You might also like

- SarfaesiDocument11 pagesSarfaesishyam agrawalNo ratings yet

- SARFAESI Act and Case Study Presentation SummaryDocument22 pagesSARFAESI Act and Case Study Presentation Summarylakshmi govindaprasadNo ratings yet

- Overview of Sarfaesi Act, 2002Document8 pagesOverview of Sarfaesi Act, 2002Pragati OjhaNo ratings yet

- CHAPTERDocument55 pagesCHAPTERwashimNo ratings yet

- SARFAESI Act 2002: Banks' Tool for NPA RecoveryDocument3 pagesSARFAESI Act 2002: Banks' Tool for NPA RecoveryRam IyerNo ratings yet

- SARFAESI Act, 2002: How It Works?Document4 pagesSARFAESI Act, 2002: How It Works?Kriti KhareNo ratings yet

- SARFAESI ACT PROVISIONS FOR NPA RECOVERYDocument6 pagesSARFAESI ACT PROVISIONS FOR NPA RECOVERYGunjeetNo ratings yet

- SARFAESI Act - Empowers banks to recover NPAs without court interventionDocument3 pagesSARFAESI Act - Empowers banks to recover NPAs without court interventionsubhasis123bbsrNo ratings yet

- SARFAESI Act, 2002: How It Works?Document4 pagesSARFAESI Act, 2002: How It Works?Anurag KumarNo ratings yet

- Sarfaesi ActDocument10 pagesSarfaesi ActramyaNo ratings yet

- Sarfaesi ActDocument3 pagesSarfaesi ActJatin PanchiNo ratings yet

- Sarfaesi ActDocument14 pagesSarfaesi ActAnup SinghNo ratings yet

- Sarfaesi Act PPT-1Document21 pagesSarfaesi Act PPT-1Vironika Reddy100% (1)

- Pages From CRILW - PART - II - BOOKDocument3 pagesPages From CRILW - PART - II - BOOKG??No ratings yet

- SecuritisationDocument16 pagesSecuritisationvishavjitbonkra1384No ratings yet

- SARFAESI Act: Secured creditors' rights for NPA recoveryDocument9 pagesSARFAESI Act: Secured creditors' rights for NPA recoveryDeepak Mangal0% (1)

- Final-Sarfaesi Act 2002Document41 pagesFinal-Sarfaesi Act 2002ninpra50% (2)

- Banking Law - Mritunjaya SinghDocument14 pagesBanking Law - Mritunjaya SinghMritunjaya SinghNo ratings yet

- Sarfaesi Act 2002Document27 pagesSarfaesi Act 2002Prajakta MantriNo ratings yet

- SARFAESI Act, 2002: Fatcs and Method of Working For: Jaiib ExamDocument10 pagesSARFAESI Act, 2002: Fatcs and Method of Working For: Jaiib ExamsiddNo ratings yet

- The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (Sarfaesi)Document15 pagesThe Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (Sarfaesi)DEV PORUS SURNo ratings yet

- Sarfaesi ActDocument13 pagesSarfaesi Act..sravana karthik100% (5)

- Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (Sarfaesi) and Npa ManagementDocument20 pagesSecuritisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (Sarfaesi) and Npa ManagementShirsendu DasNo ratings yet

- Objectives and Purpose of the SARFAESI ActDocument3 pagesObjectives and Purpose of the SARFAESI Actmansi rathiNo ratings yet

- JAIIB Paper 3 Module C Banking Related Laws Download PDFDocument42 pagesJAIIB Paper 3 Module C Banking Related Laws Download PDFstudy studyNo ratings yet

- SARFESI (Securitisation & Reconstruction and Enforcement of Security Interest)Document22 pagesSARFESI (Securitisation & Reconstruction and Enforcement of Security Interest)BaazingaFeedsNo ratings yet

- An AssetDocument8 pagesAn AssetFayiz SubairNo ratings yet

- Sarfaesi Act, 2002 PptnewDocument27 pagesSarfaesi Act, 2002 PptnewCharu Pundir50% (2)

- Act, 1993:-The Procedure For Recovery of Debts To The Banks and FinancialDocument7 pagesAct, 1993:-The Procedure For Recovery of Debts To The Banks and FinancialK KOTHAND RAMI REDDYNo ratings yet

- Banking Related Laws: Dr.P.R.Kulkarni111 August 15, 2011Document54 pagesBanking Related Laws: Dr.P.R.Kulkarni111 August 15, 2011calmchandanNo ratings yet

