You might also like

- The Hertz Corporation Case Study AnalysisDocument27 pagesThe Hertz Corporation Case Study AnalysisRahul AgarwalNo ratings yet

- Technical Note On LBO Valuation and Modeling - 150309 - 4!10!2015 - SAMPLEDocument30 pagesTechnical Note On LBO Valuation and Modeling - 150309 - 4!10!2015 - SAMPLEJayant Sharma100% (1)

- Week 1 Assignment Fundamental Principles in TaxationDocument5 pagesWeek 1 Assignment Fundamental Principles in TaxationIan Paolo CaylanNo ratings yet

- Vista Equity Partners - 2017 Analyst PositionDocument4 pagesVista Equity Partners - 2017 Analyst PositionJonathan StewartNo ratings yet

- AAFR by Sir Nasir Abbas BOOKDocument665 pagesAAFR by Sir Nasir Abbas BOOKAbdul WaheedNo ratings yet

- Corporate Sustainability Practices - Dayana MasturaDocument14 pagesCorporate Sustainability Practices - Dayana MasturaDayana MasturaNo ratings yet

- Module 4 - ImpairmentDocument5 pagesModule 4 - ImpairmentLuiNo ratings yet

- Corporate Finance - Mergers and Acquisitions - Strategic Issues - Dayana MasturaDocument19 pagesCorporate Finance - Mergers and Acquisitions - Strategic Issues - Dayana MasturaDayana MasturaNo ratings yet

- Internal Control of Fixed Assets: A Controller and Auditor's GuideFrom EverandInternal Control of Fixed Assets: A Controller and Auditor's GuideRating: 4 out of 5 stars4/5 (1)

- Corporate Sustainability - Stakeholder and Stewardship Theory - Dayana MasturaDocument18 pagesCorporate Sustainability - Stakeholder and Stewardship Theory - Dayana MasturaDayana Mastura100% (1)

- Audit of CBS EnvironmentDocument28 pagesAudit of CBS EnvironmentPatricia UkemNo ratings yet

- IAS 36 Impairment of AssetsDocument22 pagesIAS 36 Impairment of AssetsZeeshan Mahmood100% (1)

- Corporate Finance - Business Valuations - Dayana MasturaDocument14 pagesCorporate Finance - Business Valuations - Dayana MasturaDayana MasturaNo ratings yet

- Pettet, Lowry & Reisberg's Company Law '12Document657 pagesPettet, Lowry & Reisberg's Company Law '12mamahannatuadamu100% (1)

- CORPORATE SUSTAINABILITY - Evolution of Corporate Reporting - Dayana MasturaDocument29 pagesCORPORATE SUSTAINABILITY - Evolution of Corporate Reporting - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Finance - Capital Structure - Dayana MasturaDocument12 pagesCorporate Finance - Capital Structure - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Sustainability - Environmental Accounting - Dayana MasturaDocument24 pagesCorporate Sustainability - Environmental Accounting - Dayana MasturaDayana MasturaNo ratings yet

- Lec1 - Introduction To AccountingDocument47 pagesLec1 - Introduction To AccountingDylan Rabin PereiraNo ratings yet

- Kotak Mahindra Life Insurance ReportDocument72 pagesKotak Mahindra Life Insurance ReportGanesh D Panda100% (3)

- CORPORATE FINANCE - Financial Reconstruction & Business Reorganisation - Dayana MasturaDocument21 pagesCORPORATE FINANCE - Financial Reconstruction & Business Reorganisation - Dayana MasturaDayana MasturaNo ratings yet

- Philippine Financial Reporting Framework For CooperativesDocument36 pagesPhilippine Financial Reporting Framework For CooperativesMarianne SironNo ratings yet

- Chapter 8: The Mathematics of Finance: Learner'S Module: Mathematics in The Modern WorldDocument6 pagesChapter 8: The Mathematics of Finance: Learner'S Module: Mathematics in The Modern Worldchibbs1324100% (2)

- RECALLED QUESTIONS (2016-18) : (Ibps Different Banks Promotion Test)Document11 pagesRECALLED QUESTIONS (2016-18) : (Ibps Different Banks Promotion Test)Arun PrakashNo ratings yet

- Impairment of Assets (IAS 36)Document16 pagesImpairment of Assets (IAS 36)cynthiama7777No ratings yet

- Impairment of Assets - Individual Assets - 0Document31 pagesImpairment of Assets - Individual Assets - 0pam pamNo ratings yet

- Session 8 (22nd Oct)Document122 pagesSession 8 (22nd Oct)zf8dkk8fnzNo ratings yet

- ch12 PDFDocument9 pagesch12 PDFEmma Mariz GarciaNo ratings yet

- Summary - IAS 36 by hkDocument3 pagesSummary - IAS 36 by hkaimanraees10No ratings yet

