You might also like

- FMO ESG MANAGEMENT TOOLKIT MANUALDocument32 pagesFMO ESG MANAGEMENT TOOLKIT MANUALLouis SamakéNo ratings yet

- Sustainability ReportDocument21 pagesSustainability ReportRevathi Revathi100% (2)

- A Starters Guide To Sustainability ReportingDocument76 pagesA Starters Guide To Sustainability ReportingEnrique Navarrete Morales100% (1)

- REACH 2012 SUSTAINABILITY PLANDocument13 pagesREACH 2012 SUSTAINABILITY PLANMian Santos100% (1)

- Corporate Sustainability - Social Accounting - Dayana MasturaDocument20 pagesCorporate Sustainability - Social Accounting - Dayana MasturaDayana MasturaNo ratings yet

- ESG Steering Committee Charter SummaryDocument2 pagesESG Steering Committee Charter Summarykeyice100% (2)

- Apple Environmental Progress Report 2021Document105 pagesApple Environmental Progress Report 2021Vatsal PancholiNo ratings yet

- Ceres Roadmap For SustainabilityDocument88 pagesCeres Roadmap For Sustainabilitymonkey_business100% (1)

- IFC Sustainability +frameworkDocument84 pagesIFC Sustainability +frameworkALBERTO GUAJARDO MENESESNo ratings yet

- Environmental & Social Screening Report West Lunga Hydropower 2020Document133 pagesEnvironmental & Social Screening Report West Lunga Hydropower 2020Peter Mautelo100% (1)

- Corporate Sustainability: Jane Okun Bomba Chief Sustainability, IR and Comms Officer IHS Inc. February 2014Document24 pagesCorporate Sustainability: Jane Okun Bomba Chief Sustainability, IR and Comms Officer IHS Inc. February 2014ReveJoyNo ratings yet

- Sustainability Report GRI StandardDocument34 pagesSustainability Report GRI StandardRaditya ShintaNo ratings yet

- ESG-Ebook-What ESG Means For Your Business PDFDocument14 pagesESG-Ebook-What ESG Means For Your Business PDFamoghkanade100% (1)

- Lack of Private Sector Support: ESG Is Actually Contributing To Financial PerformanceDocument2 pagesLack of Private Sector Support: ESG Is Actually Contributing To Financial PerformanceBảoNgọcNo ratings yet

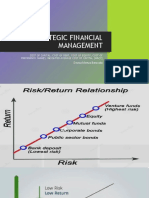

- Raising a new Generation of Leaders through Strategic Financial ManagementDocument23 pagesRaising a new Generation of Leaders through Strategic Financial ManagementgeorgeNo ratings yet

- Corporate SustainabilityDocument20 pagesCorporate SustainabilityNashwa SaadNo ratings yet

- ESG Test Format - New HireDocument5 pagesESG Test Format - New HireGoutham NethaNo ratings yet

- Environmental Impact AssessmentDocument7 pagesEnvironmental Impact AssessmentMahmoudRaafatNo ratings yet

- CDC Annual ESG Report TemplateDocument6 pagesCDC Annual ESG Report TemplateJean OlemouNo ratings yet

- 2015 Annual Report Highlights Odebrecht's Sustainability Results in AngolaDocument55 pages2015 Annual Report Highlights Odebrecht's Sustainability Results in AngolaDebbie CollettNo ratings yet

- Sustainability Plan PDFDocument51 pagesSustainability Plan PDFCarl WilliamsNo ratings yet

- Capacity Building On Health, Safety and EnvironmentalDocument131 pagesCapacity Building On Health, Safety and EnvironmentalSyaifullah Mustari100% (1)

- lTIIA ESG HandbookDocument94 pageslTIIA ESG HandbookEmdad Yusuf100% (1)

- Sustainalytics - Portfolio Research - Combining ESG Risk and Economic Moat - Dec 2020 PDFDocument24 pagesSustainalytics - Portfolio Research - Combining ESG Risk and Economic Moat - Dec 2020 PDFs harsha vardhanNo ratings yet

- In The Spotlight How Software Accelerates Sustainability Reporting and Performance Management FINAL CompressedDocument18 pagesIn The Spotlight How Software Accelerates Sustainability Reporting and Performance Management FINAL CompressedDDNo ratings yet

- Business Continuity Management FrameworkDocument17 pagesBusiness Continuity Management Frameworktahira100% (1)

- SE Environmental Policy SampleDocument2 pagesSE Environmental Policy SampleJEXNo ratings yet

- ESG ChecklistDocument9 pagesESG ChecklistSafe HavenNo ratings yet

- Sustainability Indicators and Sustainability Performance MGTDocument129 pagesSustainability Indicators and Sustainability Performance MGTFang Salinee100% (1)

- Sustainability PresentationDocument59 pagesSustainability PresentationanirbanmbeNo ratings yet

