You might also like

- Calculating Food CostDocument15 pagesCalculating Food CostRheneir Mora50% (2)

- Restaurant Inventory Management: Reducing Food Costs Using Actual vs. Theoretical ToolsDocument3 pagesRestaurant Inventory Management: Reducing Food Costs Using Actual vs. Theoretical ToolsViny Vini100% (1)

- LCCM Research Digest (November-December 2007 Ed.)Document4 pagesLCCM Research Digest (November-December 2007 Ed.)mis_administratorNo ratings yet

- Development of Robotic Arm Using Arduino Uno: Priyambada Mishra, Riki Patel, Trushit Upadhyaya, Arpan DesaiDocument9 pagesDevelopment of Robotic Arm Using Arduino Uno: Priyambada Mishra, Riki Patel, Trushit Upadhyaya, Arpan Desaihussien amareNo ratings yet

- Design, Analysis and Manufacturing of Four Degree of Freedom Wireless (Wi-Fi) Controlled Robotic ARMDocument12 pagesDesign, Analysis and Manufacturing of Four Degree of Freedom Wireless (Wi-Fi) Controlled Robotic ARMMasood Akhtar VaheedNo ratings yet

- Standard Portion CostDocument22 pagesStandard Portion CostAntonette HernandezNo ratings yet

- Introduction To Robotics'Document12 pagesIntroduction To Robotics'rahul bhattNo ratings yet

- ServiceManual UR10 en 2.0.5Document100 pagesServiceManual UR10 en 2.0.5alexNo ratings yet

- Menu PricingDocument18 pagesMenu PricingtreeknoxNo ratings yet

- Robotics 1Document24 pagesRobotics 1Rahul RoyNo ratings yet

- Dolinsky ThesisDocument183 pagesDolinsky Thesisvelo123No ratings yet

- Geometric Modeling and Singularity of 6 DOF FanucDocument7 pagesGeometric Modeling and Singularity of 6 DOF FanucDavid Rogelio Alvarez ReyesNo ratings yet

- Full ThesisDocument100 pagesFull ThesisMarcus Vinícius Campos OliveiraNo ratings yet

- Careers in Law: Below Is A List of Popular Legal and Law-Related CareersDocument1 pageCareers in Law: Below Is A List of Popular Legal and Law-Related CareersKayeNo ratings yet

- Robotic Motor ReportDocument41 pagesRobotic Motor ReportNehul PatilNo ratings yet

- Value Chain Analysis of Seaweed in Aceh, IndonesiaDocument21 pagesValue Chain Analysis of Seaweed in Aceh, IndonesiaEly John KarimelaNo ratings yet

- Robotic Arm Dynamic and Simulation With Virtual Re PDFDocument7 pagesRobotic Arm Dynamic and Simulation With Virtual Re PDFALA SOUISSINo ratings yet

- Thesis SahaDocument143 pagesThesis SahaAlen RozajacNo ratings yet

- Recipe Costing Form: M N - P Q #3 D - A T QDocument8 pagesRecipe Costing Form: M N - P Q #3 D - A T QKiran GadmaleNo ratings yet

- Biodegradable PlasticDocument21 pagesBiodegradable PlasticPRALAY GEDAMNo ratings yet

- Cost ControlDocument4 pagesCost ControlGennie100% (1)

- Calculating Food CostDocument15 pagesCalculating Food CostCharlene MohanNo ratings yet

- Laboratory Exercise EvaDocument19 pagesLaboratory Exercise EvaZhen Chin Tolentino ChengNo ratings yet

- Costing Cert IIIDocument8 pagesCosting Cert IIIlathikaNo ratings yet

- Recipe Plate Cost Template v3Document7 pagesRecipe Plate Cost Template v3Sherwin Cabueñas Sarmiento100% (1)

- Chapter 7 - Recipe and Menu Costing - Introduction To Food Production and Service (1) (JOJO)Document1 pageChapter 7 - Recipe and Menu Costing - Introduction To Food Production and Service (1) (JOJO)johari22sethNo ratings yet

- Standard Portion Cost (Objectives & Cost Cards) - Production ControlDocument2 pagesStandard Portion Cost (Objectives & Cost Cards) - Production Controlshamlee ramtekeNo ratings yet

- CulinaryMath RecipeCosting PDFDocument4 pagesCulinaryMath RecipeCosting PDFJakiki TVNo ratings yet

- Assignment Activity-Assessment 2Document26 pagesAssignment Activity-Assessment 2bhupi5No ratings yet

