You might also like

- Introduction To Accounting, Journal, Ledger, Trial Balance: Module - 1Document64 pagesIntroduction To Accounting, Journal, Ledger, Trial Balance: Module - 1irshan amirNo ratings yet

- Introduction To Accounting, Journal, Ledger, Trial BalanceDocument74 pagesIntroduction To Accounting, Journal, Ledger, Trial Balancethella deva prasadNo ratings yet

- Introduction To Accounting, Journal, Ledger, Trial BalanceDocument74 pagesIntroduction To Accounting, Journal, Ledger, Trial Balanceagustinn agustinNo ratings yet

- Basics of accounting presentationDocument11 pagesBasics of accounting presentationRajveer Singh SekhonNo ratings yet

- Explaining Financial AccountingDocument6 pagesExplaining Financial AccountinganishtomanishNo ratings yet

- Basics of Accounting: Mba (HRD) Delhi School of Economics Department of Commerce University of DelhiDocument15 pagesBasics of Accounting: Mba (HRD) Delhi School of Economics Department of Commerce University of DelhiMukesh DroliaNo ratings yet

- Accounting BasicsDocument7 pagesAccounting BasicsGovind SharmaNo ratings yet

- PNB Class 5Document56 pagesPNB Class 5sunil routNo ratings yet

- Accounting Concepts and Conventions by Professor & Lawyer Puttu Guru PrasadDocument9 pagesAccounting Concepts and Conventions by Professor & Lawyer Puttu Guru PrasadPUTTU GURU PRASAD SENGUNTHA MUDALIARNo ratings yet

- Accounting basicsDocument24 pagesAccounting basicsRoshan JhaNo ratings yet

- Acc PDFDocument61 pagesAcc PDFSmarika BistNo ratings yet

- Financial AccountingDocument16 pagesFinancial AccountingSNo ratings yet

- Fundamental Principles of Accounting ExplainedDocument37 pagesFundamental Principles of Accounting ExplainedAnuja SandbhorNo ratings yet

- Accounting Terminology: By: Dr. Deepika Saxena Associate Professor, JIMSDocument20 pagesAccounting Terminology: By: Dr. Deepika Saxena Associate Professor, JIMSumangNo ratings yet

- MC1404 - Unit 2Document111 pagesMC1404 - Unit 2Senthil KumarNo ratings yet

- Basics of Accounting and Book KeepingDocument16 pagesBasics of Accounting and Book KeepingPuneet DhuparNo ratings yet

- Accounting and Financial MangementDocument25 pagesAccounting and Financial MangementSHASHINo ratings yet

- Accounting concepts and financial statements explainedDocument10 pagesAccounting concepts and financial statements explainedHimanshu JoshiNo ratings yet

- CLASS XI ACCOUNTANCY NOTES Chapter 2 - Theory Base of AccountingDocument26 pagesCLASS XI ACCOUNTANCY NOTES Chapter 2 - Theory Base of AccountingPradyumna ChoudharyNo ratings yet

- CBSE Quick Revision Notes and Chapter Summary: Class-11 Accountancy Chapter 2 - Theory Base of AccountingDocument9 pagesCBSE Quick Revision Notes and Chapter Summary: Class-11 Accountancy Chapter 2 - Theory Base of AccountingPrashant JoshiNo ratings yet

- Financial Accounting InsightsDocument10 pagesFinancial Accounting InsightsTeChtroNiCS [AK]No ratings yet

- Introduction To AccountingDocument18 pagesIntroduction To AccountingAutoDefenceNo ratings yet

- CSI Tally AcademyDocument59 pagesCSI Tally AcademyCSI TallyNo ratings yet

- Balance Sheet Dimasaka & JaranillaDocument56 pagesBalance Sheet Dimasaka & JaranillaShaneBattierNo ratings yet

- Accounting basics for business decisionsDocument14 pagesAccounting basics for business decisionsKaran Singh RathoreNo ratings yet

- 2. Chap 2 Book Keeping and Accounting and Basic TerminologiesDocument4 pages2. Chap 2 Book Keeping and Accounting and Basic Terminologiesyousaf.mast777No ratings yet

