You might also like

- Age of Enlightenment (ID#32377)Document6 pagesAge of Enlightenment (ID#32377)saif khanNo ratings yet

- Unit 6 Accounting For LeasesDocument14 pagesUnit 6 Accounting For LeasesZebedee Taltal100% (1)

- Internal Control - Hayes - Chapter 6Document44 pagesInternal Control - Hayes - Chapter 6saif khanNo ratings yet

- Internal Control - Hayes - Chapter 6Document44 pagesInternal Control - Hayes - Chapter 6saif khanNo ratings yet

- Rehmanwaheed 3180 17836 2 12. Diminishing MusharakahDocument19 pagesRehmanwaheed 3180 17836 2 12. Diminishing MusharakahSadia AbidNo ratings yet

- Diminishing Musharakah Concept for Asset FinancingDocument26 pagesDiminishing Musharakah Concept for Asset FinancingHasan Irfan SiddiquiNo ratings yet

- IHF 18 19 Feb MUL 2013Document44 pagesIHF 18 19 Feb MUL 2013Habib Sultan KhelNo ratings yet

- Islamic Housing FinanceDocument26 pagesIslamic Housing FinanceAbdelnasir HaiderNo ratings yet

- DIMINISHING-MUSHARIKA-14112021-072718pmDocument24 pagesDIMINISHING-MUSHARIKA-14112021-072718pmAwn AqdasNo ratings yet

- AmBankIslamicAmMoneyLine iPDSDocument10 pagesAmBankIslamicAmMoneyLine iPDSMohd Naim Bin KaramaNo ratings yet

- Diminishing Musharakah Presentation 02-06-08Document32 pagesDiminishing Musharakah Presentation 02-06-08AlHuda Centre of Islamic Banking & Economics (CIBE)No ratings yet

- Bank Al Habib Car FinanceDocument9 pagesBank Al Habib Car Financefatima rahimNo ratings yet

- Diminishing Musharakah ExplainedDocument32 pagesDiminishing Musharakah ExplainedAli KhanNo ratings yet

- Diminishing Musharakah - MBL - PpsDocument17 pagesDiminishing Musharakah - MBL - Ppsgul_e_sabaNo ratings yet

- Meezan Bank PresentationDocument17 pagesMeezan Bank PresentationHussnain RazaNo ratings yet

- Diminishing Musharakah MBLDocument17 pagesDiminishing Musharakah MBLUbaid ArifNo ratings yet

- Islamic Modes of FinancingDocument17 pagesIslamic Modes of FinancingALI SHER HaidriNo ratings yet

- SME-Bank-PDS_MYS3_ENG_240616Document4 pagesSME-Bank-PDS_MYS3_ENG_240616Yowan SolomunNo ratings yet

- ISBF NotesDocument13 pagesISBF Notesmuneebmateen01No ratings yet

- Diminishing Musharakah MBLDocument17 pagesDiminishing Musharakah MBLAATIF IMTIAZNo ratings yet

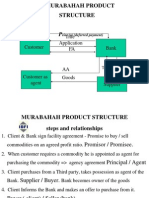

- MURABAHAH PRODUCT TITLEDocument26 pagesMURABAHAH PRODUCT TITLEUmair UddinNo ratings yet

- Arman EIF ASSignment 2Document5 pagesArman EIF ASSignment 2rafeeqNo ratings yet

- Mvtfi PdsDocument9 pagesMvtfi PdsRoselind NadieraNo ratings yet

- Affin Bank V Zulkifli Abdullah (Brief Case - Syazwani)Document5 pagesAffin Bank V Zulkifli Abdullah (Brief Case - Syazwani)Syaz SenoritasNo ratings yet

- Chapter 7 Short Term FinancingDocument41 pagesChapter 7 Short Term Financingzatty kimNo ratings yet

- 1. (a) Finance leases (b) Operating leases2. CorrectDocument22 pages1. (a) Finance leases (b) Operating leases2. CorrectEjaz AhmadNo ratings yet

- Name: Hunaid Ahmed. I.D: 9261. Course: Ibf.: Answer 1Document6 pagesName: Hunaid Ahmed. I.D: 9261. Course: Ibf.: Answer 1HUMNA AFTAB SHAHNo ratings yet

