You might also like

- Dividend Investing for Beginners & DummiesFrom EverandDividend Investing for Beginners & DummiesRating: 5 out of 5 stars5/5 (1)

- Far410 Chapter 4 Equity 2014Document32 pagesFar410 Chapter 4 Equity 2014mr.nazir.shahidanNo ratings yet

- Chapter 8 OSC PSC, Loan Capital and Bond ValuationDocument34 pagesChapter 8 OSC PSC, Loan Capital and Bond Valuationathirah jamaludinNo ratings yet

- Homework Questions For Tutorial in Week 7 With SolutionDocument12 pagesHomework Questions For Tutorial in Week 7 With SolutionrickNo ratings yet

- Far410 Chapter 4 EquityDocument34 pagesFar410 Chapter 4 EquityAQILAH NORDINNo ratings yet

- Module 4-CoC-1Document13 pagesModule 4-CoC-1Abida RiazNo ratings yet

- Chapter 3 Stock ValuationDocument51 pagesChapter 3 Stock ValuationJon Loh Soon Weng50% (2)

- Financing Decision: Dr. Md. Rezaul KabirDocument129 pagesFinancing Decision: Dr. Md. Rezaul KabirUrbana Raquib Rodosee100% (1)

- Dividend Decisions-1Document24 pagesDividend Decisions-1TIBUGWISHA IVANNo ratings yet

- 1 What Are Corporate Actions?: CreditorsDocument14 pages1 What Are Corporate Actions?: CreditorsBadal ShahNo ratings yet

- Study Guide - Chapter 3 - Issuance of Shares and Loan CapitalDocument23 pagesStudy Guide - Chapter 3 - Issuance of Shares and Loan CapitalHappy PillsNo ratings yet

- Share Capital and Basic Legal Documents of A CompanyDocument62 pagesShare Capital and Basic Legal Documents of A CompanyMuneebNo ratings yet

- Dividends and Share Repurchases: Basics: Presenter's Name Presenter's Title DD Month YyyyDocument20 pagesDividends and Share Repurchases: Basics: Presenter's Name Presenter's Title DD Month YyyyKavin Ur FrndNo ratings yet

- Long-Term Funds:: Sources and CostsDocument23 pagesLong-Term Funds:: Sources and CostsArmilyn Jean Castones0% (1)

- Far 410: Chapter 4: EquityDocument44 pagesFar 410: Chapter 4: EquityJung KookieNo ratings yet

- Mod 5 Dividend Decisions Handout SNDocument7 pagesMod 5 Dividend Decisions Handout SNAkhilNo ratings yet

- Corporate Finance Chapter6Document20 pagesCorporate Finance Chapter6Dan688No ratings yet

- Corporate Accounting 1: III Semester BBADocument57 pagesCorporate Accounting 1: III Semester BBAAR Ananth Rohith BhatNo ratings yet

- Dividend PolicyDocument52 pagesDividend PolicyANISH KUMARNo ratings yet

- ACCOUNTING FOR CORPORATIONS-Share CapitalDocument57 pagesACCOUNTING FOR CORPORATIONS-Share CapitalMarriel Fate Cullano75% (8)

- Financial ManagementDocument22 pagesFinancial Managementutkrsh raghavNo ratings yet

- Dividend Decisions: Dividend: Cash Distribution of Earnings Among ShareholdersDocument33 pagesDividend Decisions: Dividend: Cash Distribution of Earnings Among ShareholdersKritika BhattNo ratings yet

- UntitledDocument25 pagesUntitledEhab M. Abdel HadyNo ratings yet

- Redemption of Preference SharesDocument34 pagesRedemption of Preference SharesManasNo ratings yet

- Issue of Right Share and Bonus ShareDocument15 pagesIssue of Right Share and Bonus ShareRahulNo ratings yet

- Session 1-3 - Dividend PolicyDocument47 pagesSession 1-3 - Dividend PolicyHaardik GandhiNo ratings yet

- On Sore InstrumentsDocument19 pagesOn Sore InstrumentsPrashant GharatNo ratings yet

- Share: by Aju K Raju Mba Ii MiimDocument13 pagesShare: by Aju K Raju Mba Ii MiimAju K Raju100% (1)

- Share Capital, Share and MembershipDocument17 pagesShare Capital, Share and Membershipakashkr619No ratings yet

- Corporations: Organization and Capital Stock Transactions: Weygandt - Kieso - KimmelDocument54 pagesCorporations: Organization and Capital Stock Transactions: Weygandt - Kieso - Kimmelkey aidanNo ratings yet

