You might also like

- Formation of Capital (Shares)Document9 pagesFormation of Capital (Shares)Mahima ChaudharyNo ratings yet

- Presented By: Nosheen Mehfooz M.Awais Anum Aziz M.Shayan S. Hammad S. Rameez KhalidDocument19 pagesPresented By: Nosheen Mehfooz M.Awais Anum Aziz M.Shayan S. Hammad S. Rameez KhalidNOSHEEN MEHFOOZNo ratings yet

- CH 1 - Issue of SharesDocument44 pagesCH 1 - Issue of Shares21BCO097 ChelsiANo ratings yet

- Accounting For Share CapitalDocument38 pagesAccounting For Share CapitalAadi PunjabiNo ratings yet

- Introducti On T o C Ompany: Meaning of CompanyDocument5 pagesIntroducti On T o C Ompany: Meaning of CompanyTruecaller CheckNo ratings yet

- Business LawDocument15 pagesBusiness LawHimanshi YadavNo ratings yet

- Companies Act, 2013: Legal Aspects of Business Prof. Mehek KapoorDocument15 pagesCompanies Act, 2013: Legal Aspects of Business Prof. Mehek KapoorAman jaiNo ratings yet

- Notes - Share CapitalDocument32 pagesNotes - Share CapitalHeer SirwaniNo ratings yet

- Business LawDocument8 pagesBusiness Lawankita mishraNo ratings yet

- ISSUE OF SHARES - SACHIN TheoryDocument8 pagesISSUE OF SHARES - SACHIN Theorydakshparashar973No ratings yet

- What is a DebentureDocument30 pagesWhat is a DebentureRITIKANo ratings yet

- Unit 1: Introduction To Company AccountsDocument16 pagesUnit 1: Introduction To Company AccountspoojaNo ratings yet

- Types of Business Structures in the PhilippinesDocument7 pagesTypes of Business Structures in the PhilippinesBusiness100% (1)

- Company Law Assignment Share CapitalDocument14 pagesCompany Law Assignment Share Capitalharsh mittalNo ratings yet

- 67187bos54090 Cp10u2Document45 pages67187bos54090 Cp10u2Ashutosh PandeyNo ratings yet

- Law Implications in BusinessDocument5 pagesLaw Implications in Businessrocken samiunNo ratings yet

- Chapter # 3: Accounting For Company - Issuance of Shares & DebenturesDocument26 pagesChapter # 3: Accounting For Company - Issuance of Shares & DebenturesFahad BataviaNo ratings yet

- Equity Securities Market 1 PDFDocument30 pagesEquity Securities Market 1 PDFAlmira LozanoNo ratings yet

- accountingforsharecapital-160107074250Document47 pagesaccountingforsharecapital-160107074250nemewep527No ratings yet

- Corporate Accounting1Document58 pagesCorporate Accounting1Dhamodharan MNo ratings yet

- Corporate Restructuring: by Bharat Sai Kiran Ashok LahotyDocument26 pagesCorporate Restructuring: by Bharat Sai Kiran Ashok LahotyGeorgeNo ratings yet

- Taxmann's Company Law Chapter 3Document25 pagesTaxmann's Company Law Chapter 3Anushka BhanjaNo ratings yet

- Acads SEBI Companies Act NotesDocument10 pagesAcads SEBI Companies Act NotesGopinath PNo ratings yet

- Company AccountsDocument14 pagesCompany AccountsFehan' CaveNo ratings yet

- Omparative Table: Basis Shares Debentures StructureDocument2 pagesOmparative Table: Basis Shares Debentures StructureShalini Singh IPSANo ratings yet

- 67186bos54090 Cp10u1Document16 pages67186bos54090 Cp10u1Ashutosh PandeyNo ratings yet

- Corporate AccountingDocument70 pagesCorporate AccountingGayathriSrinivasanNo ratings yet

- Company LawDocument19 pagesCompany LawAakankshaNo ratings yet

- AcctheoryDocument31 pagesAcctheoryChen NuoNo ratings yet

- Weeks 10 Chapter 5. General Provisions (Republic Act No. 11232)Document6 pagesWeeks 10 Chapter 5. General Provisions (Republic Act No. 11232)Jean Paula SequiñoNo ratings yet

- Corporate AccountDocument17 pagesCorporate Accountme_sahaniNo ratings yet

- Constructive NoticeDocument13 pagesConstructive NoticeAbhishek SinghNo ratings yet

- Professional PracticeDocument19 pagesProfessional PracticeKaye ArciagaNo ratings yet