- SARFAESI Act 2002: Sujay Somani (9152) Amit Thakur (9157) Pallawi Sawaitul (9149)Document25 pagesSARFAESI Act 2002: Sujay Somani (9152) Amit Thakur (9157) Pallawi Sawaitul (9149)Sujay SomaniNo ratings yet

- Ibc V SarfesiDocument24 pagesIbc V SarfesisahilNo ratings yet

- Sarfaesi ACT, 2002: Project Presentstion BY Smit GandhiDocument16 pagesSarfaesi ACT, 2002: Project Presentstion BY Smit GandhismitNo ratings yet

- SARFAESI ACT SECURITISATIONDocument13 pagesSARFAESI ACT SECURITISATIONKishor Satpute0% (1)

- Securitisation of Debt (Loan Assets)Document7 pagesSecuritisation of Debt (Loan Assets)Sanskar YadavNo ratings yet

- Unit 1 - Session 1Document15 pagesUnit 1 - Session 1sgsoni78No ratings yet

- Sarfaesi Act 2002 PptnewDocument27 pagesSarfaesi Act 2002 PptnewHarshSuryavanshiNo ratings yet

- Sarfaesi Act in India: IILM GSM (BATCH: 2011-13)Document20 pagesSarfaesi Act in India: IILM GSM (BATCH: 2011-13)Krishnendu ChowdhuryNo ratings yet

- Sarfaesi Act Most Effective Tool To Recover Bad LoansDocument5 pagesSarfaesi Act Most Effective Tool To Recover Bad LoansSandra AdamsNo ratings yet

- Sarfaesi, IBC PDFDocument14 pagesSarfaesi, IBC PDFSHASHWAT MISHRANo ratings yet

- A Banking Law Presentation On SARFAESI ADocument23 pagesA Banking Law Presentation On SARFAESI AChandra RajanNo ratings yet

- SARFESI (Securitisation & Reconstruction and Enforcement of Security Interest)Document15 pagesSARFESI (Securitisation & Reconstruction and Enforcement of Security Interest)BaazingaFeedsNo ratings yet

- June 8, Sarfaesi Act B.voc. BVB 103unit I &IIDocument12 pagesJune 8, Sarfaesi Act B.voc. BVB 103unit I &II634Vinayak khetanNo ratings yet

- Sarfaesi Act 2002Document3 pagesSarfaesi Act 2002Basavaraju K RNo ratings yet

- Sarfaesi ActDocument8 pagesSarfaesi Actvrkesavan100% (2)

- Tools For Recovering NpaDocument4 pagesTools For Recovering Npanchaudhari_2100% (2)

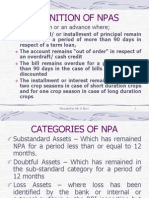

- Definition of Npas: A NPA Is A Loan or An Advance WhereDocument30 pagesDefinition of Npas: A NPA Is A Loan or An Advance WheremulchandranaNo ratings yet

- Law and Economics ProjectDocument15 pagesLaw and Economics Projectakshat0tiwariNo ratings yet

- Management of Non-Performing Assets: Presentation by Mr. S. RaviDocument29 pagesManagement of Non-Performing Assets: Presentation by Mr. S. RaviRajesh MaddiNo ratings yet

- Asset ReconstructionDocument20 pagesAsset Reconstructionlukeskywalker100No ratings yet

- BFNIADocument29 pagesBFNIArheakhandke2001No ratings yet

- PPT7 - SarfaesiDocument65 pagesPPT7 - SarfaesiDevansh JoshiNo ratings yet

- SARFAESI Act Enforcement ProcessDocument5 pagesSARFAESI Act Enforcement Processsaisankar ladiNo ratings yet

- Insolvency and Bankruptcy Code 2016Document4 pagesInsolvency and Bankruptcy Code 2016Tanima SoodNo ratings yet

- Indian Act Streamlines Bad Debt RecoveryDocument1 pageIndian Act Streamlines Bad Debt RecoveryTisha GuglianiNo ratings yet

- According To Black's Law DictionaryDocument6 pagesAccording To Black's Law DictionaryDeepak YadavNo ratings yet

- Addendum To Module 1 - SARFAESI-merged With ChartsDocument65 pagesAddendum To Module 1 - SARFAESI-merged With ChartsRAGI. KNo ratings yet

