You might also like

- (PDF) The Subtle Art of Not Giving A FuckDocument16 pages(PDF) The Subtle Art of Not Giving A FuckGvantsa Morchadze80% (5)

- SDM Case Analysis: ABB and Caterpillar (A) : Key Account ManagementDocument5 pagesSDM Case Analysis: ABB and Caterpillar (A) : Key Account Managementmahtaabk100% (1)

- OpenText Vendor Invoice Management For SAP Solutions 16.3.3 - Configuration Guide English (VIM160303-CGD-En-02)Document906 pagesOpenText Vendor Invoice Management For SAP Solutions 16.3.3 - Configuration Guide English (VIM160303-CGD-En-02)shivangi guptaNo ratings yet

- Compliance Monitoring ReportDocument6 pagesCompliance Monitoring ReportJuel MemitaNo ratings yet

- Discovering New Points of DifferentiationDocument10 pagesDiscovering New Points of DifferentiationAkshay DeshpandeNo ratings yet

- ლექცია 1 - Analyzing Economic Problems and MicroeconomicsDocument17 pagesლექცია 1 - Analyzing Economic Problems and MicroeconomicsJUST LETNo ratings yet

- Notes - Chapter 6Document4 pagesNotes - Chapter 6Aarav GuptaNo ratings yet

- S1 PPTX Capitulo 6 EstudiantesDocument16 pagesS1 PPTX Capitulo 6 EstudiantesKrissya Masis MoraNo ratings yet

- Consumption Savings Investment. ParadoxDocument46 pagesConsumption Savings Investment. ParadoxChristine Joy LanabanNo ratings yet

- Keynesian MultiplierDocument11 pagesKeynesian MultiplierAvinaw KumarNo ratings yet

- Creating An Environment For Growth and Prosperity: Full Length Text - Macro Only TextDocument40 pagesCreating An Environment For Growth and Prosperity: Full Length Text - Macro Only TextGvantsa MorchadzeNo ratings yet

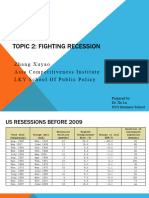

- Week 2 Fighting RecessionDocument42 pagesWeek 2 Fighting Recessiondaisyruyu2001No ratings yet

- Lecture 3 - Neoclassic Vs Keynes - Keynesian Cross - Multiplier - Money MarketDocument45 pagesLecture 3 - Neoclassic Vs Keynes - Keynesian Cross - Multiplier - Money MarketbenskantorNo ratings yet

- The Economic Approach: Full Length Text - Micro Only Text - Macro Only Text - PartDocument20 pagesThe Economic Approach: Full Length Text - Micro Only Text - Macro Only Text - PartGvantsa MorchadzeNo ratings yet

- Chapter Three: Macro Economics: 1. Business CycleDocument9 pagesChapter Three: Macro Economics: 1. Business CycleTewodros TadesseNo ratings yet

- Introduction of MacroeconomicsDocument25 pagesIntroduction of MacroeconomicsNaeem AhmedNo ratings yet

- Introduction To Macroeconomics: Powerpoint Slides Prepared By: Andreea Chiritescu Eastern Illinois UniversityDocument23 pagesIntroduction To Macroeconomics: Powerpoint Slides Prepared By: Andreea Chiritescu Eastern Illinois Universitymimi96No ratings yet

- Macroeconomics: Theory and Policy: Anindya S. Chakrabarti Indian Institute of Management, AhmedabadDocument23 pagesMacroeconomics: Theory and Policy: Anindya S. Chakrabarti Indian Institute of Management, AhmedabadvineethNo ratings yet

- Keynesian Vs Classical Macroeconomic ModelDocument47 pagesKeynesian Vs Classical Macroeconomic ModelhongphakdeyNo ratings yet

- CH 10 Lo - Economic - InstabilityDocument26 pagesCH 10 Lo - Economic - Instabilitytariku1234No ratings yet

- Mankiw PrinciplesOfEconomics 10e PPT CH01Document41 pagesMankiw PrinciplesOfEconomics 10e PPT CH01Quỳnh HươngNo ratings yet

- KWe3 Macro Ch6SelectedDocument26 pagesKWe3 Macro Ch6SelectedMichael DCNo ratings yet

