You might also like

- Risk Management Handbook (2024): FAA-H-8083-2AFrom EverandRisk Management Handbook (2024): FAA-H-8083-2ANo ratings yet

- Assignment Mpu3223 v2Document14 pagesAssignment Mpu3223 v2MOHAMAD HAMIZI BIN MAHMOOD STUDENTNo ratings yet

- MKT761 Article ReviewDocument8 pagesMKT761 Article ReviewAlea AzmiNo ratings yet

- Reasons of PIA's Decline Into Near BankruptcyDocument9 pagesReasons of PIA's Decline Into Near BankruptcyQuratulain HanifNo ratings yet

- LT50 2022 WebDocument28 pagesLT50 2022 WebasdrubalmartinsNo ratings yet

- PDSCM Om101-Ad-11538 s1 Assignment 1Document6 pagesPDSCM Om101-Ad-11538 s1 Assignment 1Mdue MafuNo ratings yet

- 5 Worst Airlines in The World: Submitted By: Marva AftabDocument3 pages5 Worst Airlines in The World: Submitted By: Marva AftabNabigha FaheemNo ratings yet

- Aircraft Records Technician Assignment 1Document16 pagesAircraft Records Technician Assignment 1Mohamad Hazwan Mohamad JanaiNo ratings yet

- Malaysia Airlines SWOT AnalysisDocument3 pagesMalaysia Airlines SWOT AnalysisMarzan Bin Azad50% (2)

- Financial ManagementDocument33 pagesFinancial Managementhaidil abd hamidNo ratings yet

- Marketing Audit - FinalDocument27 pagesMarketing Audit - FinalFaisal NizamNo ratings yet

- MPIS7103 - Assignment 1 (201905)Document38 pagesMPIS7103 - Assignment 1 (201905)Kamalnathan ElangobanNo ratings yet

- Strat Plan For CIACDocument18 pagesStrat Plan For CIACJonathan DavidNo ratings yet

- Aviation Shutdown Impacts LTR FINAL 01.10.19Document3 pagesAviation Shutdown Impacts LTR FINAL 01.10.19Benjamin ZhangNo ratings yet

- Problems of Pia and Solution Strategies PDF FreeDocument27 pagesProblems of Pia and Solution Strategies PDF FreeSaim IrfanNo ratings yet

- Literature Review On Aviation IndustryDocument5 pagesLiterature Review On Aviation Industrygvxphmm8100% (1)

- Malaysia AirlinesDocument14 pagesMalaysia Airlinesa_wyneNo ratings yet

- Synopsis - Directorate of Air Safety and Investigation of Aviation Accidents Role and ImpactDocument3 pagesSynopsis - Directorate of Air Safety and Investigation of Aviation Accidents Role and ImpactRahul BectorNo ratings yet

- Heathrow Terminal 5: The Making of A World Class Service CaseDocument4 pagesHeathrow Terminal 5: The Making of A World Class Service CaseS.M. Jakaria AbirNo ratings yet

- RASG-AFI.8 - WP05 - Common Challenges en - RevDocument3 pagesRASG-AFI.8 - WP05 - Common Challenges en - RevDaniel Dos SantosNo ratings yet

- AC 121-32A Dispatch Resource Management TrainingDocument14 pagesAC 121-32A Dispatch Resource Management Trainingbfibingier0% (1)

- Msia Aviation SU 050413 2045Document21 pagesMsia Aviation SU 050413 2045JcoveNo ratings yet

- SWOT AnalysisDocument12 pagesSWOT AnalysiswilliamjoneNo ratings yet

- Emirates Airline: SMM219 The Organisation in Its EnvironmentDocument10 pagesEmirates Airline: SMM219 The Organisation in Its EnvironmentDenver Rosario67% (3)