- RM Assignment-3: Q1. Dividend Policy Can Be Used To Maximize The Wealth of The Shareholder. Explain. AnswerDocument4 pagesRM Assignment-3: Q1. Dividend Policy Can Be Used To Maximize The Wealth of The Shareholder. Explain. AnswerSiddhant gudwaniNo ratings yet

- Introduction To Issue Forfeiture and Reissue of SharesDocument37 pagesIntroduction To Issue Forfeiture and Reissue of SharesRkenterpriseNo ratings yet

- My PartDocument6 pagesMy Partkdoshi23No ratings yet

- Dividend Decisions: Amity School of BusinessDocument33 pagesDividend Decisions: Amity School of BusinessGurshaan SarlaNo ratings yet

- Chapter 2 - Part 4 - Shares & Loan CapitalDocument24 pagesChapter 2 - Part 4 - Shares & Loan Capital2022885126No ratings yet

- Capital and Its Types: Name: Saroop Cms:42529 Section: B Semester: 6 Assignment:2Document9 pagesCapital and Its Types: Name: Saroop Cms:42529 Section: B Semester: 6 Assignment:2Sanjna ChimnaniNo ratings yet

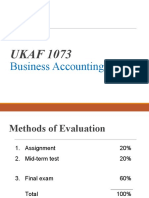

- UKAF 1073: Business Accounting IIDocument61 pagesUKAF 1073: Business Accounting IIalibabaNo ratings yet

- Financial Accounting - Information For Decisions - Session 8 - Chapter 10 PPT Eh5CoID6zuDocument38 pagesFinancial Accounting - Information For Decisions - Session 8 - Chapter 10 PPT Eh5CoID6zumukul3087_305865623No ratings yet

- Share and Share CapitalDocument16 pagesShare and Share CapitalChicIshuNo ratings yet

- Limited CompaniesDocument4 pagesLimited CompaniesSukhmani KaurNo ratings yet

- UNIT 4: Company Accounts-Share CapitalDocument13 pagesUNIT 4: Company Accounts-Share CapitalpraveentyagiNo ratings yet

- Dividends and Share Repurchases: Basics: Presenter's Name Presenter's Title DD Month YyyyDocument20 pagesDividends and Share Repurchases: Basics: Presenter's Name Presenter's Title DD Month YyyyPRAKNo ratings yet

- Chapter 13 SolutionsDocument45 pagesChapter 13 Solutionsaboodyuae2000No ratings yet

- Business Finance: Sources of Long-Term FinanceDocument33 pagesBusiness Finance: Sources of Long-Term FinanceHibaaq AxmedNo ratings yet

- Solution Manual For Core Concepts of Accounting Raiborn 2nd EditionDocument18 pagesSolution Manual For Core Concepts of Accounting Raiborn 2nd EditionJacquelineFrancisfpgs100% (36)

- Long-Term Funds Sourcing: Equity Financing: Mary Chienny Anne HocosolDocument19 pagesLong-Term Funds Sourcing: Equity Financing: Mary Chienny Anne HocosolChienny HocosolNo ratings yet

- Share Capital: Urmila ItamDocument33 pagesShare Capital: Urmila ItamUrmila JagadeeswariNo ratings yet

- 4.financing & Dividend PoliciesDocument11 pages4.financing & Dividend PoliciesSuja mkNo ratings yet

- Lesson 3Document14 pagesLesson 3Absalom OtienoNo ratings yet

- Audio Chapter 12 - Companies PART CDocument13 pagesAudio Chapter 12 - Companies PART CprunellaNo ratings yet

- Equity Securities MarketDocument23 pagesEquity Securities MarketILOVE MATURED FANSNo ratings yet

- Capital Maintenance NotesDocument4 pagesCapital Maintenance NotesFrancis Njihia KaburuNo ratings yet

- Financial Accounting A Business Process Approach 3Rd Edition Reimers Solutions Manual Full Chapter PDFDocument67 pagesFinancial Accounting A Business Process Approach 3Rd Edition Reimers Solutions Manual Full Chapter PDFKristieKelleyenfm100% (11)

- CH 07Document23 pagesCH 07mehdiNo ratings yet

- VC - Finm7312 Slides # 3Document24 pagesVC - Finm7312 Slides # 3Phumzile MahlanguNo ratings yet

- Buy Back of SharesDocument39 pagesBuy Back of SharesApurv SrivastavNo ratings yet

