You might also like

- Profits and Gains From Business and ProfessionDocument4 pagesProfits and Gains From Business and ProfessionAyaan AhmedNo ratings yet

- PGBP QuestionsDocument6 pagesPGBP QuestionsHdkakaksjsb100% (2)

- Characteristics of Business Economics1Document6 pagesCharacteristics of Business Economics1ihavenoidea33No ratings yet

- Taxable Income Calculation Mrs. NarayaniDocument5 pagesTaxable Income Calculation Mrs. NarayaniSumit PattanaikNo ratings yet

- Business & Profession Q - A 02.9.2020Document42 pagesBusiness & Profession Q - A 02.9.2020shyamiliNo ratings yet

- New Business Tax PlanningDocument47 pagesNew Business Tax PlanningashishNo ratings yet

- Costing AssignmentDocument15 pagesCosting AssignmentSumit SumanNo ratings yet

- Internship Final ReportDocument77 pagesInternship Final ReportSri Harsha100% (1)

- Problems On Taxable Salary Income Additional PDFDocument24 pagesProblems On Taxable Salary Income Additional PDFNALIN MEHTA 1713068No ratings yet

- A) Startup India QuestionnaireDocument1 pageA) Startup India Questionnairesubudhiprasanna50% (2)

- Direct Taxes Sem-Iii-20Document22 pagesDirect Taxes Sem-Iii-20Pranita MandlekarNo ratings yet

- Sidco Functions and SchemesDocument11 pagesSidco Functions and SchemesKarthikacauraNo ratings yet

- Group - I Paper - 1 Accounting V2 Chapter 13 PDFDocument13 pagesGroup - I Paper - 1 Accounting V2 Chapter 13 PDFjashveer rekhiNo ratings yet

- Royalty AccountsDocument5 pagesRoyalty AccountsRobert Henson100% (2)

- Tax Planning and Employee RemunerationDocument10 pagesTax Planning and Employee Remunerationabdulraqeeb alareqiNo ratings yet

- Assessment of CompaniesDocument5 pagesAssessment of Companiesmohanraokp22790% (1)

- Maratha Samaj Seva Mandal’s Farm Accounting ProblemsDocument7 pagesMaratha Samaj Seva Mandal’s Farm Accounting ProblemsAniket BhojaneNo ratings yet

- Whirlpool Financial AnalysisDocument5 pagesWhirlpool Financial AnalysisuddhavkulkarniNo ratings yet

- Worksheet For Issue of Share and DebentureDocument2 pagesWorksheet For Issue of Share and DebentureLaxmi Kant SahaniNo ratings yet

- Problems With Solution Capital GainsDocument12 pagesProblems With Solution Capital Gainsnaqi ali100% (1)

- Branch Account Problems & AnswerDocument11 pagesBranch Account Problems & Answeranand dpiNo ratings yet

- Residential StatusDocument15 pagesResidential StatusDeepak MinhasNo ratings yet

- What is TDS? Advance Tax and ProblemsDocument8 pagesWhat is TDS? Advance Tax and ProblemsNishantNo ratings yet

- Income from Salaries: Calculating Exempted Allowances, Taxable Gratuity & PensionDocument53 pagesIncome from Salaries: Calculating Exempted Allowances, Taxable Gratuity & PensionSiva SankariNo ratings yet

- Royalty AccountsDocument11 pagesRoyalty AccountsVipin Mandyam Kadubi0% (1)

- Request Letter - Shivakumar-FertilizerDocument5 pagesRequest Letter - Shivakumar-Fertilizernaveen KumarNo ratings yet

- Income Tax Salary NotesDocument48 pagesIncome Tax Salary NotesTanya AntilNo ratings yet

- 6 Sem Bcom - Management Accounting PDFDocument71 pages6 Sem Bcom - Management Accounting PDFaldhhdNo ratings yet

- Marginal Costing and Its Application - ProblemsDocument5 pagesMarginal Costing and Its Application - ProblemsAAKASH BAIDNo ratings yet

- Fin Account-Sole Trading AnswersDocument10 pagesFin Account-Sole Trading AnswersAR Ananth Rohith BhatNo ratings yet