- IFC Sustainability FrameworkDocument84 pagesIFC Sustainability FrameworkInternational Finance Corporation (IFC)No ratings yet

- Risk and Opportunity ManagementDocument6 pagesRisk and Opportunity Managementjalefaye abapoNo ratings yet

- Final Risk Management Manual Edition 1Document46 pagesFinal Risk Management Manual Edition 1Rahul Kumar100% (1)

- Environmental & Social Impact AssessmentDocument57 pagesEnvironmental & Social Impact AssessmentMOHAMEDNo ratings yet

- Environment, Health and Safety Report: A Shared Interest Between Xilinx and Our CustomersDocument18 pagesEnvironment, Health and Safety Report: A Shared Interest Between Xilinx and Our CustomersFarrukh Pervaiz100% (1)

- Danone Exhaustive Extra-Financial 2018 DataDocument23 pagesDanone Exhaustive Extra-Financial 2018 DatashamimshawonNo ratings yet

- Tip Safety PlanDocument28 pagesTip Safety PlanTC Nihal AlcansoyNo ratings yet

- Welcome To Sheq FoundationDocument8 pagesWelcome To Sheq FoundationElla AgbettorNo ratings yet

- REACH 2012 SUSTAINABILITY PLAN TEMPLATEDocument15 pagesREACH 2012 SUSTAINABILITY PLAN TEMPLATEArvin F. Villodres100% (1)

- ISO 26000 Basic Training Material Annexslides 2017Document59 pagesISO 26000 Basic Training Material Annexslides 2017Averyl Lei Sta.Ana100% (2)

- CSR & HSBC's Economic, Discretionary, Legal & Ethical ResponsibilitiesDocument36 pagesCSR & HSBC's Economic, Discretionary, Legal & Ethical ResponsibilitiesNajjar7No ratings yet

- Investors and The Blue EconomyDocument44 pagesInvestors and The Blue Economyutkarsh deepakNo ratings yet

- EY Sustainability Reporting The Time Is NowDocument24 pagesEY Sustainability Reporting The Time Is NowStevan PknNo ratings yet

- Shaping Safety CultureDocument54 pagesShaping Safety CultureNasrulNo ratings yet

- Detailed Environmental and Social Impact Assessment (ESIA) Study - Final ReportDocument183 pagesDetailed Environmental and Social Impact Assessment (ESIA) Study - Final ReportDaniel Chebii KipsangNo ratings yet

- HWMDocument41 pagesHWMJessica Laine TumbagaNo ratings yet

- Project Description (Elecpro)Document21 pagesProject Description (Elecpro)S Tunkla EcharojNo ratings yet

- ESG Practice in MalaysiaDocument29 pagesESG Practice in MalaysiaRazin NaimNo ratings yet

- Business Risk and Risk ManagementDocument5 pagesBusiness Risk and Risk ManagementDickens LubangaNo ratings yet

- Recent Trends in Industrial Waste Management PDFDocument22 pagesRecent Trends in Industrial Waste Management PDFVivek YadavNo ratings yet

- Equator PrinciplesDocument10 pagesEquator Principlesemma monica100% (2)

- Playbook For: Climate FinanceDocument20 pagesPlaybook For: Climate FinanceMARIO LOPEZNo ratings yet

- Sustainability Plan for Statewide Afterschool NetworkDocument4 pagesSustainability Plan for Statewide Afterschool NetworkLawrence Patrick Ladia Limen100% (1)

- Carbon Accounting: Challenges and Public InvolvementDocument4 pagesCarbon Accounting: Challenges and Public InvolvementVaibhav SharmaNo ratings yet

- Integrated Management SystemsDocument21 pagesIntegrated Management SystemsisaacbombayNo ratings yet

- ESG Indicator Metrics Used by Organisations To Assess The Degree of Sustainability in CompaniesDocument12 pagesESG Indicator Metrics Used by Organisations To Assess The Degree of Sustainability in CompaniesIJAERS JOURNALNo ratings yet

- Partially EditedDocument28 pagesPartially EditedJanine ManzanoNo ratings yet

- Sustainability Reporting Practices and Company Characteristics: Empirical Research On Listed Companies of BangladeshDocument19 pagesSustainability Reporting Practices and Company Characteristics: Empirical Research On Listed Companies of BangladeshFabihaNo ratings yet

- Mgnt2sm AssignmentDocument12 pagesMgnt2sm AssignmentAkhona NkumaneNo ratings yet

- Corporate Sustainability - Environmental Accounting - Dayana MasturaDocument24 pagesCorporate Sustainability - Environmental Accounting - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Finance - Mergers and Acquisitions - Financing Issues - Dayana MasturaDocument11 pagesCorporate Finance - Mergers and Acquisitions - Financing Issues - Dayana MasturaDayana MasturaNo ratings yet