- Project Plan Cookery 10Document11 pagesProject Plan Cookery 10milk teaNo ratings yet

- Recipe-Plate-Cost-Template_v3Document8 pagesRecipe-Plate-Cost-Template_v3vmtechnologyvkmNo ratings yet

- Culinary Math FormulasDocument11 pagesCulinary Math FormulasShane Reinhart100% (5)

- NOTE2Document4 pagesNOTE2ayekhaseseNo ratings yet

- Recipe Plate Cost Template - FOHO1024Document6 pagesRecipe Plate Cost Template - FOHO1024Dat LamNo ratings yet

- Culinary Math Lesson on Yield Percent, Costing Recipes & BeveragesDocument10 pagesCulinary Math Lesson on Yield Percent, Costing Recipes & BeveragescindibellamyNo ratings yet

- Menu Item Forecasting and Inventory ControlDocument62 pagesMenu Item Forecasting and Inventory ControlLeo Patrick CabrigasNo ratings yet

- Recipe Plate Cost Template v3Document7 pagesRecipe Plate Cost Template v3విజయ్ పిNo ratings yet

- Yield TestDocument15 pagesYield TestCanant Tepatipya100% (1)

- Recipe Costing Template Salmon & spinachDocument13 pagesRecipe Costing Template Salmon & spinachJaskarn Singh Dhonkal100% (3)

- Finding the Cost of Prosciutto for a Wedding Brunch (230 guestsDocument12 pagesFinding the Cost of Prosciutto for a Wedding Brunch (230 guestsfugaperuNo ratings yet

- Assignment Activity-Assessment 2Document10 pagesAssignment Activity-Assessment 2bhupi5No ratings yet

- Chapter 6 Food Production Control - PortionsDocument24 pagesChapter 6 Food Production Control - PortionsshuhadaNo ratings yet

- Foods II Prequel E5 Standardizing and Scaling RecipesEDocument21 pagesFoods II Prequel E5 Standardizing and Scaling RecipesEJACKILYN JURINo ratings yet

- Hot and Cold Apps Danielle DuranDocument26 pagesHot and Cold Apps Danielle DuranDanielle DuranNo ratings yet

- Calculatecostofproduction 230128091409 37f7c731Document21 pagesCalculatecostofproduction 230128091409 37f7c731kunejoseNo ratings yet

- Setting Selling Price for Cheesy Eggplant LayerDocument7 pagesSetting Selling Price for Cheesy Eggplant LayerJeyan NyleNo ratings yet

- Basic Culinary Math - PptsDocument39 pagesBasic Culinary Math - PptsfugaperuNo ratings yet

- Recipe Costing TemplateDocument37 pagesRecipe Costing TemplateStacy Parker100% (1)

- Ala Carte MainDocument3 pagesAla Carte MainSundas AnsariNo ratings yet

- Assignment Activity-Assessment 2Document26 pagesAssignment Activity-Assessment 2bhupi5No ratings yet

- Butchers Yield Test GuideDocument4 pagesButchers Yield Test GuideGladys LadromaNo ratings yet

- 02 Handout 2 (2) CostingDocument3 pages02 Handout 2 (2) CostingLuis De CastroNo ratings yet

- Steps to Easier Quantity Food ProductionDocument6 pagesSteps to Easier Quantity Food ProductionGuilfred Flores AtienzaNo ratings yet

- Most Essential Learning CompetenciesDocument19 pagesMost Essential Learning CompetenciesLaila Idaloy Arcillas100% (6)

- A1 SITHKOP002 Worksheets Ver April 2018Document11 pagesA1 SITHKOP002 Worksheets Ver April 2018Pitaram Panthi100% (1)

- Activity Performance Worksheet in TLE (Cookery) : Quarter 1: Week 7Document8 pagesActivity Performance Worksheet in TLE (Cookery) : Quarter 1: Week 7Jhomari Mollejon DiazNo ratings yet

- Restaurant Concept PowerpointDocument9 pagesRestaurant Concept PowerpointMiguel SantiagoNo ratings yet

- Riesling Baked PearsDocument2 pagesRiesling Baked Pearsjyoti soodNo ratings yet

- Recipe Costing TemplateDocument19 pagesRecipe Costing TemplateAnzel AnzelNo ratings yet

- AP and+EP+WeightDocument19 pagesAP and+EP+WeightHoyJing ChewNo ratings yet

- bpp1 Second Quarter QUICKBREADSDocument23 pagesbpp1 Second Quarter QUICKBREADSVergie Cambi EsturasNo ratings yet