- Dividend Policy 1Document56 pagesDividend Policy 1hardika jadavNo ratings yet

- Fa Unit 4Document13 pagesFa Unit 4VTNo ratings yet

- Financial ManagementDocument7 pagesFinancial ManagementShibu ShashankNo ratings yet

- Sebi TocDocument33 pagesSebi Tocapi-3712367No ratings yet

- Gibson 11e Ch08Document24 pagesGibson 11e Ch08Keval KamaniNo ratings yet

- BFM Course Syllabus 1Document8 pagesBFM Course Syllabus 1Nainisha Sawant0% (1)

- FOREX TRADING MANUAL Beginners To AdvanceDocument65 pagesFOREX TRADING MANUAL Beginners To AdvanceHenryMM75% (4)

- CH 06Document34 pagesCH 06Puput AjaNo ratings yet

- SAR CalculatorDocument8 pagesSAR CalculatorPraveen PrasadNo ratings yet

- How To Invest $50,000 - Louis Navellier's Emerging GrowthDocument2 pagesHow To Invest $50,000 - Louis Navellier's Emerging Growthsan MunNo ratings yet

- DB Realty - Bamboo Hotels - Marine Drive Hospitality & Realty - Prestige GroupDocument3 pagesDB Realty - Bamboo Hotels - Marine Drive Hospitality & Realty - Prestige Grouptowaf57520No ratings yet

- Derivations and Applications of Greek LettersDocument30 pagesDerivations and Applications of Greek Letters段鑫No ratings yet

- MCQ QuizDocument13 pagesMCQ QuizSharNo ratings yet

- Maybank - Aviation Report On CaamDocument7 pagesMaybank - Aviation Report On CaamNinerMike MysNo ratings yet

- Commercial Bank Financial Management in The Financial Services Industry PDFDocument2 pagesCommercial Bank Financial Management in The Financial Services Industry PDFPrince0% (1)

- eFM2e, CH 10, SlidesDocument32 pageseFM2e, CH 10, SlidesDanica BeleyNo ratings yet

- RẤT HAY Top 5 Advanced Forex Trading Strategies in 2020Document10 pagesRẤT HAY Top 5 Advanced Forex Trading Strategies in 2020Elap ElapNo ratings yet

- LS - Real Estate and Portfolio TheoryDocument31 pagesLS - Real Estate and Portfolio TheoryTanmoy ChakrabortyNo ratings yet

- Chapter7-Stock Price Behavior & Market EfficiencyDocument9 pagesChapter7-Stock Price Behavior & Market Efficiencytconn8276No ratings yet

- HDFC Life Insurance (HDFCLIFE) : 2. P/E 58 3. Book Value (RS) 23.57Document5 pagesHDFC Life Insurance (HDFCLIFE) : 2. P/E 58 3. Book Value (RS) 23.57Srini VasanNo ratings yet

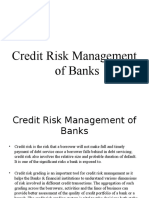

- Credit Risk Mangament of Commercial Bank.Document5 pagesCredit Risk Mangament of Commercial Bank.Sibiya Zaman AdibaNo ratings yet

- Cover Sheet: COL Financial Group, IncDocument3 pagesCover Sheet: COL Financial Group, IncIrene SalvadorNo ratings yet

- SWIFT Message Type Reference: Category 1 MessagesDocument13 pagesSWIFT Message Type Reference: Category 1 Messagessamba_luckyNo ratings yet

- Pugachevsky - Bond To CDS SpreadsDocument3 pagesPugachevsky - Bond To CDS SpreadsZerohedge100% (6)

- Ismr Full2019Document206 pagesIsmr Full2019akpo-ebi johnNo ratings yet

- Gbpaud m5 OLDocument3 pagesGbpaud m5 OLArifNo ratings yet

- Topic 4 Lecture NotesDocument13 pagesTopic 4 Lecture Notesdara ofulueNo ratings yet

- Siegel ParadoxDocument4 pagesSiegel ParadoxbobmezzNo ratings yet

- FUNDAMENTAL of ManagementDocument100 pagesFUNDAMENTAL of ManagementEralisa Paden100% (1)

- Balance Sheet - Britannia IndustriesDocument2 pagesBalance Sheet - Britannia IndustriesAnuj SachdevNo ratings yet

- The Business, Tax, and Financial EnvironmentsDocument38 pagesThe Business, Tax, and Financial EnvironmentsNaveed AhmadNo ratings yet

- CH 77Document50 pagesCH 77saraNo ratings yet