- Lecture 20Document25 pagesLecture 20waleed.link96No ratings yet

- Recovering For A Recession and Some Possible ProblemsDocument10 pagesRecovering For A Recession and Some Possible ProblemsAbdoukadirr SambouNo ratings yet

- CHAP19 Micro Foundation Mankiw 10edDocument55 pagesCHAP19 Micro Foundation Mankiw 10edAkmal FadhlurrahmanNo ratings yet

- Phases of Economic DevelopmentDocument21 pagesPhases of Economic DevelopmentJamesdomingoNo ratings yet

- Aggregate Demand & Keynesian Multiplier PDFDocument6 pagesAggregate Demand & Keynesian Multiplier PDFArunabh ChoudhuryNo ratings yet

- Policy Economics - 7nov2022Document39 pagesPolicy Economics - 7nov2022Nency MosesNo ratings yet

- Introduction To MacroeconomicsDocument24 pagesIntroduction To MacroeconomicsEchizen RyomaNo ratings yet

- Keynasian Theory of EmploymentDocument29 pagesKeynasian Theory of Employmentsunita agrawalNo ratings yet

- Consumption and SavingDocument6 pagesConsumption and Savingmah rukhNo ratings yet

- Economics 12th Edition Arnold Solutions Manual 1Document28 pagesEconomics 12th Edition Arnold Solutions Manual 1gregorydyercgspwbjekr100% (20)

- Economics 12th Edition Arnold Solutions Manual 1Document19 pagesEconomics 12th Edition Arnold Solutions Manual 1charles100% (35)

- Lesson 3 - Monetarist-New Classical View of LRASDocument12 pagesLesson 3 - Monetarist-New Classical View of LRASandrewwang417No ratings yet

- Introduction VT2024Document39 pagesIntroduction VT2024aleema anjumNo ratings yet

- Chapter 15 RizalDocument39 pagesChapter 15 RizalEdriel DaquioagNo ratings yet

- One Planet Economics: Green Growth, Steady State, or Degrowth?Document38 pagesOne Planet Economics: Green Growth, Steady State, or Degrowth?j.k.steinbergerNo ratings yet

- Session1 Introduction PDFDocument19 pagesSession1 Introduction PDFANJULI AGARWALNo ratings yet

- WINSEMFY2022-23 TLAW166L TH CH2022232300383 Reference Material I 06-03-2023 Macro MultiplierDocument17 pagesWINSEMFY2022-23 TLAW166L TH CH2022232300383 Reference Material I 06-03-2023 Macro MultiplierHaresh .sNo ratings yet

- Principles of Islamic Economics - 7th LectureDocument21 pagesPrinciples of Islamic Economics - 7th LectureNur HazimahNo ratings yet

- Income Determination in Short Run: Basic Model: Ae Y AE (C+I) Ae YDocument31 pagesIncome Determination in Short Run: Basic Model: Ae Y AE (C+I) Ae YAman Singh RajputNo ratings yet

- Economics 11Th Edition Arnold Solutions Manual Full Chapter PDFDocument36 pagesEconomics 11Th Edition Arnold Solutions Manual Full Chapter PDFjoshua.king500100% (12)

- Economics 11th Edition Arnold Solutions Manual 1Document18 pagesEconomics 11th Edition Arnold Solutions Manual 1jackqueline100% (39)

- Economics 11th Edition Arnold Solutions Manual 1Document36 pagesEconomics 11th Edition Arnold Solutions Manual 1shirleycoopercmkgzintjx100% (26)

- Chapter 3: Business Cycle, Inflation and UnemploymentDocument28 pagesChapter 3: Business Cycle, Inflation and UnemploymentChristian Jumao-as MendozaNo ratings yet

- Chapter 1 - Introduction To MacroeconomicsDocument11 pagesChapter 1 - Introduction To Macroeconomics2022890872No ratings yet

- Chapter 4 EconomicsforInvestmentDocument37 pagesChapter 4 EconomicsforInvestmentTử Đằng NguyễnNo ratings yet

- Keynes Theory of Deficit SpendingDocument14 pagesKeynes Theory of Deficit Spendingdipu francyNo ratings yet

- BUSN11 KellyWilliams Ch02Document30 pagesBUSN11 KellyWilliams Ch02Christopher KragnesNo ratings yet

- AE Principles of EcoDocument29 pagesAE Principles of EcoKurt Kurt XaiveryNo ratings yet