- Sustainability - Dayana MasturaDocument42 pagesSustainability - Dayana MasturaDayana MasturaNo ratings yet

- CORPORATE FINANCE - Financial Reconstruction & Business Reorganisation - Dayana MasturaDocument21 pagesCORPORATE FINANCE - Financial Reconstruction & Business Reorganisation - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Finance - Business Valuations - Dayana MasturaDocument14 pagesCorporate Finance - Business Valuations - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Reporting - MFRS138 - Intangible Assets - Dayana MasturaDocument17 pagesCorporate Reporting - MFRS138 - Intangible Assets - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Reporting - MFRS140 - Investment Properties - Dayana MasturaDocument12 pagesCorporate Reporting - MFRS140 - Investment Properties - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Finance - Mergers and Acquisitions - Strategic Issues - Dayana MasturaDocument19 pagesCorporate Finance - Mergers and Acquisitions - Strategic Issues - Dayana MasturaDayana MasturaNo ratings yet

- Global Sustainability Practices - Board Gender Diversity - Dayana MasturaDocument11 pagesGlobal Sustainability Practices - Board Gender Diversity - Dayana MasturaDayana MasturaNo ratings yet

- CORPORATE REPORTING - MFRS137 - Provisions, Contingent Liabilities and Contingent Assets - Dayana MasturaDocument12 pagesCORPORATE REPORTING - MFRS137 - Provisions, Contingent Liabilities and Contingent Assets - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Finance - Capital Structure - Dayana MasturaDocument12 pagesCorporate Finance - Capital Structure - Dayana MasturaDayana MasturaNo ratings yet

- CORPORATE REPORTING - Limited Companies - Bonus and Rights Issues - Dayana MasturaDocument16 pagesCORPORATE REPORTING - Limited Companies - Bonus and Rights Issues - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Reporting - MFRS120 - Government Grants - Dayana MasturaDocument14 pagesCorporate Reporting - MFRS120 - Government Grants - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Reporting - MFRS116 - Property, Plant and Equipment - PPE - Dayana MasturaDocument19 pagesCorporate Reporting - MFRS116 - Property, Plant and Equipment - PPE - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Reporting - MFRS102 - Inventory - Dayana MasturaDocument24 pagesCorporate Reporting - MFRS102 - Inventory - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Reporting - MFRS136 - Impairment of Assets - Dayana MasturaDocument26 pagesCorporate Reporting - MFRS136 - Impairment of Assets - Dayana MasturaDayana MasturaNo ratings yet

- CORPORATE SUSTAINABILITY - Evolution of Corporate Reporting - Dayana MasturaDocument29 pagesCORPORATE SUSTAINABILITY - Evolution of Corporate Reporting - Dayana MasturaDayana MasturaNo ratings yet

- CORPORATE REPORTING - Limited Companies - Redemption of Shares by A Company - Dayana MasturaDocument7 pagesCORPORATE REPORTING - Limited Companies - Redemption of Shares by A Company - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Reporting - Limited Companies - The Statement of Financial Position (SOFP) - Dayana MasturaDocument19 pagesCorporate Reporting - Limited Companies - The Statement of Financial Position (SOFP) - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Sustainability - Stakeholder and Stewardship Theory - Dayana MasturaDocument18 pagesCorporate Sustainability - Stakeholder and Stewardship Theory - Dayana MasturaDayana Mastura100% (1)

- CORPORATE REPORTING - An Introduction To The Accounts of Limited Companies - PLC - LTD - Dayana MasturaDocument10 pagesCORPORATE REPORTING - An Introduction To The Accounts of Limited Companies - PLC - LTD - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Sustainability - Theoretical Framework - Dayana MasturaDocument17 pagesCorporate Sustainability - Theoretical Framework - Dayana MasturaDayana MasturaNo ratings yet

- Strategic Financial ManagementDocument33 pagesStrategic Financial ManagementDayana MasturaNo ratings yet

- Corporate Sustainability - Accounting and Profit - Dayana MasturaDocument26 pagesCorporate Sustainability - Accounting and Profit - Dayana MasturaDayana MasturaNo ratings yet

- Corporate Reporting - Limited Companies - The Statement of Comprehensive Income (SOCI) - Dayana MasturaDocument12 pagesCorporate Reporting - Limited Companies - The Statement of Comprehensive Income (SOCI) - Dayana MasturaDayana MasturaNo ratings yet

- Strategic Financial Management - Working Capital Investment - Dayana MasturaDocument31 pagesStrategic Financial Management - Working Capital Investment - Dayana MasturaDayana MasturaNo ratings yet

- Strategic Financial ManagementDocument28 pagesStrategic Financial ManagementDayana MasturaNo ratings yet

- Strategic Financial ManagementDocument21 pagesStrategic Financial ManagementDayana MasturaNo ratings yet

