You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Macroeconomics 12th Edition Gordon Solutions ManualDocument15 pagesMacroeconomics 12th Edition Gordon Solutions Manuallouisbeatrixzk9u100% (30)

- ATM Claim FormDocument1 pageATM Claim FormJm VenkiNo ratings yet

- Business Plan of Besties Online ServicesDocument6 pagesBusiness Plan of Besties Online Servicescompliance neilanztruckingNo ratings yet

- Chapter 14 Mas Agamata Answer KeyDocument21 pagesChapter 14 Mas Agamata Answer Keytae ah kimNo ratings yet

- L.E.K. Valuation Toolkit GuideTITLEL.E.K. Business Valuation Model InstructionsTITLEL.E.K. Toolkit for Valuing CompaniesDocument10 pagesL.E.K. Valuation Toolkit GuideTITLEL.E.K. Business Valuation Model InstructionsTITLEL.E.K. Toolkit for Valuing Companiesmmitre2100% (1)

- Maf 603 Suggested Solutions Solution 1Document5 pagesMaf 603 Suggested Solutions Solution 1anis izzatiNo ratings yet

- Holding Company Accounts - TheoryDocument4 pagesHolding Company Accounts - TheoryhanumanthaiahgowdaNo ratings yet

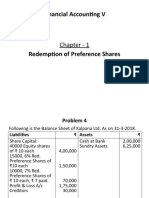

- Chapter 1 - Red. of Pref - Shares 2Document4 pagesChapter 1 - Red. of Pref - Shares 2hanumanthaiahgowdaNo ratings yet

- Compute the income from profession of Mr. Sanath Kumar for AY 2019-20Document3 pagesCompute the income from profession of Mr. Sanath Kumar for AY 2019-20hanumanthaiahgowdaNo ratings yet

- Liquidation of CompaniesDocument4 pagesLiquidation of CompanieshanumanthaiahgowdaNo ratings yet

- Chapter 4 - Valuation of SharesDocument11 pagesChapter 4 - Valuation of ShareshanumanthaiahgowdaNo ratings yet

- Types of AmalgamationDocument10 pagesTypes of AmalgamationhanumanthaiahgowdaNo ratings yet

- Income from Profession for DoctorDocument4 pagesIncome from Profession for Doctorhanumanthaiahgowda50% (2)

- HP - Interest CalculationDocument4 pagesHP - Interest CalculationhanumanthaiahgowdaNo ratings yet

- Income From House PropertyDocument36 pagesIncome From House PropertyhanumanthaiahgowdaNo ratings yet

- Financial Accounting V: Chapter - 1Document17 pagesFinancial Accounting V: Chapter - 1hanumanthaiahgowdaNo ratings yet

- Certificate Prog - PDF: 1.2 Academic FlexibilityDocument2 pagesCertificate Prog - PDF: 1.2 Academic FlexibilityhanumanthaiahgowdaNo ratings yet

- IT Problem 1 2Document1 pageIT Problem 1 2hanumanthaiahgowdaNo ratings yet

- Income Tax - SalaryDocument18 pagesIncome Tax - SalaryhanumanthaiahgowdaNo ratings yet

- Redemption of Preference Shares: Financial Accounting - VDocument8 pagesRedemption of Preference Shares: Financial Accounting - VhanumanthaiahgowdaNo ratings yet

- Single Entry ProblemsDocument2 pagesSingle Entry ProblemshanumanthaiahgowdaNo ratings yet

- Banking Practices 2Document11 pagesBanking Practices 2hanumanthaiahgowdaNo ratings yet

- Redemption of Preference Shares Format of Balance Sheet Particulars Note No. I Equity & Liabilities 1. Shareholders FundDocument2 pagesRedemption of Preference Shares Format of Balance Sheet Particulars Note No. I Equity & Liabilities 1. Shareholders FundhanumanthaiahgowdaNo ratings yet

- Answer Any Four Questions. (4X6 24) : Time: 3 Hours Max. Marks:120Document5 pagesAnswer Any Four Questions. (4X6 24) : Time: 3 Hours Max. Marks:120hanumanthaiahgowdaNo ratings yet

- Chapter - 1 GST - IntroductionDocument24 pagesChapter - 1 GST - IntroductionhanumanthaiahgowdaNo ratings yet

- Banking Practices 2Document11 pagesBanking Practices 2hanumanthaiahgowdaNo ratings yet

- LTC exemption and tax on retrenchment compensationDocument2 pagesLTC exemption and tax on retrenchment compensationhanumanthaiahgowdaNo ratings yet