- Mankiw PrinciplesOfEconomics 10e PPT CH22Document55 pagesMankiw PrinciplesOfEconomics 10e PPT CH22ngocle071125No ratings yet

- Macroeconomics 13th Edition Arnold Solutions Manual Full Chapter PDFDocument40 pagesMacroeconomics 13th Edition Arnold Solutions Manual Full Chapter PDFJosephWebbemwiy100% (11)

- Macroeconomics 13th Edition Arnold Solutions ManualDocument19 pagesMacroeconomics 13th Edition Arnold Solutions Manualdencuongpow5100% (25)

- ECON7002: Unemployment and InflationDocument65 pagesECON7002: Unemployment and InflationNima MoaddeliNo ratings yet

- Macro Ecoomic Analysis For Business DecisionsDocument22 pagesMacro Ecoomic Analysis For Business DecisionsVrkNo ratings yet

- CH5 Economic Instability - A Critique of The Self-Regulating EconomyDocument37 pagesCH5 Economic Instability - A Critique of The Self-Regulating EconomyTiviyaNo ratings yet

- CM 3c 3d - 3e Unemployment - Aggregate Supply and DemandDocument69 pagesCM 3c 3d - 3e Unemployment - Aggregate Supply and Demandbojan GeorgievskiNo ratings yet

- 113 Unit VDocument61 pages113 Unit V21002hadiNo ratings yet

- Lecture 2 Chapter 3Document37 pagesLecture 2 Chapter 3chenboontaiNo ratings yet

- What Is The Investment MultiplierDocument4 pagesWhat Is The Investment MultiplierArpita DasNo ratings yet

- Topic 1 - Consumption FunctionDocument13 pagesTopic 1 - Consumption Functionreuben kawongaNo ratings yet

- Business Cycles 10.10.2019Document21 pagesBusiness Cycles 10.10.2019Pradeep RaviNo ratings yet

- Econ Week 13 Savings and The Financial SystemDocument35 pagesEcon Week 13 Savings and The Financial SystemMeeka CalimagNo ratings yet

- Lessons From The Japanese Experience: Full Length Text - Macro Only TextDocument28 pagesLessons From The Japanese Experience: Full Length Text - Macro Only TextGvantsa MorchadzeNo ratings yet

- (Zhongguo Zong Jiao Ji Ben Qing Kuang Cong Shu) Haicheng Ling - Buddhism in China-China Intercontinental Press (2005)Document280 pages(Zhongguo Zong Jiao Ji Ben Qing Kuang Cong Shu) Haicheng Ling - Buddhism in China-China Intercontinental Press (2005)Gvantsa Morchadze100% (1)

- Lessons From The Great Depression: Full Length Text - Macro Only Text - Micro Only Text - PartDocument45 pagesLessons From The Great Depression: Full Length Text - Macro Only Text - Micro Only Text - PartGvantsa MorchadzeNo ratings yet

- The Journal of The International Assosiation of Buddhist Studies.Document16 pagesThe Journal of The International Assosiation of Buddhist Studies.Gvantsa MorchadzeNo ratings yet

- Are We Running Out of Resources?: Full Length Text - Micro Only TextDocument22 pagesAre We Running Out of Resources?: Full Length Text - Micro Only TextGvantsa MorchadzeNo ratings yet

- The Economics of Health Care: Full Length Text - Micro Only TextDocument25 pagesThe Economics of Health Care: Full Length Text - Micro Only TextGvantsa MorchadzeNo ratings yet

- Do Labor Unions Increase The Wages of Workers?: Full Length Text - Micro Only TextDocument24 pagesDo Labor Unions Increase The Wages of Workers?: Full Length Text - Micro Only TextGvantsa MorchadzeNo ratings yet

- Earnings Differences Between Men and Women: Full Length Text - Micro Only TextDocument12 pagesEarnings Differences Between Men and Women: Full Length Text - Micro Only TextGvantsa MorchadzeNo ratings yet

- School Choice:: Can It Improve The Quality of Education in America?Document20 pagesSchool Choice:: Can It Improve The Quality of Education in America?Gvantsa MorchadzeNo ratings yet

- The Federal Budget and The National Debt: Full Length Text - Macro Only TextDocument23 pagesThe Federal Budget and The National Debt: Full Length Text - Macro Only TextGvantsa MorchadzeNo ratings yet