- SARFAESI ACT Explained: Key Definitions, Enforcement Process and MoreDocument4 pagesSARFAESI ACT Explained: Key Definitions, Enforcement Process and MoresrinivaspdfNo ratings yet

- Screenshot 2023-11-23 at 6.29.59 PMDocument8 pagesScreenshot 2023-11-23 at 6.29.59 PMVasant bhoknalNo ratings yet

- Chart of AccountsDocument3 pagesChart of AccountsOzioma Ihekwoaba0% (1)

- Cross-Border InsolvencyDocument3 pagesCross-Border InsolvencySameeksha KashyapNo ratings yet

- BAM 242 Pre Final Exam PointersDocument2 pagesBAM 242 Pre Final Exam PointersMarielle Dela Torre LubatNo ratings yet

- A Detailed Study of Winding Up of A CompanyDocument7 pagesA Detailed Study of Winding Up of A CompanyIJRASETPublicationsNo ratings yet

- Minggu 2 - 3 - Time Value of MoneyDocument79 pagesMinggu 2 - 3 - Time Value of MoneylisdhiyantoNo ratings yet

- Contract of Antichresis Loan AgreementDocument2 pagesContract of Antichresis Loan AgreementcrisypilNo ratings yet

- BDO Secretary CertificateDocument2 pagesBDO Secretary CertificateDeliaNo ratings yet

- Test 1 August 2022 PDFDocument11 pagesTest 1 August 2022 PDFIjaaz AjouhaarNo ratings yet

- Time Value of Money: Future Value Present Value Annuities Rates of Return AmortizationDocument55 pagesTime Value of Money: Future Value Present Value Annuities Rates of Return Amortizationfaheem qureshiNo ratings yet

- Sundaravalli Subramanian ReportDocument4 pagesSundaravalli Subramanian ReportManish KumarNo ratings yet

- How Much Does It Really CostDocument2 pagesHow Much Does It Really Costapi-372302973No ratings yet

- Finance Module 10 Managing Personal FinanceDocument4 pagesFinance Module 10 Managing Personal FinanceKJ JonesNo ratings yet

- Truth in Lending Act SlidesDocument6 pagesTruth in Lending Act SlidesSherine Vizconde100% (1)

- Mortgage Refinancing Benefits You Must KnowDocument3 pagesMortgage Refinancing Benefits You Must KnowriyaNo ratings yet

- PALOMARIA-MODULE 4 - Consumer MathDocument16 pagesPALOMARIA-MODULE 4 - Consumer MathALMIRA LOUISE PALOMARIANo ratings yet

- Etfeb 23Document131 pagesEtfeb 23new placeNo ratings yet

- FOREIGN DOLL CORP May 2023 TD StatementDocument4 pagesFOREIGN DOLL CORP May 2023 TD Statementlesly malebrancheNo ratings yet

- Transactions 600 051949600 20220324 160153Document2 pagesTransactions 600 051949600 20220324 160153Hemanth Kumar NNo ratings yet

- C2 Bank ReconciliationDocument22 pagesC2 Bank ReconciliationKenzel lawasNo ratings yet

- Midterm Exam in Business LogicDocument5 pagesMidterm Exam in Business LogicMaguan, Vincent Paul A.No ratings yet

- Olive Green Neutral Declutter Simple Living How To Guide Ebook CoverDocument6 pagesOlive Green Neutral Declutter Simple Living How To Guide Ebook Covernijhoom624No ratings yet

- IBK - Personal Finance and BudgetingDocument18 pagesIBK - Personal Finance and Budgetingisaackwegyir2No ratings yet

- Unit 2 FRQ AnswersDocument4 pagesUnit 2 FRQ AnswersThe uploaderNo ratings yet

- 7 - T24 - Account FunctionsDocument41 pages7 - T24 - Account FunctionsPranay SahuNo ratings yet

- (AyslipipsDocument5 pages(AyslipipsJee AlmanzorNo ratings yet

- Homework #3-Business Transfer TaxesDocument9 pagesHomework #3-Business Transfer TaxesQuendrick SurbanNo ratings yet

- HSBC Financial Analysis PPDocument68 pagesHSBC Financial Analysis PPKareem L SayidNo ratings yet

- BankingDocument74 pagesBankingAbhishek DubeyNo ratings yet

- 23-350001 Merit - Warba InvoiceDocument4 pages23-350001 Merit - Warba InvoicerameeshaNo ratings yet