- Air Asia CompleteDocument18 pagesAir Asia CompleteAmy CharmaineNo ratings yet

- DocxDocument9 pagesDocx'Zhi En WongNo ratings yet

- Potential Safety Risk of Interference To Aircraft Altimeter by 5G Telecommunications SystemDocument3 pagesPotential Safety Risk of Interference To Aircraft Altimeter by 5G Telecommunications SystemAfdhalNo ratings yet

- Sanya Shoaib TP048114: Individual AssignmentDocument12 pagesSanya Shoaib TP048114: Individual AssignmentGurung AnshuNo ratings yet

- Case Analysis AirAsia Group 8Document23 pagesCase Analysis AirAsia Group 8Czarina Faye CamalesNo ratings yet

- CAPA India COVID Update 4Document16 pagesCAPA India COVID Update 4Yadukul BhuvanendranNo ratings yet

- Air BlueDocument6 pagesAir BlueFarid Nawaz KhanNo ratings yet

- Nap 2019Document98 pagesNap 2019Adeel AfzalNo ratings yet

- Internal Environment of MASDocument5 pagesInternal Environment of MASKah ChunNo ratings yet

- Literature ReviewDocument21 pagesLiterature ReviewXeeshan Shah100% (1)

- OW Airline Economics 08Document8 pagesOW Airline Economics 08felizjulianidadNo ratings yet

- Strategic Management Report: Student Id: 21420599 Submitted To: MS. Sneha ThakkarDocument13 pagesStrategic Management Report: Student Id: 21420599 Submitted To: MS. Sneha ThakkarRohan KurupNo ratings yet

- Manual References FLTDocument236 pagesManual References FLTKola IludiranNo ratings yet

- Dispatch Resource Management Training: Subject: Date: 11/21/05 Initiated By: AFS-220 AC No: 121-32A ChangeDocument15 pagesDispatch Resource Management Training: Subject: Date: 11/21/05 Initiated By: AFS-220 AC No: 121-32A ChangeZawNo ratings yet

- Advanced Strategic Management Yr 3 Assignment Strategic Options For Malaysia Airlines To Enhance Its Growth S PDFDocument51 pagesAdvanced Strategic Management Yr 3 Assignment Strategic Options For Malaysia Airlines To Enhance Its Growth S PDFBin HassanNo ratings yet

- Problems of PIA and Solution + StrategiesDocument27 pagesProblems of PIA and Solution + StrategiesAreeba Imtiaz HUssain50% (4)

- Sustainability of Airlines in India With Covid19 Challenges Ahead and Possible Wayouts2020journal of Revenue and Pricing ManagementDocument16 pagesSustainability of Airlines in India With Covid19 Challenges Ahead and Possible Wayouts2020journal of Revenue and Pricing ManagementashishNo ratings yet

- Research ProposalDocument10 pagesResearch ProposalHafiz Abid HameedNo ratings yet

- Research Paper On Airline IndustryDocument6 pagesResearch Paper On Airline Industryhyxjmyhkf100% (1)

- Key Lessons From The Boeing 737 MAX 8 AccidentsDocument3 pagesKey Lessons From The Boeing 737 MAX 8 AccidentsRenita MrcllaNo ratings yet

- Module Title: Aerodrome Certification/Registration Name: Hanna F. Porras Date: Nov. 30, 2020 Page 1 of 2 Grade: Activity No. 3Document2 pagesModule Title: Aerodrome Certification/Registration Name: Hanna F. Porras Date: Nov. 30, 2020 Page 1 of 2 Grade: Activity No. 3Hanna PorrasNo ratings yet

- Strategic Audit Report by Inzamam EditedDocument21 pagesStrategic Audit Report by Inzamam EditedAhsan SomrooNo ratings yet

- Aerospace - Developing A Minimum Equipment ListDocument16 pagesAerospace - Developing A Minimum Equipment ListStephen EriakuNo ratings yet

- Faa Ac120-82Document78 pagesFaa Ac120-82voxoxoxNo ratings yet

- Airspace Management and Air Traffic ServicesDocument9 pagesAirspace Management and Air Traffic ServicesOm LalchandaniNo ratings yet

