You might also like

- The Mean Variance Portfolio TheoryDocument32 pagesThe Mean Variance Portfolio TheoryEbenezerNo ratings yet

- JWCh07 PDFDocument29 pagesJWCh07 PDF007featherNo ratings yet

- Institutional Finance: Lecture 05: Portfolio Choice, CAPM, Black-LittermanDocument45 pagesInstitutional Finance: Lecture 05: Portfolio Choice, CAPM, Black-LittermandesbiauxNo ratings yet

- Financial Economics: Optimal Choice: Mean-Variance and Portfolio TheoryDocument77 pagesFinancial Economics: Optimal Choice: Mean-Variance and Portfolio TheoryVi LinhNo ratings yet

- International Portfolio DiversificationDocument34 pagesInternational Portfolio DiversificationGaurav KumarNo ratings yet

- Lecture 3Document29 pagesLecture 3isteaq ahamedNo ratings yet

- Lecture 5 Optimal Risky PortfoliosDocument28 pagesLecture 5 Optimal Risky PortfoliosLuisLoNo ratings yet

- Chapter 7 Portfolio Theory: 1 Introduction and OverviewDocument38 pagesChapter 7 Portfolio Theory: 1 Introduction and OverviewEbenezerMebrateNo ratings yet

- Efficient Diversification: Mcgraw-Hill/IrwinDocument41 pagesEfficient Diversification: Mcgraw-Hill/IrwinAhmed El KhateebNo ratings yet

- Formula Sheet for MidtermDocument1 pageFormula Sheet for MidtermrawanelayusNo ratings yet

- Stat 366 Lab 3 Solutions PDF summaryDocument6 pagesStat 366 Lab 3 Solutions PDF summaryMotseilekgoaNo ratings yet

- Revision Questions and Classwork 7Document11 pagesRevision Questions and Classwork 7Sams HaiderNo ratings yet

- Hinkley 1969Document6 pagesHinkley 1969Raúl Díez GarcíaNo ratings yet

- 6 Modern Portfolio TheoryDocument78 pages6 Modern Portfolio Theorysupeng huangNo ratings yet

- ClassdemoDocument3 pagesClassdemoVishnu GaurNo ratings yet

- Introduction To Portfolio Selection and Capital Market Theory: Static AnalysisDocument97 pagesIntroduction To Portfolio Selection and Capital Market Theory: Static AnalysisAkshay TyagiNo ratings yet

- Financial Market Analysis (Fmax) : "Asset Allocation and Diversification"Document52 pagesFinancial Market Analysis (Fmax) : "Asset Allocation and Diversification"Beka GurgenidzeNo ratings yet

- Investment TheoryDocument29 pagesInvestment Theorypgdm23samamalNo ratings yet

- Multiple Regression Analysis (MLR)Document28 pagesMultiple Regression Analysis (MLR)Samara ChaudhuryNo ratings yet

- (CFA) (2015) (L2) 06 V3 - 2015 - 二级强化班 - 组合1Document102 pages(CFA) (2015) (L2) 06 V3 - 2015 - 二级强化班 - 组合1Phyllis YenNo ratings yet

- BMAN71171 Portfolio Investment Lecture 2a: Intuition On Portfolio Selection Chris Godfrey (Christopher - Godfrey@manchester - Ac.uk)Document27 pagesBMAN71171 Portfolio Investment Lecture 2a: Intuition On Portfolio Selection Chris Godfrey (Christopher - Godfrey@manchester - Ac.uk)Nazmul H. PalashNo ratings yet

- Portfolio TheoryDocument48 pagesPortfolio Theoryzhongyi87No ratings yet

- Investment Science Solutions To Suggested Problems: Dr. James A. TzitzourisDocument5 pagesInvestment Science Solutions To Suggested Problems: Dr. James A. Tzitzouris曾一晋No ratings yet

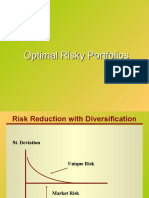

- Risk Reduction with DiversificationDocument23 pagesRisk Reduction with DiversificationJay GuptaNo ratings yet

