popular Industries: EdappallyDocument79 pagesPopular Industries: EdappallyAlex John MadavanaNo ratings yet

- TALF Annual Report 2018Document197 pagesTALF Annual Report 2018Doni WarganegaraNo ratings yet

- 1 MT PreviewDocument7 pages1 MT Previewjdalvaran100% (1)

- Fdi and Its Impact On Indian EconomyDocument22 pagesFdi and Its Impact On Indian EconomyYash AgarwalNo ratings yet

- Nissan Intelligent Ownership BrochureDocument4 pagesNissan Intelligent Ownership BrochureJjhdental OpdNo ratings yet

- Khalil QuestionnaireDocument6 pagesKhalil QuestionnaireAffan KhanNo ratings yet

- Group Assignment For The Course Introduction To Economics May 9Document4 pagesGroup Assignment For The Course Introduction To Economics May 9yohannes lemiNo ratings yet

- Modul Minggu Ke-2Document14 pagesModul Minggu Ke-2Sandi AdityaNo ratings yet

- Case Study:: How I Generated N310K in 7 Days Using WhatsappDocument12 pagesCase Study:: How I Generated N310K in 7 Days Using WhatsappCollins felixNo ratings yet

- Bisi 2018Document96 pagesBisi 2018Akun NuyulNo ratings yet

- K - GRP 7 - Report On Aviation SectorDocument47 pagesK - GRP 7 - Report On Aviation SectorApoorva PattnaikNo ratings yet

- Proforma InvoiceDocument1 pageProforma Invoice黃嘉德No ratings yet

- Payhawk Ebook How To Manage Month End Close Like A ProDocument11 pagesPayhawk Ebook How To Manage Month End Close Like A ProCorneliu Bajenaru - Talisman Consult SRLNo ratings yet

- PT Garuda Indonesia Persero TBK IDX GIAA FinancialsDocument48 pagesPT Garuda Indonesia Persero TBK IDX GIAA FinancialsTEDY TEDYNo ratings yet

- SE AssignmentAsPerSPPUDocument2 pagesSE AssignmentAsPerSPPUkedarNo ratings yet

- 31 - Enano-Bote v. AlvarezDocument4 pages31 - Enano-Bote v. AlvarezWilfredo Guerrero IIINo ratings yet

- HD RegulationDocument78 pagesHD RegulationzamsiranNo ratings yet

- Introduction To Management AccountingDocument37 pagesIntroduction To Management AccountingVin me.No ratings yet

- Sri Lanka Media Audience Study 2019Document64 pagesSri Lanka Media Audience Study 2019methlalNo ratings yet

- Objectives of Marketing ProcessDocument6 pagesObjectives of Marketing ProcessMamta VermaNo ratings yet

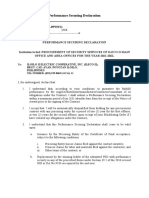

- Performance Securing Declaration 2021Document2 pagesPerformance Securing Declaration 2021Mike Francis F GubuanNo ratings yet