- Thesis Airline ManagementDocument8 pagesThesis Airline Managementpamelawilliamserie100% (2)

- HHRG 118 PW05 Wstate BlackDocument20 pagesHHRG 118 PW05 Wstate BlackJessica A. BotelhoNo ratings yet

- AC 61-134 Editorial UpdateDocument21 pagesAC 61-134 Editorial UpdateRaimundo MNo ratings yet

- Pia ReportDocument17 pagesPia ReportAltaf MagsiNo ratings yet

- Malindo AirDocument22 pagesMalindo AirKHAIRIL HAJAR BINTI AHMADNo ratings yet

- Aerospace: Unsupervised Anomaly Detection in Flight Data Using Convolutional Variational Auto-EncoderDocument19 pagesAerospace: Unsupervised Anomaly Detection in Flight Data Using Convolutional Variational Auto-EncoderRodolfo BetanzosNo ratings yet

- Malaysian Airline Systems (Mas) : Swot Analysis, Twos Analysis, Pest Analysis, Porter'S Five, BCG Matrix and Strategic MAPDocument11 pagesMalaysian Airline Systems (Mas) : Swot Analysis, Twos Analysis, Pest Analysis, Porter'S Five, BCG Matrix and Strategic MAPNoorAhmed100% (3)

- Air Blue ProjectDocument50 pagesAir Blue Projectsyed usman wazir92% (13)

- Executive Summary Navigating Safety Challenges at Company B and Its Impact On Acquisition DecisionsDocument9 pagesExecutive Summary Navigating Safety Challenges at Company B and Its Impact On Acquisition DecisionsNick RoyNo ratings yet

- MCTF FY2016 Report PublicDocument26 pagesMCTF FY2016 Report PublicfernandoNo ratings yet

- Registration Form ISAR 2023 LatestDocument2 pagesRegistration Form ISAR 2023 LatestNinerMike MysNo ratings yet

- Caam RM1000Document2 pagesCaam RM1000NinerMike MysNo ratings yet

- Aircraft Maintenance Engineers As Effective Project ManagersDocument12 pagesAircraft Maintenance Engineers As Effective Project ManagersNinerMike MysNo ratings yet

- 03.05.2022 LinkedIn ChecklistDocument4 pages03.05.2022 LinkedIn ChecklistNinerMike MysNo ratings yet

- Timeline Short Course (NDT)Document1 pageTimeline Short Course (NDT)NinerMike MysNo ratings yet

- SAS2022 BrochureDocument12 pagesSAS2022 BrochureNinerMike MysNo ratings yet

- 25 27 Nov 2021 SAS BrochureDocument16 pages25 27 Nov 2021 SAS BrochureNinerMike MysNo ratings yet

- OOHM - Malaysia's 1st Outdoor Integrated MediaDocument14 pagesOOHM - Malaysia's 1st Outdoor Integrated MediaNinerMike MysNo ratings yet

- Purple Yellow Blue Orange Broom CLeaning Lady Professional Home Cleaners Business Card PDFDocument1 pagePurple Yellow Blue Orange Broom CLeaning Lady Professional Home Cleaners Business Card PDFNinerMike MysNo ratings yet

- Daily Motivational Quotes Brought To You by TEBAB0 MALAYSIA: FB: @tebabomalaysiaDocument6 pagesDaily Motivational Quotes Brought To You by TEBAB0 MALAYSIA: FB: @tebabomalaysiaNinerMike MysNo ratings yet

- Kannad Aviation Install E-Prog and ManageYourBeaconDocument7 pagesKannad Aviation Install E-Prog and ManageYourBeaconNinerMike MysNo ratings yet

- Kannad Aviation Install E-Prog and ManageYourBeaconDocument7 pagesKannad Aviation Install E-Prog and ManageYourBeaconNinerMike MysNo ratings yet