- Impairment of Long-Lived Assets: Balance SheetDocument2 pagesImpairment of Long-Lived Assets: Balance SheetJuan MatiasNo ratings yet

- INTERMEDIATE ACCOUNTING - IMPAIRMENT OF ASSETS (PAS 36)Document4 pagesINTERMEDIATE ACCOUNTING - IMPAIRMENT OF ASSETS (PAS 36)22100629No ratings yet

- Impairment of Assets NotesDocument23 pagesImpairment of Assets NotesRonnie MontanerNo ratings yet

- CAF 1 SupplementsDocument36 pagesCAF 1 SupplementsAb WasayNo ratings yet

- Week 9 Impairment of Non-Current Assets (MFRS 136) For StudentsDocument32 pagesWeek 9 Impairment of Non-Current Assets (MFRS 136) For StudentsAnselmNo ratings yet

- Chapter 17 IAS 36 Impairment of AssetsDocument13 pagesChapter 17 IAS 36 Impairment of AssetsKelvin Chu JYNo ratings yet

- Oacc - Pp&e P 1 - P3Document23 pagesOacc - Pp&e P 1 - P3Trixie Divine SantosNo ratings yet

- 5th Lecture-Ch. 5Document57 pages5th Lecture-Ch. 5otaku25488No ratings yet

- Ch9 Impairment of AssetsDocument20 pagesCh9 Impairment of AssetsiKarloNo ratings yet

- Pas34 1Document7 pagesPas34 1Elisha Mae ManzonNo ratings yet

- AAFR by Sir Nasir Abbas - RemovedDocument559 pagesAAFR by Sir Nasir Abbas - RemovedAbdul BalochNo ratings yet

- E-Portfolio: PAS 36 - Impairment of AssetsDocument3 pagesE-Portfolio: PAS 36 - Impairment of AssetsKaye NaranjoNo ratings yet

- Grey Minimalist Business Project PresentationDocument10 pagesGrey Minimalist Business Project PresentationTrixie Divine SantosNo ratings yet

- Ias 36 ImpairementDocument24 pagesIas 36 Impairementesulawyer2001No ratings yet

- Tudy Buddy: Ias 36 - Impairment of AssetsDocument2 pagesTudy Buddy: Ias 36 - Impairment of AssetsAbdullah Al Amin MubinNo ratings yet

- Impairment of AssetsDocument4 pagesImpairment of AssetsNath BongalonNo ratings yet

- Survey of Accounting 6th Edition Warren Solutions ManualDocument25 pagesSurvey of Accounting 6th Edition Warren Solutions Manualbrianhue3zqkp100% (26)

- Survey of Accounting 6Th Edition Warren Solutions Manual Full Chapter PDFDocument46 pagesSurvey of Accounting 6Th Edition Warren Solutions Manual Full Chapter PDFzanewilliamhzkbr100% (7)

- Impairment of Non Current Assets - Ias 36: - Impairment Is A Reduction To The Recoverable Amount of An Asset or ADocument89 pagesImpairment of Non Current Assets - Ias 36: - Impairment Is A Reduction To The Recoverable Amount of An Asset or ATram NguyenNo ratings yet

- Summary of Ias 36Document4 pagesSummary of Ias 36Dewa WindhuNo ratings yet

- Impairment of AssetDocument27 pagesImpairment of AssetSrabon BaruaNo ratings yet

- HSBC0469, D, Priyansh - Group D11Document14 pagesHSBC0469, D, Priyansh - Group D11Priyansh KhatriNo ratings yet

- Corporate Reporting - MFRS116 - Property, Plant and Equipment - PPE - Dayana MasturaDocument19 pagesCorporate Reporting - MFRS116 - Property, Plant and Equipment - PPE - Dayana MasturaDayana MasturaNo ratings yet

- Cash Flow StatementDocument12 pagesCash Flow StatementRIONAN CUADRASALNo ratings yet

- Impairment of Assets: Students Name Ameera Al - Shdeifat Mahmood Al - Saad Ahmad RadaydehDocument28 pagesImpairment of Assets: Students Name Ameera Al - Shdeifat Mahmood Al - Saad Ahmad Radaydehahmad RadaidehNo ratings yet

- Depreciation Accounting PDFDocument42 pagesDepreciation Accounting PDFASIFNo ratings yet

- Chapter 5 Depreciation Accounting PDFDocument42 pagesChapter 5 Depreciation Accounting PDFravibhartia197888% (8)

- Impairments Setup and ProcessDocument35 pagesImpairments Setup and ProcessRam PillaiNo ratings yet

- PAS 7 Cash Flows ExplainedDocument6 pagesPAS 7 Cash Flows ExplainedLEIGHANNE ZYRIL SANTOSNo ratings yet