- Accounting Concepts and Conventions ExplainedDocument61 pagesAccounting Concepts and Conventions ExplainedJAY Solanki100% (1)

- Chapter 1Document23 pagesChapter 1mahiramazoon mazoonNo ratings yet

- Download the original attachment - The complete basics of accountingDocument32 pagesDownload the original attachment - The complete basics of accountingvijayNo ratings yet

- Basic Accounting Terms: By: Shivani ChandelDocument29 pagesBasic Accounting Terms: By: Shivani ChandelDheeraj KumarNo ratings yet

- BBddFY Business AccountingDocument24 pagesBBddFY Business AccountingMehul KumarNo ratings yet

- UNIT 5 ACDocument12 pagesUNIT 5 ACBCA SY 63 Aaditi RanawareNo ratings yet

- Notes-N-Unit-2-Starting To Cash Book (ALL) - .Document93 pagesNotes-N-Unit-2-Starting To Cash Book (ALL) - .happy lifeNo ratings yet

- Basic NoteDocument8 pagesBasic Noteworld2learnNo ratings yet

- PC-14 - Day 1 - Session-1 - 22.03.2023Document14 pagesPC-14 - Day 1 - Session-1 - 22.03.2023Ajaya SahooNo ratings yet

- Accounting for Business CommunicationDocument24 pagesAccounting for Business Communicationsebastion thomasNo ratings yet

- Introduction NotesDocument4 pagesIntroduction NotesWarrioropNo ratings yet

- Introduction To Accounting Introduction To Accounting Introduction To AccountingDocument23 pagesIntroduction To Accounting Introduction To Accounting Introduction To AccountingAsitha AjayanNo ratings yet

- Accounting TheoryDocument9 pagesAccounting TheoryLokesh AggarwalNo ratings yet

- Accounting Basics ExplainedDocument25 pagesAccounting Basics Explainedjayadevsr2380No ratings yet

- Accountingnit Jamshedpur NotesDocument47 pagesAccountingnit Jamshedpur NotesSuraj KumarNo ratings yet

- Accounting-Trainer NepalDocument36 pagesAccounting-Trainer NepalSandeep UpretiNo ratings yet

- Rules and principles govern accountingDocument22 pagesRules and principles govern accountingMartha AntonNo ratings yet

- SEM - I Study Material on Basic Accounting ConceptsDocument62 pagesSEM - I Study Material on Basic Accounting Conceptssagar sheralNo ratings yet

- Accounting BasicsDocument9 pagesAccounting BasicsAnkon Gopal BanikNo ratings yet

- Understanding Basic Accounting TermsDocument17 pagesUnderstanding Basic Accounting TermsShoryamann SharmaNo ratings yet

- Lesson 8 Elements of FsDocument53 pagesLesson 8 Elements of FsSoothing BlendNo ratings yet

- Business AccountingDocument25 pagesBusiness AccountingYash PatawariNo ratings yet

- FinanceDocument48 pagesFinanceMimi Adriatico JaranillaNo ratings yet

- MBR517 Lect 01Document30 pagesMBR517 Lect 01Updyfitah TahlilNo ratings yet

- The Original Attachment: BasicsDocument32 pagesThe Original Attachment: BasicsVijayGogulaNo ratings yet

- Basics of Accounting 3 Double Entry Book Keeping RulesDocument44 pagesBasics of Accounting 3 Double Entry Book Keeping Rulesjiten zopeNo ratings yet

- What Is Financial Management?Document43 pagesWhat Is Financial Management?Jonas AlcantaraNo ratings yet

- What Is Accounting ?: PDF HandoutDocument5 pagesWhat Is Accounting ?: PDF Handoutshreya partiNo ratings yet

- Trading Basics: AccountingDocument10 pagesTrading Basics: AccountingNonameforeverNo ratings yet

- 11 Accountancy Keynotes Ch02 Theory Base of Accounting VKDocument9 pages11 Accountancy Keynotes Ch02 Theory Base of Accounting VKAnonymous 1Zepq14UarNo ratings yet

- Tally ERP9Document68 pagesTally ERP9Jinesh100% (1)

- Accounting Period Shareholders DividendsDocument3 pagesAccounting Period Shareholders DividendsAmaranathreddy YgNo ratings yet