- Markowitz Portfolio Analysis: The Demonstration Portfolio ProblemDocument10 pagesMarkowitz Portfolio Analysis: The Demonstration Portfolio ProblemvlaciarNo ratings yet

- CH 7 Efficient Diversification (Part 1) (W2024)Document38 pagesCH 7 Efficient Diversification (Part 1) (W2024)Graeme WilhelmNo ratings yet

- Lecture One: Introduction To Power System Yoseph MekonnenDocument23 pagesLecture One: Introduction To Power System Yoseph MekonnenKalab TenadegNo ratings yet

- Markowitz Models and CAPMDocument17 pagesMarkowitz Models and CAPMVinay DuttaNo ratings yet

- Thick Lenses Systems: Fulvio Andres CallegariDocument20 pagesThick Lenses Systems: Fulvio Andres Callegariammar tambunanNo ratings yet

- 15.401 Recitation 15.401 Recitation: 6: Portfolio ChoiceDocument33 pages15.401 Recitation 15.401 Recitation: 6: Portfolio ChoiceJohnNo ratings yet

- Another Proof of 6ζ (2) =π^2 Using Double Integrals - Daniele Ritelli (AMM, v120, n7, 2013)Document5 pagesAnother Proof of 6ζ (2) =π^2 Using Double Integrals - Daniele Ritelli (AMM, v120, n7, 2013)Leandro AzNo ratings yet

- Math 213a: Homework 2: Vinh-Kha Le September 2018Document10 pagesMath 213a: Homework 2: Vinh-Kha Le September 2018vinhkhaleNo ratings yet

- Ch12-Dennis G. Zill - Warren S. Wright-Advanced Engineering Mathematics-Jones - Amp - Bartlett Learning (2012)Document34 pagesCh12-Dennis G. Zill - Warren S. Wright-Advanced Engineering Mathematics-Jones - Amp - Bartlett Learning (2012)Nguyễn Chí NguyệnNo ratings yet

- Bilaplacians problems with a sign-changing coefficient: Abstract. We investigate the properties of the operator ∆ (σ∆Document31 pagesBilaplacians problems with a sign-changing coefficient: Abstract. We investigate the properties of the operator ∆ (σ∆Mehtar YNo ratings yet

- Multiple Regression Analysis ExplainedDocument28 pagesMultiple Regression Analysis ExplainedfaignacioNo ratings yet

- Rasprsenje CL 1Document7 pagesRasprsenje CL 1zhoe_boeNo ratings yet

- Singh Studentsolutions Misc4Document36 pagesSingh Studentsolutions Misc4Debdutta ChatterjeeNo ratings yet

- ComplexElectrostatics PDFDocument19 pagesComplexElectrostatics PDFjuan CarlosNo ratings yet

- Lecture 4Document35 pagesLecture 4Nart-Ahia GideonNo ratings yet

- Probability and Stochastic Processes: A Friendly IntroductionDocument6 pagesProbability and Stochastic Processes: A Friendly IntroductionqscvbqscvbNo ratings yet

- Portfolio Theory PresentationDocument50 pagesPortfolio Theory PresentationAkshatNo ratings yet

- ACTL1001, Week 8: - Risk Pooling and Diversification - Correlation and CovarianceDocument26 pagesACTL1001, Week 8: - Risk Pooling and Diversification - Correlation and CovariancejlosamNo ratings yet

- Hydraulics Lab ManualDocument45 pagesHydraulics Lab ManualRohith BommalaNo ratings yet

- RLM 2016 027 004 02Document18 pagesRLM 2016 027 004 02Luis FuentesNo ratings yet

- The Finite Element Method For One-Dimensional ProblemsDocument13 pagesThe Finite Element Method For One-Dimensional ProblemsAlireza PahlevanzadehNo ratings yet

- Markowitz Portfolio SelectionDocument29 pagesMarkowitz Portfolio SelectionJessicaGonzalesNo ratings yet