- Acc470 Ias 36Document33 pagesAcc470 Ias 36Naji EssaNo ratings yet

- Group Five DisposalDocument10 pagesGroup Five Disposalelvis page kamunanwireNo ratings yet

- Pas 36Document38 pagesPas 36iyahvrezNo ratings yet

- Kelompok 5 Chapter 9 EditedDocument38 pagesKelompok 5 Chapter 9 EditedFathiyah AdilahNo ratings yet

- Accounting Standard 28 Impairment 2Document15 pagesAccounting Standard 28 Impairment 2sosteniblebusinessNo ratings yet

- ACC2001 Lecture 11 Asset ImpairmentDocument42 pagesACC2001 Lecture 11 Asset Impairmentmichael krueseiNo ratings yet

- IMPAIRMENTS WHITE PAPER v2 PDFDocument33 pagesIMPAIRMENTS WHITE PAPER v2 PDFSrinibasNo ratings yet

- FAM Presentation MODULE-3Document72 pagesFAM Presentation MODULE-3upperdig5No ratings yet

- Fixed Assets - NotesDocument8 pagesFixed Assets - NotesMuhammad Imran LatifNo ratings yet

- FINC6021 - Financial StatementsDocument126 pagesFINC6021 - Financial Statements尹米勒No ratings yet

- Unit Ii Learning Activities Accounting StandardsDocument8 pagesUnit Ii Learning Activities Accounting StandardsChin FiguraNo ratings yet

- SS - 5-6 - Mindmaps - Financial ReportingDocument48 pagesSS - 5-6 - Mindmaps - Financial Reportinghaoyuting426No ratings yet

- CA Notes Concept and Accounting of Depreciation PDFDocument36 pagesCA Notes Concept and Accounting of Depreciation PDFBijay Aryan Dhakal100% (2)

- Week 5 - Chapter 4Document45 pagesWeek 5 - Chapter 4AJNo ratings yet

- Is Described As An Event Which IsDocument2 pagesIs Described As An Event Which IsstoneNo ratings yet

- Is Described As An Event Which IsDocument2 pagesIs Described As An Event Which IsstoneNo ratings yet

- Intangible AssetsDocument3 pagesIntangible Assetsgreat angelNo ratings yet

- Coop 8Document2 pagesCoop 8hoxhiiNo ratings yet

- Fixed AssetDocument20 pagesFixed AssetMohamed Ahmed RammadanNo ratings yet

- 05 Ias 36Document4 pages05 Ias 36Irtiza AbbasNo ratings yet

- Workbook 4 (July 2022)Document41 pagesWorkbook 4 (July 2022)Sansaar KandhroNo ratings yet

- Corporate Sustainability - Social Accounting - Dayana MasturaDocument20 pagesCorporate Sustainability - Social Accounting - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Finance - Mergers and Acquisitions - Financing Issues - Dayana MasturaDocument11 pagesCorporate Finance - Mergers and Acquisitions - Financing Issues - Dayana MasturaDayana MasturaNo ratings yet

- Sustainability - Dayana MasturaDocument42 pagesSustainability - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Reporting - MFRS138 - Intangible Assets - Dayana MasturaDocument17 pagesCorporate Reporting - MFRS138 - Intangible Assets - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Reporting - MFRS140 - Investment Properties - Dayana MasturaDocument12 pagesCorporate Reporting - MFRS140 - Investment Properties - Dayana MasturaDayana MasturaNo ratings yet

- CORPORATE REPORTING - MFRS137 - Provisions, Contingent Liabilities and Contingent Assets - Dayana MasturaDocument12 pagesCORPORATE REPORTING - MFRS137 - Provisions, Contingent Liabilities and Contingent Assets - Dayana MasturaDayana MasturaNo ratings yet

- CORPORATE REPORTING - Limited Companies - Bonus and Rights Issues - Dayana MasturaDocument16 pagesCORPORATE REPORTING - Limited Companies - Bonus and Rights Issues - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Reporting - MFRS120 - Government Grants - Dayana MasturaDocument14 pagesCorporate Reporting - MFRS120 - Government Grants - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Reporting - MFRS102 - Inventory - Dayana MasturaDocument24 pagesCorporate Reporting - MFRS102 - Inventory - Dayana MasturaDayana MasturaNo ratings yet

- Global Sustainability Practices - Board Gender Diversity - Dayana MasturaDocument11 pagesGlobal Sustainability Practices - Board Gender Diversity - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Reporting - MFRS116 - Property, Plant and Equipment - PPE - Dayana MasturaDocument19 pagesCorporate Reporting - MFRS116 - Property, Plant and Equipment - PPE - Dayana MasturaDayana MasturaNo ratings yet