- Chapter 8Document34 pagesChapter 8Gene Roy P. HernandezNo ratings yet

- Fudserve Course ModuleDocument15 pagesFudserve Course ModuleGene Roy P. HernandezNo ratings yet

- Baking Session 1Document4 pagesBaking Session 1Gene Roy P. HernandezNo ratings yet

- Cookies 101.Document43 pagesCookies 101.Gene Roy P. HernandezNo ratings yet

- The New Marketing Mix Approach of Hospitality andDocument5 pagesThe New Marketing Mix Approach of Hospitality andGene Roy P. HernandezNo ratings yet

- Module 4 Assess The Challenges and Opportunities WorksheetDocument2 pagesModule 4 Assess The Challenges and Opportunities WorksheetGene Roy P. HernandezNo ratings yet

- Chapter 6Document2 pagesChapter 6Gene Roy P. HernandezNo ratings yet

- Recipe Ni DaenielDocument1 pageRecipe Ni DaenielGene Roy P. HernandezNo ratings yet

- APPENDICESDocument29 pagesAPPENDICESGene Roy P. HernandezNo ratings yet

- Housekeeping RubricsDocument2 pagesHousekeeping RubricsGene Roy P. Hernandez100% (2)

- Rubric For Napkin Folds Table Setting and ServiceDocument2 pagesRubric For Napkin Folds Table Setting and ServiceGene Roy P. Hernandez100% (3)

- Executive SummaryDocument2 pagesExecutive SummaryGene Roy P. HernandezNo ratings yet

- Chapter 1&2 DRTHDRTDDocument30 pagesChapter 1&2 DRTHDRTDGene Roy P. HernandezNo ratings yet

- Case Analysis For MIS...Document5 pagesCase Analysis For MIS...Gene Roy P. HernandezNo ratings yet

- Balance Sheet Financial StatementDocument3 pagesBalance Sheet Financial StatementGene Roy P. HernandezNo ratings yet

- Haiti Mangoes Social Enterprise SolutionDocument4 pagesHaiti Mangoes Social Enterprise SolutionGene Roy P. HernandezNo ratings yet

- For Survey QuestionnaireDocument2 pagesFor Survey QuestionnaireGene Roy P. HernandezNo ratings yet

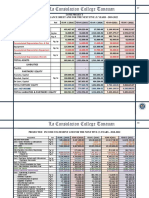

- La Consolacion College Tanauan: Preliminary Examination (SY: 2018-2019/ 2 Semester)Document4 pagesLa Consolacion College Tanauan: Preliminary Examination (SY: 2018-2019/ 2 Semester)Gene Roy P. HernandezNo ratings yet

- Case AnalysisDocument2 pagesCase AnalysisGene Roy P. HernandezNo ratings yet

- Problem 3Document1 pageProblem 3Gene Roy P. HernandezNo ratings yet

- Catering and Banqueting Management Practical Examination: "Eat All You Can Breakfast at Consuelo's Garden"Document5 pagesCatering and Banqueting Management Practical Examination: "Eat All You Can Breakfast at Consuelo's Garden"Gene Roy P. HernandezNo ratings yet

- Table Setting ContestDocument6 pagesTable Setting ContestMhel Demabogte100% (1)

- Cruise Package EvaluationDocument1 pageCruise Package EvaluationGene Roy P. HernandezNo ratings yet

- Cost of Good Sold Expenses Net Profit Income TaxDocument1 pageCost of Good Sold Expenses Net Profit Income TaxGene Roy P. HernandezNo ratings yet

- Western Cisine Final Examination DocumentationDocument19 pagesWestern Cisine Final Examination DocumentationGene Roy P. HernandezNo ratings yet

- Haiti Mangoes Social Enterprise SolutionDocument4 pagesHaiti Mangoes Social Enterprise SolutionGene Roy P. HernandezNo ratings yet

- Letter of Appointment Cub AdviserDocument6 pagesLetter of Appointment Cub AdviserGene Roy P. HernandezNo ratings yet

- Pizza DoughDocument2 pagesPizza DoughGene Roy P. HernandezNo ratings yet

- Sithccc 020 Final Marking Guide Work Effectively As A CookDocument5 pagesSithccc 020 Final Marking Guide Work Effectively As A CookBaljeet SinghNo ratings yet

- Food Safety Implementation ProgramDocument138 pagesFood Safety Implementation Programabdul qudoosNo ratings yet

- ReadymixDocument113 pagesReadymixgururajanNo ratings yet

- GAF686 - Recipe BookDocument68 pagesGAF686 - Recipe Bookerwin_betancourt_2No ratings yet