- Regression Analysis ExplainedDocument28 pagesRegression Analysis ExplainedGidisa LachisaNo ratings yet

- Ejercicio Edp ExpoDocument1 pageEjercicio Edp Exposantiago floresNo ratings yet

- E e e e e E: e e H e e H e e HDocument6 pagesE e e e e E: e e H e e H e e HAsdcxzNo ratings yet

- CH 03Document28 pagesCH 03Kathiravan GopalanNo ratings yet

- FE - Portfolio Returns and Market IndexesDocument11 pagesFE - Portfolio Returns and Market IndexesJUAN BERMUDEZNo ratings yet

- 2-Single Vs Multi Polarization Interferometry PDFDocument24 pages2-Single Vs Multi Polarization Interferometry PDFadre traNo ratings yet

- Week 6Document67 pagesWeek 6Aaditya KumarNo ratings yet

- Mutual CouplingDocument6 pagesMutual Couplingjagadish mNo ratings yet

- Formulas Two SamplesDocument1 pageFormulas Two SamplesNguyễn TrangNo ratings yet

- Multiple Regression Analysis: y + X + X + - . - X + UDocument43 pagesMultiple Regression Analysis: y + X + X + - . - X + UMike JonesNo ratings yet

- Hydro 1 Module 2Document13 pagesHydro 1 Module 2Jericho Alfred Rullog Sapitula100% (1)

- Ricardian Models: This Example Is Based On One From Tim KehoeDocument14 pagesRicardian Models: This Example Is Based On One From Tim KehoeRaja AhmedNo ratings yet

- FMTZDocument6 pagesFMTZUtkarsh ChoudharyNo ratings yet

- Tables of the Function w (z)- e-z2 ? ex2 dx: Mathematical Tables Series, Vol. 27From EverandTables of the Function w (z)- e-z2 ? ex2 dx: Mathematical Tables Series, Vol. 27No ratings yet

- Gambles, Stochastic Dominance, EU Theory AlternativesDocument32 pagesGambles, Stochastic Dominance, EU Theory AlternativesEbenezerNo ratings yet

- Operational Risk Exam PackDocument33 pagesOperational Risk Exam PackEbenezer100% (2)

- Study+school+slides Market Risk ManagementDocument64 pagesStudy+school+slides Market Risk ManagementEbenezerNo ratings yet

- Topic: Capital Structure Theory: Honours Financial Economics Lectures Notes 2017 Lecturer: Tendai Gwatidzo, PHDDocument19 pagesTopic: Capital Structure Theory: Honours Financial Economics Lectures Notes 2017 Lecturer: Tendai Gwatidzo, PHDEbenezerNo ratings yet

- CCAPM EPP 2017 Final SlidesDocument52 pagesCCAPM EPP 2017 Final SlidesEbenezerNo ratings yet

- Financial Risk ManagementDocument41 pagesFinancial Risk ManagementEbenezerNo ratings yet

- Honours Financial Economics: InstructionsDocument3 pagesHonours Financial Economics: InstructionsEbenezerNo ratings yet

- Understanding the Capital Asset Pricing Model (CAPMDocument49 pagesUnderstanding the Capital Asset Pricing Model (CAPMEbenezerNo ratings yet

- CCAPM EPP 2017 Final SlidesDocument52 pagesCCAPM EPP 2017 Final SlidesEbenezerNo ratings yet

- Black FlagsDocument12 pagesBlack Flagsmrashid_usmanNo ratings yet

- Drug Study (Pe)Document15 pagesDrug Study (Pe)Jobelle AcenaNo ratings yet

- Modernist PoetryDocument14 pagesModernist PoetryFaisal JahangirNo ratings yet

- Olberding - Other People DieDocument19 pagesOlberding - Other People DiefelmmandoNo ratings yet

- Engleza Clasa 1Document4 pagesEngleza Clasa 1Ioana BotarNo ratings yet

- Eating Disorders Reading AssignmentDocument2 pagesEating Disorders Reading AssignmentNasratullah sahebzadaNo ratings yet