- MY DIGESTS - Public OfficersDocument12 pagesMY DIGESTS - Public OfficersMegan PacientoNo ratings yet

- Development Plan for Naxal-Affected Saranda RegionDocument22 pagesDevelopment Plan for Naxal-Affected Saranda RegionsachinNo ratings yet

- Course Material: National Board For Techniceal Education (Nbte)Document8 pagesCourse Material: National Board For Techniceal Education (Nbte)Mohammed HayatuNo ratings yet

- 4 2020 UP BOC Taxation Law ReviewerDocument263 pages4 2020 UP BOC Taxation Law ReviewerNathalie Bermudez50% (2)

- Evolution OF Public AdministrationDocument19 pagesEvolution OF Public AdministrationSruti UNo ratings yet

- Anatomy of Disaster Relief: The International Network in ActionDocument2 pagesAnatomy of Disaster Relief: The International Network in ActionAland MediaNo ratings yet

- Republic v. Gonzales, 13 SCRA 633 (1965)Document10 pagesRepublic v. Gonzales, 13 SCRA 633 (1965)citizenNo ratings yet

- Political Parties Programme Handbook No 18 EISADocument119 pagesPolitical Parties Programme Handbook No 18 EISALehlohonoloNo ratings yet

- Scope: I. Child Labour: Ii. Modern Slavery: Iii. Health, Safety and Hygiene: Iv. DisciplineDocument1 pageScope: I. Child Labour: Ii. Modern Slavery: Iii. Health, Safety and Hygiene: Iv. DisciplinepeaceckNo ratings yet

- Andhra Pradesh DWCRA Program ReviewDocument19 pagesAndhra Pradesh DWCRA Program Reviewsai kiran gudisevaNo ratings yet

- Cases For PrelimDocument49 pagesCases For PrelimDILG XIII- Atty. Robelen CallantaNo ratings yet

- Test Bank For Essential Statistics For Public Managers and Policy Analysts 4th Edition Evan Berman Xiaohu WangDocument34 pagesTest Bank For Essential Statistics For Public Managers and Policy Analysts 4th Edition Evan Berman Xiaohu Wanghilumwheretof5uk3h100% (44)

- Carter, William Public Fact Sheet 6-1-21Document1 pageCarter, William Public Fact Sheet 6-1-21inforumdocsNo ratings yet

- Promoting and Enforcing Human Rights in The International CommunityDocument3 pagesPromoting and Enforcing Human Rights in The International CommunityScarlettzartNo ratings yet

- Project Ipc AbhishekDocument17 pagesProject Ipc AbhishekAbhishekNo ratings yet

- TOR - Project Manager - GambiaDocument7 pagesTOR - Project Manager - Gambianana enguahNo ratings yet

- Barangay Development Council ConstitutionDocument4 pagesBarangay Development Council ConstitutionJessica Cindy100% (1)

- ZTBL Internship Report PDFDocument71 pagesZTBL Internship Report PDFmuhammad waseem100% (8)

- The Fleming Foundation Is A Charitable Organization Founded by GDocument1 pageThe Fleming Foundation Is A Charitable Organization Founded by GAmit PandeyNo ratings yet

- Civil Procedure Notes Compiled University of San Carlos College of Law 25Document3 pagesCivil Procedure Notes Compiled University of San Carlos College of Law 25Jan NiñoNo ratings yet

- Buckle Marsh Smale Assessing Resilience Vulnerability Principles Strategies ActionsDocument61 pagesBuckle Marsh Smale Assessing Resilience Vulnerability Principles Strategies ActionsRamanditya WimbardanaNo ratings yet

- Contentious Politics in TheoryDocument26 pagesContentious Politics in TheoryPANGKY_FNo ratings yet

- The Contemporary World M6T1Document12 pagesThe Contemporary World M6T1joint accountNo ratings yet

- ICL ProjectDocument8 pagesICL ProjectArjun SarkarNo ratings yet

- ISO 45000 Audit Questionnaire SAMPLEDocument2 pagesISO 45000 Audit Questionnaire SAMPLEMarco TsstNo ratings yet

- DM - Question Bank Module 6Document4 pagesDM - Question Bank Module 6Megha ThomasNo ratings yet

- Philippine Law School: F E B R U A R Y 2 4, 2 5, 2 6 & 2 7, 2 0 2 1Document1 pagePhilippine Law School: F E B R U A R Y 2 4, 2 5, 2 6 & 2 7, 2 0 2 1nbragasNo ratings yet

- Local Budget Memorandum No 82Document59 pagesLocal Budget Memorandum No 82Fernand Q BuensalidaNo ratings yet

- E004454 FullDocument12 pagesE004454 FullDarioNo ratings yet

- ITMProposers Day2022020v6Document32 pagesITMProposers Day2022020v6熊俊捷No ratings yet