- Fortune TellerDocument3 pagesFortune TellerbharatNo ratings yet

- Mrs. Batliboi's income from other sourcesDocument5 pagesMrs. Batliboi's income from other sourcesSarvar PathanNo ratings yet

- Taxable Salary Problem With Solution Part 1Document2 pagesTaxable Salary Problem With Solution Part 1NagadeepaNo ratings yet

- Income From House PropertyDocument26 pagesIncome From House PropertySuyash Patwa100% (1)

- House PropertyDocument18 pagesHouse PropertyNidhi LathNo ratings yet

- PCA & RD Bank PDFDocument86 pagesPCA & RD Bank PDFmohan ks100% (2)

- Working Capital Requirement QuestionsDocument2 pagesWorking Capital Requirement QuestionsVIRAL DOSHI100% (1)

- B.Com. Degree Exam Income Tax PaperDocument0 pagesB.Com. Degree Exam Income Tax PaperbkamithNo ratings yet

- Final Summer Training Report Mohit PalDocument110 pagesFinal Summer Training Report Mohit Palbharat sachdevaNo ratings yet

- Unit - V Budget and Budgetary Control ProblemsDocument2 pagesUnit - V Budget and Budgetary Control ProblemsalexanderNo ratings yet

- Deductions under Section 80C to 80U of the Income Tax ActDocument9 pagesDeductions under Section 80C to 80U of the Income Tax ActSarvar PathanNo ratings yet

- Tax PlanDocument2 pagesTax PlanMrigendra MishraNo ratings yet

- Employee Loan AgreementDocument3 pagesEmployee Loan Agreementshannbaby22No ratings yet

- Problems On Income From Salaries: Tax SupplementDocument20 pagesProblems On Income From Salaries: Tax SupplementJkNo ratings yet

- Course Name: 2T7 - Cost AccountingDocument56 pagesCourse Name: 2T7 - Cost Accountingjhggd100% (1)

- Describe The Scope of Payment of Gratuity Act 1972Document3 pagesDescribe The Scope of Payment of Gratuity Act 1972Jaspreet SinghNo ratings yet

- Functions of A SalesmanDocument2 pagesFunctions of A SalesmanpilotNo ratings yet

- Residential Status Problems 2021-2022-1Document5 pagesResidential Status Problems 2021-2022-120-UCO-517 AJAY KELVIN ANo ratings yet

- As-11 The Effects of Changes in Foreign Exchange RatesDocument21 pagesAs-11 The Effects of Changes in Foreign Exchange RatesDipen AdhikariNo ratings yet

- Tally Journal Entry QuestionsDocument3 pagesTally Journal Entry QuestionsVikas KumarNo ratings yet

- Problems On Joint VentureDocument8 pagesProblems On Joint VentureKrishna Prince M MNo ratings yet

- Consignment CorrectDocument51 pagesConsignment CorrectPraveetha Prakash75% (4)

- Double Tax Avoidance AgreementDocument13 pagesDouble Tax Avoidance AgreementRavi SinghNo ratings yet

- Industrial Securities MarketDocument16 pagesIndustrial Securities MarketNaga Mani Merugu100% (3)

- Objectives & Functions of IDBI BankDocument2 pagesObjectives & Functions of IDBI BankParveen SinghNo ratings yet

- Customs Duty: 1) Trisha Company Imported A Machine From Europe. From The FollowingDocument32 pagesCustoms Duty: 1) Trisha Company Imported A Machine From Europe. From The FollowingAneesh D'souzaNo ratings yet

- Chapter 1 MCQs On Income Tax Rates and Basic Concept of Income TaxDocument25 pagesChapter 1 MCQs On Income Tax Rates and Basic Concept of Income TaxSonu KumarNo ratings yet

- Trademark NOC FormatDocument1 pageTrademark NOC FormatVIBHOR100% (2)

- Project ReportDocument14 pagesProject Reportsee248985No ratings yet

- Illustrative Examples Accounting For Health Care Providers-HospitalsDocument2 pagesIllustrative Examples Accounting For Health Care Providers-HospitalsLa MarieNo ratings yet

- Holding Company Accounts - TheoryDocument4 pagesHolding Company Accounts - TheoryhanumanthaiahgowdaNo ratings yet