- Volleyball BOTTOM LINE ESSAY TEMPLATEDocument2 pagesVolleyball BOTTOM LINE ESSAY TEMPLATEViness Pearl Kristina R. AcostoNo ratings yet

- 21st Century Literature Grade 11 21st Century Literature Grade 11 21st Century Literature Grade 11 CompressDocument75 pages21st Century Literature Grade 11 21st Century Literature Grade 11 21st Century Literature Grade 11 Compressdesly jane sianoNo ratings yet

- F Chart Method Klein Duffie BeckmanDocument10 pagesF Chart Method Klein Duffie BeckmansergioNo ratings yet

- Qatar Airways FS 31 March 2019 (En)Document62 pagesQatar Airways FS 31 March 2019 (En)HusSam Ud DinNo ratings yet

- Brown v. Board of EducationDocument1 pageBrown v. Board of EducationSam TaborNo ratings yet

- Amity School of Communication: BA (J&MC), Semester-1 Basics of Print Media Neha BhagatDocument10 pagesAmity School of Communication: BA (J&MC), Semester-1 Basics of Print Media Neha BhagatYash TiwariNo ratings yet

- Legal Counselling defined in broad and narrow sensesDocument5 pagesLegal Counselling defined in broad and narrow sensesRegie Rey AgustinNo ratings yet

- REVLONDocument20 pagesREVLONUrika RufinNo ratings yet

- The Tracking Shot in Kapo Serge Daney Senses of CinemaDocument22 pagesThe Tracking Shot in Kapo Serge Daney Senses of CinemaMarcos GonzálezNo ratings yet

- 3 Affect Regulation, Mentalization, and The Development of The Self (Peter Fonagy, Gyorgy Gergely, Elliot L. Jurist Etc.) - 211-259Document49 pages3 Affect Regulation, Mentalization, and The Development of The Self (Peter Fonagy, Gyorgy Gergely, Elliot L. Jurist Etc.) - 211-259Sergio Andres Rico AvendanoNo ratings yet

- De Onde Eu Te VejoDocument2 pagesDe Onde Eu Te VejoBianca Oliveira CoelhoNo ratings yet

- American Ceramic: SocietyDocument8 pagesAmerican Ceramic: SocietyPhi TiêuNo ratings yet

- RitzeDocument4 pagesRitzeLalai IskolatongNo ratings yet

- Mock Test 2Document8 pagesMock Test 2Niranjan BeheraNo ratings yet

- Digest Aswat Vs GalidoDocument3 pagesDigest Aswat Vs GalidoLeo Felicilda100% (1)

- Infoplc Net Sitrain 15 Documenting Saving ArchivingDocument26 pagesInfoplc Net Sitrain 15 Documenting Saving ArchivingBijoy RoyNo ratings yet

- 2023 - 002075129500001316312023 - Error CJALDocument7 pages2023 - 002075129500001316312023 - Error CJALFabian Quiroz VergelNo ratings yet

- Lecture NotesDocument12 pagesLecture NotesSabina Ioana AioneseiNo ratings yet

- EBM CasesDocument1 pageEBM CasesdnaritaNo ratings yet

- Marketing Research An Applied Orientation 7th Edition Malhotra Solutions ManualDocument33 pagesMarketing Research An Applied Orientation 7th Edition Malhotra Solutions Manualtitusotis7s8yba100% (27)

- Chapter 5 - Strategic Human Resource ManagementDocument19 pagesChapter 5 - Strategic Human Resource ManagementmaiaaaaNo ratings yet

- Notes in Readings in Philippine History: Act of Proclamation of Independence of The Filipino PeopleDocument4 pagesNotes in Readings in Philippine History: Act of Proclamation of Independence of The Filipino PeopleAiris Ramos AgillonNo ratings yet

- CH 05 Wooldridge 5e PPTDocument8 pagesCH 05 Wooldridge 5e PPTMomal IshaqNo ratings yet

- Ib Q OnlyDocument1 pageIb Q Onlyapi-529669983No ratings yet