- The Internet: How Is It Changing The Economy?: Full Length Text - Micro Only Text - Macro Only Text - PartDocument19 pagesThe Internet: How Is It Changing The Economy?: Full Length Text - Micro Only Text - Macro Only Text - PartGvantsa MorchadzeNo ratings yet

- Income Inequality and Poverty: Full Length Text - Micro Only TextDocument21 pagesIncome Inequality and Poverty: Full Length Text - Micro Only TextGvantsa MorchadzeNo ratings yet

- Its Function, Performance, and Potential As An Investment OpportunityDocument20 pagesIts Function, Performance, and Potential As An Investment OpportunityGvantsa MorchadzeNo ratings yet

- The Economics of Social Security: Full Length Text - Micro Only Text - Macro Only Text - PartDocument25 pagesThe Economics of Social Security: Full Length Text - Micro Only Text - Macro Only Text - PartGvantsa MorchadzeNo ratings yet

- Price-Searcher Markets With Low Entry Barriers: Full Length Text - Micro Only TextDocument31 pagesPrice-Searcher Markets With Low Entry Barriers: Full Length Text - Micro Only TextGvantsa MorchadzeNo ratings yet

- Investment, The Capital Market, and The Wealth of Nations: Full Length Text - Micro Only TextDocument34 pagesInvestment, The Capital Market, and The Wealth of Nations: Full Length Text - Micro Only TextGvantsa MorchadzeNo ratings yet

- The Supply and Demand For Productive Resources: Full Length Text - Micro Only TextDocument32 pagesThe Supply and Demand For Productive Resources: Full Length Text - Micro Only TextGvantsa MorchadzeNo ratings yet

- Price Takers and The Competitive Process: Full Length Text - Micro Only TextDocument42 pagesPrice Takers and The Competitive Process: Full Length Text - Micro Only TextGvantsa MorchadzeNo ratings yet

- Institutions, Policies, and Cross-Country Differences in Income and GrowthDocument61 pagesInstitutions, Policies, and Cross-Country Differences in Income and GrowthGvantsa MorchadzeNo ratings yet

- Price-Searcher Markets With High Entry Barriers: Full Length Text - Micro Only TextDocument39 pagesPrice-Searcher Markets With High Entry Barriers: Full Length Text - Micro Only TextGvantsa MorchadzeNo ratings yet

- Consumer Choice and Elasticity: Full Length Text - Micro Only TextDocument35 pagesConsumer Choice and Elasticity: Full Length Text - Micro Only TextGvantsa MorchadzeNo ratings yet

- Modern Macroeconomics and Monetary Policy: Full Length Text - Macro Only TextDocument46 pagesModern Macroeconomics and Monetary Policy: Full Length Text - Macro Only TextGvantsa MorchadzeNo ratings yet

- Earnings, Productivity, and The Job Market: Full Length Text - Micro Only TextDocument25 pagesEarnings, Productivity, and The Job Market: Full Length Text - Micro Only TextGvantsa MorchadzeNo ratings yet

- Economic Fluctuations, Unemployment, and Inflation: Full Length Text - Macro Only TextDocument37 pagesEconomic Fluctuations, Unemployment, and Inflation: Full Length Text - Macro Only TextGvantsa MorchadzeNo ratings yet

- Taking The Nation's Economic Pulse: Full Length Text - Macro Only TextDocument38 pagesTaking The Nation's Economic Pulse: Full Length Text - Macro Only TextGvantsa MorchadzeNo ratings yet

- Creating An Environment For Growth and Prosperity: Full Length Text - Macro Only TextDocument40 pagesCreating An Environment For Growth and Prosperity: Full Length Text - Macro Only TextGvantsa MorchadzeNo ratings yet

- An Introduction To Basic Macroeconomic Markets: Full Length Text - Macro Only TextDocument56 pagesAn Introduction To Basic Macroeconomic Markets: Full Length Text - Macro Only TextGvantsa MorchadzeNo ratings yet

- 13 Calculus 7th Edition Textbook SolutionsDocument1 page13 Calculus 7th Edition Textbook SolutionsAbraao Zuza CostaNo ratings yet

- BCAS Membership FormDocument1 pageBCAS Membership FormRichi MonaniNo ratings yet

