You might also like

- Lanen 5e ch13 StudentDocument39 pagesLanen 5e ch13 StudentDagnachew TsegayeNo ratings yet

- Budgeting 101: By: Limheya Lester Glenn National University-ManilaDocument42 pagesBudgeting 101: By: Limheya Lester Glenn National University-ManilaXXXXXXXXXXXXXXXXXXNo ratings yet

- Lecture 5-6 Master BudgetDocument19 pagesLecture 5-6 Master BudgetFathurrahman AnwarNo ratings yet

- IPPTChap013 000Document39 pagesIPPTChap013 000Merly JusayanNo ratings yet

- CH 13Document29 pagesCH 13Prinzz TaylorNo ratings yet

- Group Iii. Business FinanceDocument11 pagesGroup Iii. Business FinanceChristian PhilipNo ratings yet

- Financial Planning and ManagementDocument13 pagesFinancial Planning and ManagementHazel AmionNo ratings yet

- MPA 602: Cost and Managerial AccountingDocument119 pagesMPA 602: Cost and Managerial AccountingMd. ZakariaNo ratings yet

- Budget Matterial For The Students NewDocument10 pagesBudget Matterial For The Students NewheysemNo ratings yet

- BuggetDocument45 pagesBuggetTrexie De Vera JaymeNo ratings yet

- Key Lecture Concepts: Master Budget: Operational and Financial BudgetsDocument13 pagesKey Lecture Concepts: Master Budget: Operational and Financial BudgetsaNo ratings yet

- Chapter Iii. Master Budget: An Overall Plan: Page 1 of 19Document19 pagesChapter Iii. Master Budget: An Overall Plan: Page 1 of 19Nahum DaichaNo ratings yet

- Teodoro M. Luansing College of Rosario: Senior High School DepartmentDocument7 pagesTeodoro M. Luansing College of Rosario: Senior High School DepartmentSamantha Alice LysanderNo ratings yet

- Master BudgetDocument45 pagesMaster BudgetJay Mark AbellarNo ratings yet

- Hilton 11e Chap009PPTDocument51 pagesHilton 11e Chap009PPTNgọc ĐỗNo ratings yet

- Budgetary Planning and Control: 7.1 Nature and Purposes of BudgetsDocument18 pagesBudgetary Planning and Control: 7.1 Nature and Purposes of Budgetsserge folegweNo ratings yet

- Week 8 - Lecture Budgeting v3Document23 pagesWeek 8 - Lecture Budgeting v3NabilNo ratings yet

- Chapter 4A Financial Planning ManagementDocument20 pagesChapter 4A Financial Planning ManagementAlexa RomarateNo ratings yet

- Master BudgetDocument34 pagesMaster BudgetAnnabel SenitaNo ratings yet

- Module 3 - Topic 2Document4 pagesModule 3 - Topic 2Moon LightNo ratings yet

- Horngrens Financial and Managerial Accounting The Managerial Chapters 4Th Edition Nobles Solutions Manual Download PDF 2024Document133 pagesHorngrens Financial and Managerial Accounting The Managerial Chapters 4Th Edition Nobles Solutions Manual Download PDF 2024thomas.casey387100% (18)

- Budgets & Budgetary Control Systems: Prepared byDocument35 pagesBudgets & Budgetary Control Systems: Prepared byShakil AnwaarNo ratings yet

- Budgetary Planning and ControlDocument67 pagesBudgetary Planning and ControlJade Ballado-TanNo ratings yet

- Lecture 5-6 BudgetingDocument15 pagesLecture 5-6 BudgetingAfzal AhmedNo ratings yet

- Handout 1 UnlockedDocument14 pagesHandout 1 UnlockedRhaffe DaydayNo ratings yet

- Financial Planning and BudgetingDocument33 pagesFinancial Planning and Budgetingsalonzonicole04No ratings yet

- Accounting & Control: Cost ManagementDocument41 pagesAccounting & Control: Cost ManagementMeriskaNo ratings yet

- Hilton 11e Chap009PPTDocument52 pagesHilton 11e Chap009PPTNgô Khánh HòaNo ratings yet

- Analysis Master BudgetDocument40 pagesAnalysis Master BudgetAisyahNo ratings yet

- CH04Document35 pagesCH04Elen LimNo ratings yet

- Budgeting For Planning and Control: Cengage Learning and South-Western Are Trademarks Used Herein Under LicenseDocument41 pagesBudgeting For Planning and Control: Cengage Learning and South-Western Are Trademarks Used Herein Under LicenseSetiani Putri HendratnoNo ratings yet

- 6e ch08Document42 pages6e ch08Ever PuebloNo ratings yet

- Financial Planning and Analysis: The Master Budget: Mcgraw-Hill/IrwinDocument52 pagesFinancial Planning and Analysis: The Master Budget: Mcgraw-Hill/IrwinAmirah ZNo ratings yet

- Cost and Management Accounting IIDocument9 pagesCost and Management Accounting IIarefayne wodajoNo ratings yet

- Test Bank For Managerial Accounting 1st Edition BalakrishnanDocument28 pagesTest Bank For Managerial Accounting 1st Edition Balakrishnanjohnortizgaiofnqjsz100% (22)

- VI. Budgeting and Financial ForecastingDocument39 pagesVI. Budgeting and Financial ForecastingJemNo ratings yet

- Midterm Topic 4.1 - Notes - Sales Budgets and Production BudgetsDocument2 pagesMidterm Topic 4.1 - Notes - Sales Budgets and Production BudgetslanoyjessicaellahNo ratings yet

- Financial Projections-TextDocument5 pagesFinancial Projections-TextFarid UddinNo ratings yet