- FA - Problem 1Document1 pageFA - Problem 1hanumanthaiahgowdaNo ratings yet

- HP - Interest CalculationDocument4 pagesHP - Interest CalculationhanumanthaiahgowdaNo ratings yet

- Income From House PropertyDocument32 pagesIncome From House PropertyhanumanthaiahgowdaNo ratings yet

- FA - Problem 8Document1 pageFA - Problem 8hanumanthaiahgowdaNo ratings yet

- IFHP - ProblemsDocument2 pagesIFHP - ProblemshanumanthaiahgowdaNo ratings yet

- E-Commerce HistoryDocument2 pagesE-Commerce HistoryhanumanthaiahgowdaNo ratings yet

- Session 5Document6 pagesSession 5hanumanthaiahgowdaNo ratings yet

- Why Is It Important?: Exchange and Progression of Goods - Marketing Is HighlyDocument11 pagesWhy Is It Important?: Exchange and Progression of Goods - Marketing Is HighlyhanumanthaiahgowdaNo ratings yet

- DocDocument6 pagesDoctai nguyenNo ratings yet

- DocxDocument7 pagesDocxSaoxalo ONo ratings yet

- Chapter 3 What Is MoneyDocument19 pagesChapter 3 What Is MoneySamanthaHandNo ratings yet

- SEC Form 10-Q FilingDocument39 pagesSEC Form 10-Q FilingalexandercuongNo ratings yet

- Upsc Classroom Online Courses 2023 Vajiram and RaviDocument2 pagesUpsc Classroom Online Courses 2023 Vajiram and RaviSHOUBHIK MUKHERJEENo ratings yet

- Accounting For Business CombinationsDocument13 pagesAccounting For Business CombinationsLu CasNo ratings yet

- Yosra Turki's Resume Highlighting Financial Analysis and Modeling ExperienceDocument2 pagesYosra Turki's Resume Highlighting Financial Analysis and Modeling ExperienceEmdadul Hoque TusherNo ratings yet

- Inflation Is The Decline of Purchasing Power of A Given Currency Over TimeDocument2 pagesInflation Is The Decline of Purchasing Power of A Given Currency Over TimeMidz SantayanaNo ratings yet

- IandF - CM1A - 202304 - Examiner ReportDocument15 pagesIandF - CM1A - 202304 - Examiner ReportFoo Zi YeeNo ratings yet

- NYIF Career Plan - FinalDocument186 pagesNYIF Career Plan - FinalChristian Ezequiel ArmenterosNo ratings yet

- Makalah Bahasa Inggris-1Document8 pagesMakalah Bahasa Inggris-1NajwaNo ratings yet

- HDFC Life BrochureDocument28 pagesHDFC Life BrochureVijay GopalNo ratings yet

- Tugas Novita Putri Tesalonika (A031191105)Document1 pageTugas Novita Putri Tesalonika (A031191105)Novita Putri TesalonikaNo ratings yet

- GCC July 2013Document68 pagesGCC July 2013Manas RawatNo ratings yet

- Equity Capital Common and Preffered StockDocument23 pagesEquity Capital Common and Preffered StockNicole LasiNo ratings yet

- Harbin Bank Co LTD (6138) 19 March 2014Document637 pagesHarbin Bank Co LTD (6138) 19 March 2014clam@whitecase.comNo ratings yet

- Acct Statement XX8558 19012023Document18 pagesAcct Statement XX8558 19012023Ankit GairolaNo ratings yet

- Corporate Valuation A Guide For Analysts Managers and Investors PDFDocument358 pagesCorporate Valuation A Guide For Analysts Managers and Investors PDFMalcomNo ratings yet

- SIMPLE & COMPOUND INTEREST CONCEPTS, FORMULAS & PROBLEMSDocument6 pagesSIMPLE & COMPOUND INTEREST CONCEPTS, FORMULAS & PROBLEMSDebasis BetalNo ratings yet

- What Is Dematerialisation?Document15 pagesWhat Is Dematerialisation?renuka03No ratings yet

- Common Derivative ProductsDocument71 pagesCommon Derivative Productsapi-19952066100% (2)

- Kebs 108Document26 pagesKebs 108Arjun kumar ShresthaNo ratings yet

- Annu Singh FinalDocument64 pagesAnnu Singh Finalsauravv7100% (1)

- ADD QuestionDocument8 pagesADD Questionomkolhe0007No ratings yet