- PBI - Unit 4 & 5Document70 pagesPBI - Unit 4 & 5AdarshPanickerNo ratings yet

- Portfolio and Services - MuradDocument22 pagesPortfolio and Services - Muradronica24sethNo ratings yet

- Brand Audit ChecklistDocument2 pagesBrand Audit ChecklistPasek KamajayaNo ratings yet

- SAQA - 10135 - Facilitator GuideDocument34 pagesSAQA - 10135 - Facilitator GuideTalentNo ratings yet

- Research Proposal Applied Research Methods: Submitted To: Mr. Waqar Akbar Submitted By: Harris Kamran (1735154-Section F)Document8 pagesResearch Proposal Applied Research Methods: Submitted To: Mr. Waqar Akbar Submitted By: Harris Kamran (1735154-Section F)AhmadNo ratings yet

- Writ of Quo Warranto MR. COOPER RevisedDocument7 pagesWrit of Quo Warranto MR. COOPER RevisedRosetta Rashid’s McCowan El0% (1)

- UN Transnational Organized Crime in Southeast Asia - Evolution, Growth and Impact SEA - TOCTA - 2019 - WebDocument194 pagesUN Transnational Organized Crime in Southeast Asia - Evolution, Growth and Impact SEA - TOCTA - 2019 - WebA ChNo ratings yet

- Corporate GovernanceDocument110 pagesCorporate GovernanceRISHABH GUPTANo ratings yet

- Career Objective:: U BalaraghavanDocument4 pagesCareer Objective:: U BalaraghavanubraghuNo ratings yet

- UNDP Bhopal Consultation Report FINAL DigiPrintDocument32 pagesUNDP Bhopal Consultation Report FINAL DigiPrinthusarilNo ratings yet

- Islamic Financing OriginationDocument8 pagesIslamic Financing OriginationTsomondo KudakwasheNo ratings yet

- Chapter - 2 - Acctg Concepts and PrinciplesDocument24 pagesChapter - 2 - Acctg Concepts and PrinciplesPortia AbestanoNo ratings yet

- Advanced Referral Skills WorkshopDocument18 pagesAdvanced Referral Skills WorkshopnNo ratings yet

- Outage Management System (OMS) Market - Current Impact To Make Big Changes - General Electric, Oracle, SiemensDocument20 pagesOutage Management System (OMS) Market - Current Impact To Make Big Changes - General Electric, Oracle, SiemenskhoshnamaNo ratings yet

- Changhong - WikipediaDocument12 pagesChanghong - Wikipediaayanmehdi96No ratings yet

- Tanggung Jawab Direksi Berdasarkan Prinsip Fiduciary Duties Dalam Perseroan TerbatasDocument6 pagesTanggung Jawab Direksi Berdasarkan Prinsip Fiduciary Duties Dalam Perseroan TerbatasciciNo ratings yet

- Tourism and Development Planning: Slide 9.1Document19 pagesTourism and Development Planning: Slide 9.1English TimeNo ratings yet

- Business and Impact Planning For Social Enterprises (BIPSE) : Prof. Muneza Kagzi T A Pai Management InstituteDocument13 pagesBusiness and Impact Planning For Social Enterprises (BIPSE) : Prof. Muneza Kagzi T A Pai Management Institutekshitiz singhNo ratings yet

- Standard STD 5051,16: Text Marking On PartsDocument50 pagesStandard STD 5051,16: Text Marking On PartsRobertoNo ratings yet

- Difference Between LLP and CompanyDocument20 pagesDifference Between LLP and CompanyAvinash LoharNo ratings yet

- Farparcor 2 Chapter 1 Exercises Problem AnswersDocument10 pagesFarparcor 2 Chapter 1 Exercises Problem AnswersWillnie Shane LabaroNo ratings yet

- 03 - Anderson 2009 - Fiscal FederalismDocument81 pages03 - Anderson 2009 - Fiscal FederalismkevinNo ratings yet

- Financial Technology (Fintech) - Its Uses and Impact On Our LivesDocument10 pagesFinancial Technology (Fintech) - Its Uses and Impact On Our Livessharafernando2No ratings yet

- Account Statement From 1 May 2021 To 11 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument5 pagesAccount Statement From 1 May 2021 To 11 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balance1382aceNo ratings yet