- CORPORATE REPORTING - Limited Companies - Redemption of Shares by A Company - Dayana MasturaDocument7 pagesCORPORATE REPORTING - Limited Companies - Redemption of Shares by A Company - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Reporting - Limited Companies - The Statement of Financial Position (SOFP) - Dayana MasturaDocument19 pagesCorporate Reporting - Limited Companies - The Statement of Financial Position (SOFP) - Dayana MasturaDayana MasturaNo ratings yet

- CORPORATE REPORTING - An Introduction To The Accounts of Limited Companies - PLC - LTD - Dayana MasturaDocument10 pagesCORPORATE REPORTING - An Introduction To The Accounts of Limited Companies - PLC - LTD - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Sustainability - Theoretical Framework - Dayana MasturaDocument17 pagesCorporate Sustainability - Theoretical Framework - Dayana MasturaDayana MasturaNo ratings yet

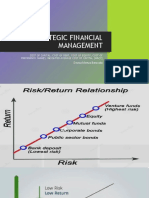

- Strategic Financial ManagementDocument33 pagesStrategic Financial ManagementDayana MasturaNo ratings yet

- Corporate Sustainability - Accounting and Profit - Dayana MasturaDocument26 pagesCorporate Sustainability - Accounting and Profit - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Reporting - Limited Companies - The Statement of Comprehensive Income (SOCI) - Dayana MasturaDocument12 pagesCorporate Reporting - Limited Companies - The Statement of Comprehensive Income (SOCI) - Dayana MasturaDayana MasturaNo ratings yet

- Strategic Financial Management - Working Capital Investment - Dayana MasturaDocument31 pagesStrategic Financial Management - Working Capital Investment - Dayana MasturaDayana MasturaNo ratings yet

- Strategic Financial ManagementDocument28 pagesStrategic Financial ManagementDayana MasturaNo ratings yet

- Strategic Financial ManagementDocument21 pagesStrategic Financial ManagementDayana MasturaNo ratings yet

- Unit-1 Potential RevenueDocument5 pagesUnit-1 Potential RevenueYash RajNo ratings yet

- Lecture 4. StockDocument26 pagesLecture 4. StockazizbektokhirbekovNo ratings yet

- Al-Ghazi Tractors Ltd (AGTL) Balance Sheet and Financial Ratios AnalysisDocument13 pagesAl-Ghazi Tractors Ltd (AGTL) Balance Sheet and Financial Ratios AnalysisM.ShahnamNo ratings yet

- Study of Risk Management in Digital Transaction in Banking SectorDocument10 pagesStudy of Risk Management in Digital Transaction in Banking SectorSRUTISMITA PATTANAIKNo ratings yet

- 6898 - Equity InvestmentsDocument2 pages6898 - Equity InvestmentsAljur SalamedaNo ratings yet

- IAS 2 Inventories QuizDocument14 pagesIAS 2 Inventories QuizRocel Vasaya PacresNo ratings yet

- Benefit Illustration For HDFC Life Sanchay Par AdvantageDocument3 pagesBenefit Illustration For HDFC Life Sanchay Par Advantagekesk32No ratings yet

- F6mys Jun 2011 QuDocument10 pagesF6mys Jun 2011 Qutoushiga100% (1)

- Week 4 - Topic OverviewDocument16 pagesWeek 4 - Topic Overviewsibzz08No ratings yet

- Ideal candidate to utilize unique skills and experienceDocument1 pageIdeal candidate to utilize unique skills and experienceAli AyubNo ratings yet

- Axis Card 1Document4 pagesAxis Card 1Om PrakashNo ratings yet

- 2014 Complete Annual Report PDFDocument264 pages2014 Complete Annual Report PDFChaityAzmeeNo ratings yet

- Ebullient Services invoice for 400kg gold shipment to ItalyDocument1 pageEbullient Services invoice for 400kg gold shipment to ItalyYimbi King Dénis-PârisNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Sanchita KunwerNo ratings yet

- Annual Report 2012 Al Arafa BankDocument150 pagesAnnual Report 2012 Al Arafa BankWasik Abdullah MomitNo ratings yet

- Cash Flow and Financial Planning Chapter SolutionsDocument3 pagesCash Flow and Financial Planning Chapter SolutionsSaifur R. SabbirNo ratings yet

- Customizing For Hedge Management: Hedging ClassificationDocument13 pagesCustomizing For Hedge Management: Hedging ClassificationDillip Kumar mallickNo ratings yet

- Georgia Economic Outlook 2022Document43 pagesGeorgia Economic Outlook 2022Jessie GarciaNo ratings yet

- Bank Reconciliation Statements: MBA ExecutiveDocument37 pagesBank Reconciliation Statements: MBA ExecutiveAreeb IqbalNo ratings yet

- Chapter 9 Accounting Cycle of A Service BusinessDocument59 pagesChapter 9 Accounting Cycle of A Service BusinessArlyn Ragudos BSA1No ratings yet