- (Lecture 5) - Other Investment Appraisal DecisionsDocument21 pages(Lecture 5) - Other Investment Appraisal DecisionsAjay Kumar Takiar100% (1)

- Ing Musharakah by Muhammad Shaheed KhanDocument20 pagesIng Musharakah by Muhammad Shaheed KhanShammo SagaNo ratings yet

- DM - Diminishing Musharakah Application & Documentation GuideDocument4 pagesDM - Diminishing Musharakah Application & Documentation GuideSyed Muhammad Hasan BilalNo ratings yet

- Hire PurchaseDocument49 pagesHire PurchasePriya SinghNo ratings yet

- Islamic Finance MCQ QuestionsDocument3 pagesIslamic Finance MCQ QuestionsYasmin Zainuddin100% (1)

- L2 Source of FinanceDocument26 pagesL2 Source of FinanceZhiyu KamNo ratings yet

- Finama LeasingDocument34 pagesFinama LeasingLoren Rosaria100% (1)

- Diminishing Musharakah: Center of Islamic FinanceDocument17 pagesDiminishing Musharakah: Center of Islamic Financeshahidkhan53No ratings yet

- Leasing As A Source of Finance: Fin501 Financial ManagementDocument23 pagesLeasing As A Source of Finance: Fin501 Financial ManagementDevyansh GuptaNo ratings yet

- Leasing As A Source of Finance: Fin501 Financial ManagementDocument23 pagesLeasing As A Source of Finance: Fin501 Financial ManagementDevyansh GuptaNo ratings yet

- AFFIN Home Invest-i Product Disclosure SheetDocument8 pagesAFFIN Home Invest-i Product Disclosure SheetMrHohoho97No ratings yet

- SME Bank High Tech and Green FacilityDocument4 pagesSME Bank High Tech and Green FacilitysuncroxsolarNo ratings yet

- Slide Lease 3Document33 pagesSlide Lease 3Rafia TasnimNo ratings yet

- Musharka Financing AgreementDocument12 pagesMusharka Financing AgreementHajra Aslam AfridiNo ratings yet

- Corporate Finance Ii2008 PDFDocument85 pagesCorporate Finance Ii2008 PDFTrymore KateeraNo ratings yet

- HASPACC 425 - Lease or Buy - HandoutDocument3 pagesHASPACC 425 - Lease or Buy - HandoutTawanda Tatenda HerbertNo ratings yet

- Sesssion 10 21-Nov-2020Document22 pagesSesssion 10 21-Nov-2020Uzma UzmaNo ratings yet

- Sesssion 10 21-Nov-2020Document22 pagesSesssion 10 21-Nov-2020Nasreen FawadNo ratings yet

- MFRS123Document23 pagesMFRS123Kelvin Leong100% (1)

- CH 3Document47 pagesCH 3Sarose ThapaNo ratings yet

- Sources of FinanceDocument10 pagesSources of FinanceOmer UddinNo ratings yet

- Cancellable SwapDocument1 pageCancellable SwapdltanevNo ratings yet

- Crédit À La ConsoDocument23 pagesCrédit À La ConsoNhật Minh Nguyễn ĐặngNo ratings yet

- Diminishing Musharaka IjarahBasedDocument22 pagesDiminishing Musharaka IjarahBasedArsalan AqeeqNo ratings yet

- Islamic FinanceDocument5 pagesIslamic Financeahsand123No ratings yet

- Assignment On Diminishing Musharakah by Malik SaeedDocument3 pagesAssignment On Diminishing Musharakah by Malik SaeedIbne- -AadamNo ratings yet

- IjaraDocument26 pagesIjaraNehal BadawyNo ratings yet

- Warrants & ConvertiblesDocument21 pagesWarrants & ConvertiblesSonika SoniNo ratings yet

- Application of Islamic FinancingDocument94 pagesApplication of Islamic Financingamirol93No ratings yet

- CH Hamad Rasool BhullarDocument12 pagesCH Hamad Rasool BhullarAlHuda Centre of Islamic Banking & Economics (CIBE)No ratings yet

- Islamic Financial Accounting IJARAH by MEZAAN BANKDocument24 pagesIslamic Financial Accounting IJARAH by MEZAAN BANKMBA...KID100% (1)

- Chapter - 10 Lease and Term LoansDocument15 pagesChapter - 10 Lease and Term LoansNabila EramNo ratings yet