- Accounting Training OverviewDocument74 pagesAccounting Training Overviewzee_iitNo ratings yet

- Lecture 6Document14 pagesLecture 6Kertik SinghNo ratings yet

- Worksheet 1.2Document1 pageWorksheet 1.2Kertik SinghNo ratings yet

- Ishu Worksheet 1Document7 pagesIshu Worksheet 1Kertik SinghNo ratings yet

- Worksheet 1.1Document1 pageWorksheet 1.1Kertik SinghNo ratings yet

- Aditya Solanki Expriment No.3Document5 pagesAditya Solanki Expriment No.3Kertik SinghNo ratings yet

- Lecture 4Document16 pagesLecture 4Kertik SinghNo ratings yet

- Lecture 20Document16 pagesLecture 20Kertik SinghNo ratings yet

- Ishu Worksheet 2Document6 pagesIshu Worksheet 2Kertik SinghNo ratings yet

- Financial ReformsDocument21 pagesFinancial ReformsKertik SinghNo ratings yet

- Lect Topic 3.2 DisinvestmentDocument23 pagesLect Topic 3.2 DisinvestmentKertik SinghNo ratings yet

- Understanding Business Environment FactorsDocument22 pagesUnderstanding Business Environment FactorsKertik SinghNo ratings yet

- Institute-University School of Business Department-Bachelor of Business Administration Advanced Accounting (BAT - 165)Document22 pagesInstitute-University School of Business Department-Bachelor of Business Administration Advanced Accounting (BAT - 165)Kertik SinghNo ratings yet

- Lecture Topic 1.2 ENVIORNMENT SCANNING TECHNIQUESDocument35 pagesLecture Topic 1.2 ENVIORNMENT SCANNING TECHNIQUESKertik Singh100% (1)

- Understanding Business EnvironmentDocument22 pagesUnderstanding Business EnvironmentKertik SinghNo ratings yet

- Understanding the Economic EnvironmentDocument35 pagesUnderstanding the Economic EnvironmentKertik SinghNo ratings yet

- Elements of Financial StatementDocument33 pagesElements of Financial StatementKertik Singh100% (1)

- UNEMPLOYMENT FinalDocument18 pagesUNEMPLOYMENT FinalKertik SinghNo ratings yet

- Channel Management DistributionDocument65 pagesChannel Management DistributionKertik SinghNo ratings yet

- Operational Research (Unit 3)Document14 pagesOperational Research (Unit 3)Kertik SinghNo ratings yet

- Types of DepressionDocument7 pagesTypes of DepressionKertik SinghNo ratings yet

- Accounting Principles for Business StudentsDocument26 pagesAccounting Principles for Business StudentsKertik SinghNo ratings yet

- Promotion & DistributionDocument18 pagesPromotion & DistributionKertik SinghNo ratings yet

- Unemployment: - Hunger Is Not The Worst Feature of Unemployment Idleness IsDocument4 pagesUnemployment: - Hunger Is Not The Worst Feature of Unemployment Idleness IsKertik SinghNo ratings yet

- Operational Research (Unit 2)Document20 pagesOperational Research (Unit 2)Kertik SinghNo ratings yet

- Social and Professional Ethics-1Document78 pagesSocial and Professional Ethics-1Kertik SinghNo ratings yet

- Advertising and Sales PromotionDocument15 pagesAdvertising and Sales PromotionKertik SinghNo ratings yet

- What Is Meant by Deferred COGS in R12Document3 pagesWhat Is Meant by Deferred COGS in R12devender143No ratings yet

- IFRS 16 and IAS 36: How Changes in Lease Accounting Will Impact Your Impairment Testing ProcessesDocument4 pagesIFRS 16 and IAS 36: How Changes in Lease Accounting Will Impact Your Impairment Testing ProcessesHamada Asmr Aladham100% (1)

- Liability of Parent Company in A Subsidiary CompanyDocument9 pagesLiability of Parent Company in A Subsidiary CompanyAvaniAyuNo ratings yet

- Quiz Partnership 1Document2 pagesQuiz Partnership 1Arj Sulit Centino DaquiNo ratings yet