- Dissolution Partnership FirmDocument8 pagesDissolution Partnership FirmanuhyaextraNo ratings yet

- On CompanyDocument18 pagesOn Companyyatin1990No ratings yet

- Corp Acc-2 - Chap1-5-Material Updated-Sep2013Document64 pagesCorp Acc-2 - Chap1-5-Material Updated-Sep2013Pavan Kumar MylavaramNo ratings yet

- COMPANY LAW MODULE 2 SHARES AND DEBENTURESDocument74 pagesCOMPANY LAW MODULE 2 SHARES AND DEBENTURESramniwas sharmaNo ratings yet

- Accounting Volume 2 Canadian 9th Edition Horngren Solutions ManualDocument26 pagesAccounting Volume 2 Canadian 9th Edition Horngren Solutions ManualElizabethBautistadazi100% (56)

- Partnership Liability and AuthorityDocument31 pagesPartnership Liability and AuthorityJassey Jane Orapa50% (2)

- Compapy Act 5moduleDocument21 pagesCompapy Act 5moduleBasappaSarkarNo ratings yet

- Chapter 5 CorporationDocument14 pagesChapter 5 CorporationMathewos Woldemariam BirruNo ratings yet

- Share CapDocument29 pagesShare CapRabbikaNo ratings yet

- Note On Financial InstrumentsDocument5 pagesNote On Financial InstrumentsVismay GharatNo ratings yet

- Law 05 Company Law 02 Classification of Companies Notes 20170314 ParabDocument20 pagesLaw 05 Company Law 02 Classification of Companies Notes 20170314 ParabarshiNo ratings yet

- SCHEMATIC OF INDONESIAN BUSINESS ENTITY STRUCTUREDocument22 pagesSCHEMATIC OF INDONESIAN BUSINESS ENTITY STRUCTUREAlivia HasnandaNo ratings yet

- Differences between Shareholders and Debenture HoldersDocument7 pagesDifferences between Shareholders and Debenture HoldersNesanithi PariNo ratings yet

- Acc DebenturesDocument12 pagesAcc DebenturesDRISYANo ratings yet

- Study Note 7.1, Page 470 508Document39 pagesStudy Note 7.1, Page 470 508s4sahithNo ratings yet

- Chapter Five-CorporationDocument6 pagesChapter Five-Corporationbereket nigussieNo ratings yet

- Corporate Law Tutorial QuestionsDocument9 pagesCorporate Law Tutorial QuestionsSooXueJiaNo ratings yet

- 5. Company & Its FeaturesDocument15 pages5. Company & Its FeaturesAditi MusaleNo ratings yet

- Dissolution Revision FinalDocument9 pagesDissolution Revision FinalAnish MohantyNo ratings yet

- AC Theory - Pref Share, Valuation, CR, AmalgamationDocument8 pagesAC Theory - Pref Share, Valuation, CR, Amalgamationjimmyadamskl69No ratings yet

- 11_CA_Foundation_Accounts_Introduction_to_Company_Accounts_WithoutDocument45 pages11_CA_Foundation_Accounts_Introduction_to_Company_Accounts_Withoutbhawanar3950No ratings yet

- Corporation 1Document26 pagesCorporation 1Erica Faye AsaNo ratings yet

- Tutorial 7Document6 pagesTutorial 7Felicia LimNo ratings yet

- النظام الأساسي لشركة محدودة المسؤوليةDocument13 pagesالنظام الأساسي لشركة محدودة المسؤوليةKhamed Tabet100% (1)

- Corporations PDFDocument16 pagesCorporations PDFkylee MaranteeNo ratings yet

- Textbook of Urgent Care Management: Chapter 6, Business Formation and Entity StructuringFrom EverandTextbook of Urgent Care Management: Chapter 6, Business Formation and Entity StructuringNo ratings yet

- Asset Securitization A Comparative Study Between The United States and Belgium, Papeians, Jean-CharleDocument30 pagesAsset Securitization A Comparative Study Between The United States and Belgium, Papeians, Jean-Charlesalah hamoudaNo ratings yet

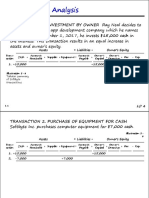

- Transaction Analysis: Transaction 1. Investment by Owner Ray Neal Decides ToDocument31 pagesTransaction Analysis: Transaction 1. Investment by Owner Ray Neal Decides ToSophia LocreNo ratings yet

- Apply Principles of Professional PracticeDocument15 pagesApply Principles of Professional PracticeBelay Kassahun100% (2)