- The Saint Augustine University of Tanzania: QuestionsDocument7 pagesThe Saint Augustine University of Tanzania: QuestionsIssa AdiemaNo ratings yet

- Chap 9Document22 pagesChap 9charlie simoNo ratings yet

- The Art of Persuasion: Cold Calling Home Sellers for Owner Financing OpportunitiesFrom EverandThe Art of Persuasion: Cold Calling Home Sellers for Owner Financing OpportunitiesNo ratings yet

- The Business, Tax, and Financial EnvironmentsDocument44 pagesThe Business, Tax, and Financial EnvironmentsAAM26No ratings yet

- Financial Risk ManagementDocument38 pagesFinancial Risk Managementsaif khanNo ratings yet

- Risk ManagementDocument40 pagesRisk Managementsaif khanNo ratings yet

- CSR and CGDocument18 pagesCSR and CGsaif khanNo ratings yet

- Introduction To RiskDocument38 pagesIntroduction To Risksaif khanNo ratings yet

- Industry AnalysisDocument49 pagesIndustry Analysissaif khanNo ratings yet

- Introduction To Business FinanceDocument86 pagesIntroduction To Business FinanceYahya KhanNo ratings yet

- The Valuation of Long-Term Securities: Instructor: Ajab Khan BurkiDocument82 pagesThe Valuation of Long-Term Securities: Instructor: Ajab Khan BurkiGaurav KarkiNo ratings yet

- CH 01Document20 pagesCH 01saif khanNo ratings yet

- Name: Saif Ur Rehman ID# 32280 Program: BS A&F Assignment No.02Document1 pageName: Saif Ur Rehman ID# 32280 Program: BS A&F Assignment No.02saif khanNo ratings yet

- Financial Markets and Institutions: Abridged 11 EditionDocument38 pagesFinancial Markets and Institutions: Abridged 11 Editionsaif khanNo ratings yet

- Assignment 1: (Also Cover This Scheme From Pakistan) 6. (Mention Any Three Plus One From Pakistan)Document1 pageAssignment 1: (Also Cover This Scheme From Pakistan) 6. (Mention Any Three Plus One From Pakistan)saif khanNo ratings yet

- Saif Ur Rehman Week 3 SmimDocument3 pagesSaif Ur Rehman Week 3 Smimsaif khanNo ratings yet

- World War 1Document41 pagesWorld War 1saif khanNo ratings yet

- Saif Ur Rehman Week 3 SmimDocument3 pagesSaif Ur Rehman Week 3 Smimsaif khanNo ratings yet

- SDG 9 Group PresentationDocument15 pagesSDG 9 Group Presentationsaif khanNo ratings yet

- World History Assignment 32280Document7 pagesWorld History Assignment 32280saif khanNo ratings yet

- Syed Hassan Zar Naqvi (32323) SMIMDocument2 pagesSyed Hassan Zar Naqvi (32323) SMIMsaif khanNo ratings yet

- Name: Saif Ur Rehman ID# 32280 Program: BS A&F Assignment No.02Document1 pageName: Saif Ur Rehman ID# 32280 Program: BS A&F Assignment No.02saif khanNo ratings yet

- Name: Saif Ur Rehman ID# 32280 Program: BS A&F Assignment No.02Document1 pageName: Saif Ur Rehman ID# 32280 Program: BS A&F Assignment No.02saif khanNo ratings yet

- Presentation World HistoryDocument13 pagesPresentation World Historysaif khanNo ratings yet

- Topic No.14-Ambiguity and VaguenessDocument20 pagesTopic No.14-Ambiguity and Vaguenesssaif khanNo ratings yet

- Name: Saif Ur Rehman ID# 32280 Program: BS A&F Assignment No.02Document1 pageName: Saif Ur Rehman ID# 32280 Program: BS A&F Assignment No.02saif khanNo ratings yet

- Attitude and Self ConceptDocument11 pagesAttitude and Self Conceptsaif khanNo ratings yet

- Isl. Lecture#9 Compilation in The Time of Hazrat Usman (R.a.) - 1Document10 pagesIsl. Lecture#9 Compilation in The Time of Hazrat Usman (R.a.) - 1saif khanNo ratings yet

- Faith in God'S ProphetsDocument14 pagesFaith in God'S Prophetssaif khanNo ratings yet