- 14-6: A (At Fair Value at Date of Acquisition) 14-7: D: Total Net Income P1,800,000Document26 pages14-6: A (At Fair Value at Date of Acquisition) 14-7: D: Total Net Income P1,800,000Love FreddyNo ratings yet

- Accounting System-Special Journals Accounting System - Special JournalsDocument27 pagesAccounting System-Special Journals Accounting System - Special JournalsShane Jesuitas100% (1)

- Business Ownership PresentationDocument24 pagesBusiness Ownership Presentationfarie ahmadNo ratings yet

- Financial Performance Analysis of SOE Transportation and Warehousing Sector Before and During Covid-19 PandemicDocument11 pagesFinancial Performance Analysis of SOE Transportation and Warehousing Sector Before and During Covid-19 PandemicFatihah rachmah PramuditaNo ratings yet

- Law 2 ReviewerDocument10 pagesLaw 2 ReviewerXiao RodriguezNo ratings yet

- 01 Capitalized CostDocument3 pages01 Capitalized CostDexter JavierNo ratings yet

- FM-Dividend PolicyDocument9 pagesFM-Dividend PolicyMaxine SantosNo ratings yet

- IMT PatanjaliDocument4 pagesIMT PatanjalisquyenNo ratings yet

- Intermediate Accounting 1st Edition Gordon Solutions Manual 1Document61 pagesIntermediate Accounting 1st Edition Gordon Solutions Manual 1shaun100% (36)

- Final AssignmentDocument6 pagesFinal AssignmentTalimur RahmanNo ratings yet

- Company Law Subject Code and CreditsDocument3 pagesCompany Law Subject Code and CreditsCrystal CaveNo ratings yet

- CHP 1 and 2 BbaDocument73 pagesCHP 1 and 2 BbaBarkkha MakhijaNo ratings yet

- ST439 - Chapter 1: Financial Derivatives, Binomial ModelsDocument27 pagesST439 - Chapter 1: Financial Derivatives, Binomial ModelslowchangsongNo ratings yet

- CFAS Chapter 2-7 Conceptual FrameworkDocument3 pagesCFAS Chapter 2-7 Conceptual FrameworkKaren CaelNo ratings yet

- How Unethical Practices Almost Destroyed WorldcomDocument16 pagesHow Unethical Practices Almost Destroyed WorldcomtodkarvijayNo ratings yet

- WMCC Assignment 15TH AprilDocument18 pagesWMCC Assignment 15TH AprilRamya GowdaNo ratings yet

- FABM 2 Lesson 6 CFSDocument28 pagesFABM 2 Lesson 6 CFSKia MorenoNo ratings yet

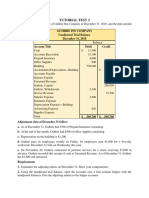

- Tutorial Test 3Document2 pagesTutorial Test 3b1112014041No ratings yet

- Unsecured Bond: Why Issue Unsecured Bonds?Document2 pagesUnsecured Bond: Why Issue Unsecured Bonds?aeman hassan100% (1)

- Vossmann Industrial Sdn. Bhd. - DennisDocument6 pagesVossmann Industrial Sdn. Bhd. - Dennisnishio fdNo ratings yet

- Adani Group - How The World's 3rd Richest Man Is Pulling The Largest Con in Corporate History - Hindenburg ResearchDocument90 pagesAdani Group - How The World's 3rd Richest Man Is Pulling The Largest Con in Corporate History - Hindenburg ResearchmallikarjunbpatilNo ratings yet

- LLP Act Guide Explains Limited Liability Partnership RulesDocument7 pagesLLP Act Guide Explains Limited Liability Partnership RulesMaygie KeiNo ratings yet

- RWJ FCF11e Chap 02Document25 pagesRWJ FCF11e Chap 02kaylakshmiNo ratings yet

- Regulatory Framework for Business TransactionsDocument23 pagesRegulatory Framework for Business TransactionsJasmine Marie Ng Cheong0% (1)

- General Mathematics: Quarter 2 - Module 10: Market Indices For Stocks and BondsDocument32 pagesGeneral Mathematics: Quarter 2 - Module 10: Market Indices For Stocks and BondsDon't mind meNo ratings yet