- Universiti Teknologi Mara Final Examination: This Examination Paper Consists of 6 Printed PagesDocument6 pagesUniversiti Teknologi Mara Final Examination: This Examination Paper Consists of 6 Printed PagesAnisah NiesNo ratings yet

- 0 - Employer Employee Presentation-RevisedDocument22 pages0 - Employer Employee Presentation-Revisedreetu888No ratings yet

- STOCK AUDIT PROCEDURES AND IRREGULARITIESDocument4 pagesSTOCK AUDIT PROCEDURES AND IRREGULARITIESCma Suman Kumar VermaNo ratings yet

- Solution Manual For Ethical Obligations and Decision Making in Accounting Text and Cases 2nd Edition by MintzDocument16 pagesSolution Manual For Ethical Obligations and Decision Making in Accounting Text and Cases 2nd Edition by MintzLoriSmithamdt100% (42)

- SYBBIDocument13 pagesSYBBIshekhar landageNo ratings yet

- Solved From The Trial Balance of Girtie Lillis Attorney at Law Given inDocument1 pageSolved From The Trial Balance of Girtie Lillis Attorney at Law Given inAnbu jaromiaNo ratings yet

- Role of Technology in Digital Payments by BanksDocument30 pagesRole of Technology in Digital Payments by Bankspreeti magdumNo ratings yet

- Depreciation MethodsDocument25 pagesDepreciation Methodsluvy acerdenNo ratings yet

- BFS Unit 3Document13 pagesBFS Unit 3akileshbharathwaj2000No ratings yet

- Quality Flavors Pvt Ltd Flavor QuoteDocument2 pagesQuality Flavors Pvt Ltd Flavor QuoteSidra AnjumNo ratings yet

- Financial Decision Making Assignment SolutionsDocument2 pagesFinancial Decision Making Assignment SolutionsAbu SufianNo ratings yet

- Insurance Commission Traditional Life Reviewer QuizDocument41 pagesInsurance Commission Traditional Life Reviewer QuizSHENNA ALLAM100% (1)

- Journalizing-3-Laarni-Pascua MAINDocument7 pagesJournalizing-3-Laarni-Pascua MAINJohn DelaPazNo ratings yet

- Loan Sanction_LetterDocument2 pagesLoan Sanction_LetterDaMoN0% (1)

- New Earth mining valuation approachesDocument16 pagesNew Earth mining valuation approachesSaurabh ChhabraNo ratings yet

- Moniepoint Document 2023-12-27T10 30Document20 pagesMoniepoint Document 2023-12-27T10 30miracleikeaNo ratings yet

- Sample Personal Statement 2 0Document4 pagesSample Personal Statement 2 0Ly Hoang100% (1)

- YMO - Hand Book PDFDocument90 pagesYMO - Hand Book PDFashu jessyNo ratings yet

- Competitive Strategy of Digital Financial ServicesDocument5 pagesCompetitive Strategy of Digital Financial ServicesAfiful IchwanNo ratings yet

- Hala Arrabi Managerial Finance Assignment Chapter 3-Part 1 Multiple Choice QuestionsDocument3 pagesHala Arrabi Managerial Finance Assignment Chapter 3-Part 1 Multiple Choice QuestionsMohamad Haytham ElturkNo ratings yet

- Ibs TMN Sri Gombak, S'Gor 000010: Tarikh Masuk Butir Urusniaga Jumlah Urusniaga Baki PenyataDocument38 pagesIbs TMN Sri Gombak, S'Gor 000010: Tarikh Masuk Butir Urusniaga Jumlah Urusniaga Baki Penyataain balqisNo ratings yet

- IB - Course OutlineDocument4 pagesIB - Course OutlineChaitanya JethaniNo ratings yet

- Tev - Mrsia Final (Aleiah)Document20 pagesTev - Mrsia Final (Aleiah)Aleiah Jean LibatiqueNo ratings yet

- SY B.Com (Hons) C - Group 5Document27 pagesSY B.Com (Hons) C - Group 5Riya GuptaNo ratings yet

- BDODocument2 pagesBDOBevegel Sasan LlidoNo ratings yet

- Nanyang Business School AB1201 Financial Management Tutorial 2: Time Value of Money (Common Questions)Document7 pagesNanyang Business School AB1201 Financial Management Tutorial 2: Time Value of Money (Common Questions)asdsadsaNo ratings yet

- Unique Consultancy and Training Center Solution Mannual 2023Document25 pagesUnique Consultancy and Training Center Solution Mannual 2023Firdows SuleymanNo ratings yet