- Y.S.P. Southeast Asia Holding Bhd. (Company No. 552781 X) Board CharterDocument11 pagesY.S.P. Southeast Asia Holding Bhd. (Company No. 552781 X) Board CharterNinerMike MysNo ratings yet

- Package Paymeent Method Reserve Your Seats Today!: Accelerating Growth and Cooperation For A Win-Win SituationDocument1 pagePackage Paymeent Method Reserve Your Seats Today!: Accelerating Growth and Cooperation For A Win-Win SituationNinerMike MysNo ratings yet

- Approvals and Standardisation Organisation Approvals Docs Good Practices EASA - S21 - GP001 - 1209Document26 pagesApprovals and Standardisation Organisation Approvals Docs Good Practices EASA - S21 - GP001 - 1209Azzeddine ZariouhNo ratings yet

- Aerospace Manufacturers Legal Dated 31.07.2019 PDFDocument33 pagesAerospace Manufacturers Legal Dated 31.07.2019 PDFNinerMike MysNo ratings yet

- ICAO 8 Critical ElementsDocument2 pagesICAO 8 Critical ElementsNinerMike MysNo ratings yet

- Top 100 Aerospace Companies by Revenue 2018 PDFDocument8 pagesTop 100 Aerospace Companies by Revenue 2018 PDFNinerMike MysNo ratings yet

- ICAO SMICG Document PDFDocument4 pagesICAO SMICG Document PDFNinerMike MysNo ratings yet

- Civil Aviation Authority of Malaysia Civil Aviation Notice (Can)Document7 pagesCivil Aviation Authority of Malaysia Civil Aviation Notice (Can)NinerMike MysNo ratings yet

- CNS AtmDocument10 pagesCNS Atmfuego00No ratings yet

- 2019 Aerospace Manufacturing Attractiveness RankingsDocument24 pages2019 Aerospace Manufacturing Attractiveness RankingsNinerMike MysNo ratings yet

- Malaysian Standard MS 1500 2019 PDFDocument24 pagesMalaysian Standard MS 1500 2019 PDFNinerMike Mys33% (3)

- SAVE THE DATE Sarajevo Halal Fair 2019 MailDocument2 pagesSAVE THE DATE Sarajevo Halal Fair 2019 MailNinerMike MysNo ratings yet

- Able Engineering B206-WebDocument2 pagesAble Engineering B206-WebNinerMike MysNo ratings yet

- FPP PartB Template PDFDocument16 pagesFPP PartB Template PDFAshish RoyNo ratings yet

- Benefits of Integrated TerminalsDocument10 pagesBenefits of Integrated TerminalsNinerMike MysNo ratings yet

- Technical Paper Air Services Agreement November 2018Document78 pagesTechnical Paper Air Services Agreement November 2018NinerMike MysNo ratings yet

- Mavcom Waypoint May 2019Document90 pagesMavcom Waypoint May 2019NinerMike MysNo ratings yet

- Position Paper On Sequencing Liberalization For The Malaysian Aviation Services SectorDocument76 pagesPosition Paper On Sequencing Liberalization For The Malaysian Aviation Services SectorNinerMike MysNo ratings yet

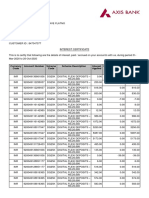

- Interest CertificateDocument2 pagesInterest CertificatesumitNo ratings yet

- A Guide To The Stock Exchange For Beginners - Part 2 PDFDocument5 pagesA Guide To The Stock Exchange For Beginners - Part 2 PDFAnil Yadavrao GaikwadNo ratings yet

- New Investment Supports SkySparc Growth StrategyDocument3 pagesNew Investment Supports SkySparc Growth StrategyPR.comNo ratings yet

- Kuwait Finance House AustDocument2 pagesKuwait Finance House AustchairunnisanovNo ratings yet

- Statement of AccountDocument7 pagesStatement of AccountHamza CollectionNo ratings yet