- Chapter 1 - Red. of Pref - Shares 2Document4 pagesChapter 1 - Red. of Pref - Shares 2hanumanthaiahgowdaNo ratings yet

- Income Tax - SalaryDocument18 pagesIncome Tax - SalaryhanumanthaiahgowdaNo ratings yet

- Liquidation of CompaniesDocument4 pagesLiquidation of CompanieshanumanthaiahgowdaNo ratings yet

- Chapter 4 - Valuation of SharesDocument11 pagesChapter 4 - Valuation of ShareshanumanthaiahgowdaNo ratings yet

- Types of AmalgamationDocument10 pagesTypes of AmalgamationhanumanthaiahgowdaNo ratings yet

- Compute the income from profession of Mr. Sanath Kumar for AY 2019-20Document3 pagesCompute the income from profession of Mr. Sanath Kumar for AY 2019-20hanumanthaiahgowdaNo ratings yet

- Banking Practices 2Document11 pagesBanking Practices 2hanumanthaiahgowdaNo ratings yet

- Income From House PropertyDocument36 pagesIncome From House PropertyhanumanthaiahgowdaNo ratings yet

- Financial Accounting V: Chapter - 1Document17 pagesFinancial Accounting V: Chapter - 1hanumanthaiahgowdaNo ratings yet

- Certificate Prog - PDF: 1.2 Academic FlexibilityDocument2 pagesCertificate Prog - PDF: 1.2 Academic FlexibilityhanumanthaiahgowdaNo ratings yet

- IT Problem 1 2Document1 pageIT Problem 1 2hanumanthaiahgowdaNo ratings yet

- Redemption of Preference Shares: Financial Accounting - VDocument8 pagesRedemption of Preference Shares: Financial Accounting - VhanumanthaiahgowdaNo ratings yet

- HP - Interest CalculationDocument4 pagesHP - Interest CalculationhanumanthaiahgowdaNo ratings yet

- Single Entry ProblemsDocument2 pagesSingle Entry ProblemshanumanthaiahgowdaNo ratings yet

- Banking PracticesDocument29 pagesBanking PracticeshanumanthaiahgowdaNo ratings yet

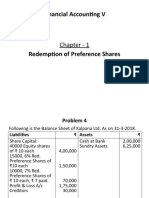

- Redemption of Preference Shares Format of Balance Sheet Particulars Note No. I Equity & Liabilities 1. Shareholders FundDocument2 pagesRedemption of Preference Shares Format of Balance Sheet Particulars Note No. I Equity & Liabilities 1. Shareholders FundhanumanthaiahgowdaNo ratings yet

- Answer Any Four Questions. (4X6 24) : Time: 3 Hours Max. Marks:120Document5 pagesAnswer Any Four Questions. (4X6 24) : Time: 3 Hours Max. Marks:120hanumanthaiahgowdaNo ratings yet

- Chapter - 1 GST - IntroductionDocument24 pagesChapter - 1 GST - IntroductionhanumanthaiahgowdaNo ratings yet

- Banking Practices 2Document11 pagesBanking Practices 2hanumanthaiahgowdaNo ratings yet

- LTC exemption and tax on retrenchment compensationDocument2 pagesLTC exemption and tax on retrenchment compensationhanumanthaiahgowdaNo ratings yet

- FA - Problem 1Document1 pageFA - Problem 1hanumanthaiahgowdaNo ratings yet

- HP - Interest CalculationDocument4 pagesHP - Interest CalculationhanumanthaiahgowdaNo ratings yet

- Income From House PropertyDocument32 pagesIncome From House PropertyhanumanthaiahgowdaNo ratings yet

- FA - Problem 8Document1 pageFA - Problem 8hanumanthaiahgowdaNo ratings yet

- IFHP - ProblemsDocument2 pagesIFHP - ProblemshanumanthaiahgowdaNo ratings yet

- E-Commerce HistoryDocument2 pagesE-Commerce HistoryhanumanthaiahgowdaNo ratings yet

- Session 5Document6 pagesSession 5hanumanthaiahgowdaNo ratings yet

- Why Is It Important?: Exchange and Progression of Goods - Marketing Is HighlyDocument11 pagesWhy Is It Important?: Exchange and Progression of Goods - Marketing Is HighlyhanumanthaiahgowdaNo ratings yet