- Chap 3 Development Process REM315Document78 pagesChap 3 Development Process REM315Shaleea ShaNo ratings yet

- Unit 2 Objectives VipulDocument7 pagesUnit 2 Objectives Vipulamrutapillai06No ratings yet

- Sample of Doctoral Thesis On Corporate Governance and Financial PerformanceDocument5 pagesSample of Doctoral Thesis On Corporate Governance and Financial Performancexgkeiiygg100% (2)

- KKCL - Investor Presentation Q2 & H1FY24Document45 pagesKKCL - Investor Presentation Q2 & H1FY24Variable SeperableNo ratings yet

- Dark Green Light Green White Corporate Geometric Company Internal Deck Business PresentationDocument14 pagesDark Green Light Green White Corporate Geometric Company Internal Deck Business PresentationHarkrishan SinghNo ratings yet

- Supermarket Kelompok 5Document6 pagesSupermarket Kelompok 5adriana kuswaraNo ratings yet

- Basel AccordDocument12 pagesBasel AccordRimissha Udenia 2No ratings yet

- URA FactsheetDocument2 pagesURA FactsheetAlex MilarNo ratings yet

- Rocket Brand SolutionsDocument17 pagesRocket Brand SolutionsSujeet PathareNo ratings yet

- International Finance Global 6th Edition Eun Test BankDocument71 pagesInternational Finance Global 6th Edition Eun Test Bankjethrodavide6qi100% (31)

- Porter's Competitive Forces Model Information SystemDocument13 pagesPorter's Competitive Forces Model Information SystemhimanshuNo ratings yet

- ADOBE - Compensation Breakup - Member of Technical StaffDocument2 pagesADOBE - Compensation Breakup - Member of Technical Staffdehejar970No ratings yet

- PB BrE B1+ WB Answers U5 PDFDocument1 pagePB BrE B1+ WB Answers U5 PDFDaniel CostaNo ratings yet

- Nursyafiqa Syafira Binti Maheran (2082018070009)Document3 pagesNursyafiqa Syafira Binti Maheran (2082018070009)Syafiqa SyafiraNo ratings yet

- Krish Mar23Document4 pagesKrish Mar23Gengaraj PothirajNo ratings yet

- Bản inDocument23 pagesBản inTrang VũNo ratings yet

- Christy Apparels-RA-10-03-2023Document10 pagesChristy Apparels-RA-10-03-2023Karthikeyan RK SwamyNo ratings yet

- Movie Theater Business PlanDocument21 pagesMovie Theater Business PlanShifna MohamedNo ratings yet

- ENG Creed Company Profile 2023Document20 pagesENG Creed Company Profile 2023herifikrioNo ratings yet

- Thesis On Regional Rural Banks in IndiaDocument8 pagesThesis On Regional Rural Banks in Indiafj9dbfw4100% (2)

- You Exec - Project Dashboards Collection CompleteDocument25 pagesYou Exec - Project Dashboards Collection CompleteJohn DulayNo ratings yet

- Integer Programming QuestionsDocument15 pagesInteger Programming QuestionsAishwarya SrivastavaNo ratings yet

- CF2 - Chapter 2 Capital Structure - SVDocument45 pagesCF2 - Chapter 2 Capital Structure - SVleducNo ratings yet

- Urdu Essay WritingDocument9 pagesUrdu Essay Writingb6yf8tcd100% (2)

- Managerial Economic-QuizDocument5 pagesManagerial Economic-QuizPrincessNo ratings yet

- Pay Durham College Fees Before October 20Document2 pagesPay Durham College Fees Before October 20hkc123No ratings yet

- Liberalisation Privatisation and GlobalisationDocument13 pagesLiberalisation Privatisation and Globalisationakp200522No ratings yet

- Ebe1516 01Document13 pagesEbe1516 01Rajendra Gibran Alvaro RamadhanNo ratings yet

- Innovative Financial Services QBDocument32 pagesInnovative Financial Services QBLeo Bogosi MotlogelwNo ratings yet

- SHARES, DIVIDENDS, AND PERFORMANCE OF HM SAMPOERNA INDONESIA TBKDocument13 pagesSHARES, DIVIDENDS, AND PERFORMANCE OF HM SAMPOERNA INDONESIA TBKfahrulhidayatNo ratings yet