- Banking RatiosDocument7 pagesBanking Ratioszhalak04No ratings yet

- Module 2 Simple DiscountDocument13 pagesModule 2 Simple DiscountMhestica MiranoNo ratings yet

- Deposit, Mutuum, CommudatumDocument33 pagesDeposit, Mutuum, CommudatumkimuchosNo ratings yet

- Money: Money Is Any Item or Verifiable Record That Is Generally AcceptedDocument2 pagesMoney: Money Is Any Item or Verifiable Record That Is Generally AcceptedMokshi shahNo ratings yet

- Books of Accounts Double Entry System With Answers by AlagangwencyDocument4 pagesBooks of Accounts Double Entry System With Answers by AlagangwencyHello KittyNo ratings yet

- Sample Questions - Mini-Test 1Document4 pagesSample Questions - Mini-Test 1sam heisenbergNo ratings yet

- Us Engineering Construction Ma Due DiligenceDocument52 pagesUs Engineering Construction Ma Due DiligenceOsman Murat TütüncüNo ratings yet

- Ap COSTSDocument4 pagesAp COSTSferNo ratings yet

- Pamantasan NG Cabuyao: Katapatan Subd., Banay Banay, City of CabuyaoDocument5 pagesPamantasan NG Cabuyao: Katapatan Subd., Banay Banay, City of CabuyaoLyca SorianoNo ratings yet

- 11th Com DepreciationDocument4 pages11th Com DepreciationObaid KhanNo ratings yet

- 1 Alfino Borrowed Money From Yakutsk and Agreed in WritingDocument1 page1 Alfino Borrowed Money From Yakutsk and Agreed in Writingjoanne bajetaNo ratings yet

- Earnings Management: A Review of Selected Cases: July 2018Document15 pagesEarnings Management: A Review of Selected Cases: July 2018Andre SetiawanNo ratings yet

- Federal Reserve Lien Ammended AgainDocument3 pagesFederal Reserve Lien Ammended AgainCharles Scott0% (1)

- Chapter 4: Analysis of Financial StatementsDocument50 pagesChapter 4: Analysis of Financial StatementsHope Trinity EnriquezNo ratings yet

- Prop Firm Drawdown Limitations - Forex Prop ReviewsDocument9 pagesProp Firm Drawdown Limitations - Forex Prop ReviewsMye RakNo ratings yet

- Risk Management Framework For Indian BanksDocument8 pagesRisk Management Framework For Indian BankstapanroutrayNo ratings yet

- Form 16Document6 pagesForm 16Pulkit Gupta100% (1)

- International Banking-Euro Bank, Types of Banking Offices, Correspondent Bank, Representative Bank 5Document20 pagesInternational Banking-Euro Bank, Types of Banking Offices, Correspondent Bank, Representative Bank 5Chintakunta PreethiNo ratings yet

- Jurnal 2 - Alaeto Henry Emeka (2020) - Determinants - of - Dividend - Polic - NigeriaDocument31 pagesJurnal 2 - Alaeto Henry Emeka (2020) - Determinants - of - Dividend - Polic - NigeriaGilang KotawaNo ratings yet

- Carried Lumber Co. vs. ACCFADocument6 pagesCarried Lumber Co. vs. ACCFAJENNY BUTACANNo ratings yet

- HLB SME 1form (Original)Document14 pagesHLB SME 1form (Original)Mandy ChanNo ratings yet

- Topic 7 - Forecasting Financial Statements (Updated)Document64 pagesTopic 7 - Forecasting Financial Statements (Updated)Jasmine JacksonNo ratings yet

- A B C D: 02 Objective / Objektif 2Document5 pagesA B C D: 02 Objective / Objektif 2foryourhonour wongNo ratings yet

- Chapter No. 2Document46 pagesChapter No. 2Muhammad SalmanNo ratings yet

- IC38 Janamghutti v1 10052019 PDFDocument67 pagesIC38 Janamghutti v1 10052019 PDFMahesh S Gour75% (4)