- IGCSE Accounting Chapter 1-3 Exam Questions by Mrs Sana AbdullahDocument7 pagesIGCSE Accounting Chapter 1-3 Exam Questions by Mrs Sana AbdullahMeredith TwinnNo ratings yet

- FSI Financial Statements SummaryDocument14 pagesFSI Financial Statements SummaryEmosNo ratings yet

- Chapter 9 - Interim Financial ReportingDocument8 pagesChapter 9 - Interim Financial ReportingXiena0% (1)

- Engineering Economics Course OverviewDocument2 pagesEngineering Economics Course OverviewAnil MarsaniNo ratings yet

- TUI AG Bericht 2019 ENDocument48 pagesTUI AG Bericht 2019 ENgoggsNo ratings yet

- BV2018 - MFRS 141Document15 pagesBV2018 - MFRS 141iqbalhakim123No ratings yet

- Ais ExerciseDocument26 pagesAis ExerciseLele DongNo ratings yet

- MSU-CBA Finance Lease Accounting ConceptsDocument4 pagesMSU-CBA Finance Lease Accounting ConceptsJayr BVNo ratings yet

- Perez Long Quiz Auditing and Assurance Concepts and ApplicationDocument7 pagesPerez Long Quiz Auditing and Assurance Concepts and ApplicationMitch MinglanaNo ratings yet

- Accounting InformationDocument3 pagesAccounting Informationnenette cruzNo ratings yet

- Overview of Indian Accounting Standards For SMEsDocument44 pagesOverview of Indian Accounting Standards For SMEsSamrat JonejaNo ratings yet

- IAS 41 Agriculture OverviewDocument45 pagesIAS 41 Agriculture OverviewEmily Rose ZafeNo ratings yet

- Manufacturing and Trading AccountsDocument5 pagesManufacturing and Trading AccountsFarrukhsgNo ratings yet

- Infocept Pte LTD - 2021Document47 pagesInfocept Pte LTD - 2021Lin ZincNo ratings yet

- Model Question Paper for Valuation ExamDocument16 pagesModel Question Paper for Valuation ExamAnshul Chauhan50% (2)

- Final Exam - FA PDFDocument7 pagesFinal Exam - FA PDFNga NguyễnNo ratings yet

- Auditing Problems 2Document8 pagesAuditing Problems 2Rujean Salar AltejarNo ratings yet

- Step by Step Guide On Discounted Cash Flow Valuation Model - Fair Value AcademyDocument25 pagesStep by Step Guide On Discounted Cash Flow Valuation Model - Fair Value AcademyIkhlas SadiminNo ratings yet

- Chapter 3 Target CostingDocument32 pagesChapter 3 Target CostingĐạt DươngNo ratings yet

- Infrastructure Asset Register MaintenanceDocument19 pagesInfrastructure Asset Register MaintenanceTino MatsvayiNo ratings yet

- 11 x09 Capital BudgetingDocument29 pages11 x09 Capital BudgetingKatherine Cabading Inocando100% (10)

- All Subj - Mock Board Exam BBDocument9 pagesAll Subj - Mock Board Exam BBMJ YaconNo ratings yet

- 5Document2 pages5ABDUL WAHABNo ratings yet

- M5&M6 SC - Other AJE & WorksheetDocument47 pagesM5&M6 SC - Other AJE & WorksheetLady Ysabel HechanovaNo ratings yet

- Acc05 Far Handout 7Document5 pagesAcc05 Far Handout 7Jullia BelgicaNo ratings yet

- Chemical Process Design Analysis NPVDocument7 pagesChemical Process Design Analysis NPVHaematomaNo ratings yet

- Partnership Dissolution and Admission ExplainedDocument14 pagesPartnership Dissolution and Admission ExplainedMila aguasanNo ratings yet

- Assignment Chapter 2 SOLUTIONDocument6 pagesAssignment Chapter 2 SOLUTIONBeatrice BallabioNo ratings yet

- Worktext Fabm1 Q4 W1-WokDocument19 pagesWorktext Fabm1 Q4 W1-WokQuincy Lawrence DimaanoNo ratings yet