- Mexican Home Cooking - 2 Books in 1 - 77 Recipes (x2) Cookbook To Prepare Mexican Food at Home-Pages-32Document6 pagesMexican Home Cooking - 2 Books in 1 - 77 Recipes (x2) Cookbook To Prepare Mexican Food at Home-Pages-32KowiWaltzNo ratings yet

- Franke CR 66 M WH-1 Oven PDFDocument148 pagesFranke CR 66 M WH-1 Oven PDFCecilia Di YorioNo ratings yet

- Soap CalculatorDocument23 pagesSoap CalculatorsurfingyoginiNo ratings yet

- Paulo and Bill Lunch MenuDocument2 pagesPaulo and Bill Lunch Menusupport_local_flavorNo ratings yet

- Anna Maria Oyster Bar Dinner MenuDocument2 pagesAnna Maria Oyster Bar Dinner Menusupport_local_flavorNo ratings yet

- A) Cereal and Cereal ProductsDocument11 pagesA) Cereal and Cereal ProductsMubasher SaleemNo ratings yet

- Diet PlanDocument4 pagesDiet Pland_tantubaiNo ratings yet

- مفرداتDocument34 pagesمفرداتاحمد خيراللهNo ratings yet

- IIFYM Flexible Dieting Bodybuilding Guide Recipe Book Top 10 RecipesDocument10 pagesIIFYM Flexible Dieting Bodybuilding Guide Recipe Book Top 10 Recipessean griffinNo ratings yet

- Pengaruh Penambahan Daging Ikan Mujair Terhadap Sifat Organoleptik Abon Ampas Tahu Ikan Mujair (Abon Atm)Document6 pagesPengaruh Penambahan Daging Ikan Mujair Terhadap Sifat Organoleptik Abon Ampas Tahu Ikan Mujair (Abon Atm)Meist UntariNo ratings yet

- School of Hospitality Ypj Johor Bahru Culinary Artistry (DCA 2093) Individual Report Prepared ForDocument21 pagesSchool of Hospitality Ypj Johor Bahru Culinary Artistry (DCA 2093) Individual Report Prepared ForNUR AMIRAH NATASYA BINTI ABUNo ratings yet

- Ts10 Chuyên 1920 DBDocument7 pagesTs10 Chuyên 1920 DBNgô Tấn DũngNo ratings yet

- Philippine Christian University: Risk Management AS Applied TO Safety, Security & SanitationDocument7 pagesPhilippine Christian University: Risk Management AS Applied TO Safety, Security & SanitationalexisNo ratings yet

- Price List in Dollar and Naira EquivalentDocument5 pagesPrice List in Dollar and Naira EquivalentDaniel Chukwuka UzoNo ratings yet

- Master Soal X GanjilDocument12 pagesMaster Soal X GanjilUmie SafitriNo ratings yet

- Dearborn Fundraiser Order Form 2022Document1 pageDearborn Fundraiser Order Form 2022api-260909045No ratings yet

- CYPRUSDocument24 pagesCYPRUSIoana BrîndăuNo ratings yet

- GROUP 5 - FortitudeDocument26 pagesGROUP 5 - Fortitudejjbghwq9xdNo ratings yet

- Modele de Teste Online Intensiv Engleza Clasa 5 - Global-LearningDocument1 pageModele de Teste Online Intensiv Engleza Clasa 5 - Global-LearningSimonaElena100% (2)

- The Big Book of Keto Diet Cooking - 200 Quick & Easy 2020 PDFDocument432 pagesThe Big Book of Keto Diet Cooking - 200 Quick & Easy 2020 PDFgelu vitelariu100% (3)

- 13 fn41 2 05 Kitchen MathDocument2 pages13 fn41 2 05 Kitchen Mathapi-3293211400% (5)

- Beach BBQDocument32 pagesBeach BBQDraq ShoruNo ratings yet

- Speakout-2nd-Ed-Placement-TestDocument16 pagesSpeakout-2nd-Ed-Placement-TestНаталья УлановаNo ratings yet

- Oriya To English Translations of Popular IngredientsDocument3 pagesOriya To English Translations of Popular IngredientsBhagirathi SahuNo ratings yet

- Unit 7 Recipes and Eating HabitsDocument13 pagesUnit 7 Recipes and Eating HabitsRaphaël DurandNo ratings yet

- Prepare and Produce Pastry ProductDocument36 pagesPrepare and Produce Pastry ProductMarlon Martin100% (1)