- Budgeting: Afzal Ahmed, Fca Finance Controller NagadDocument19 pagesBudgeting: Afzal Ahmed, Fca Finance Controller NagadsajedulNo ratings yet

- RL R.% - R. N : Rga, A/"Document4 pagesRL R.% - R. N : Rga, A/"Vince De GuzmanNo ratings yet

- FP & B (PPT Lecture)Document38 pagesFP & B (PPT Lecture)Dyan LacanlaleNo ratings yet

- Assignment A2: The University of Danang University of Economics Center For International EducationDocument9 pagesAssignment A2: The University of Danang University of Economics Center For International EducationBảo OliverNo ratings yet

- Types of Budget: A Project Report OnDocument15 pagesTypes of Budget: A Project Report OnForam ShahNo ratings yet

- LAS 3 Business-FinanceDocument12 pagesLAS 3 Business-FinanceVenus AriateNo ratings yet

- Topic 3 - Master BudgetDocument21 pagesTopic 3 - Master BudgetQuỳnh ĐỗNo ratings yet

- BudgetDocument13 pagesBudgetstaycgirls itsgoingdownNo ratings yet

- Budget (!Document6 pagesBudget (!Timilehin GbengaNo ratings yet

- Topic 1 - BudgetingDocument27 pagesTopic 1 - Budgetingmarlina rahmatNo ratings yet

- MPT15L4DEems6BL4PyEw - A - Module 4 Example Cases SolutionsDocument64 pagesMPT15L4DEems6BL4PyEw - A - Module 4 Example Cases SolutionsSonali AgarwalNo ratings yet

- MGMT 027 Chapter 08 Slides OnlineDocument89 pagesMGMT 027 Chapter 08 Slides OnlineCeline Kaye AbadNo ratings yet

- L5257 - 1 Introduction 2017Document46 pagesL5257 - 1 Introduction 2017Reza Nursyah PutraNo ratings yet

- ch19 Revised 2020Document41 pagesch19 Revised 2020Nicole DavilaNo ratings yet

- BudgetingDocument20 pagesBudgetingRakesh JhaNo ratings yet

- Aaa A!"# Aaa A! "Document4 pagesAaa A!"# Aaa A! "sandeepssn47No ratings yet

- Budget PreparationDocument33 pagesBudget PreparationLizbethHazelRiveraNo ratings yet

- Ch1 - Master BudgetDocument38 pagesCh1 - Master BudgetProf. Nisaif JasimNo ratings yet

- MAS - 1.2.5 Integrated Review & Refresher in Accountancy R.D.BalocatingDocument6 pagesMAS - 1.2.5 Integrated Review & Refresher in Accountancy R.D.BalocatingLOUISE ELIJAH GACUANNo ratings yet

- Chapter 4 Masrter BudgetDocument17 pagesChapter 4 Masrter BudgetCabdiraxmaan GeeldoonNo ratings yet

- Ch08 - Guan CM - AISEDocument42 pagesCh08 - Guan CM - AISEIassa MarcelinaNo ratings yet

- Guide to Management Accounting CCC (Cash Conversion Cycle) for managersFrom EverandGuide to Management Accounting CCC (Cash Conversion Cycle) for managersNo ratings yet

- Balance Sheet: Blaster LTDDocument2 pagesBalance Sheet: Blaster LTDrahul khaithanNo ratings yet

- Term Paper of Working CapitalDocument20 pagesTerm Paper of Working CapitalShiwanee RaoNo ratings yet

- Fin2001 Pset4Document10 pagesFin2001 Pset4Valeria MartinezNo ratings yet

- Keac 211Document38 pagesKeac 211vichmegaNo ratings yet

- Dasra in 2013 14 (Annual Report)Document56 pagesDasra in 2013 14 (Annual Report)asanjeevraoNo ratings yet

- Assignment 2 Transactions To FS AnswerDocument24 pagesAssignment 2 Transactions To FS AnswerJorniNo ratings yet

- Abm Acctg Firm Section 2am 2Document40 pagesAbm Acctg Firm Section 2am 2Diana Rosales CalNo ratings yet

- Funds FlowDocument5 pagesFunds FlowSubha KalyanNo ratings yet

- Useful For Certified Accounting & Audit Professional 1Document340 pagesUseful For Certified Accounting & Audit Professional 1nageswara kuchipudi100% (1)

- Chapter 3 - Intangible Assets (IAS 38)Document7 pagesChapter 3 - Intangible Assets (IAS 38)Yaamin Mohamed NiyazNo ratings yet

- Balance Sheet of JK Tyre and IndustriesDocument4 pagesBalance Sheet of JK Tyre and IndustriesHimanshu MangeNo ratings yet

- ACC6050 Module 3 AssignmentDocument9 pagesACC6050 Module 3 AssignmentFavourNo ratings yet

- Balance of Payments AUSDocument36 pagesBalance of Payments AUSKoushik SenNo ratings yet

- Withdrawal or Retirement of A PartnerDocument8 pagesWithdrawal or Retirement of A PartnerReyes LykaNo ratings yet

- Topic 6 - Recording Year End AdjustmentsDocument71 pagesTopic 6 - Recording Year End AdjustmentsdenixngNo ratings yet

- BMBE LawDocument3 pagesBMBE LawGerry Malgapo100% (1)

- FA Session 1Document75 pagesFA Session 1keenodiidNo ratings yet

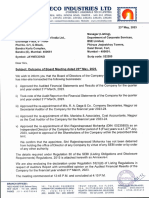

- Jayaswal Neco Industries LTDDocument13 pagesJayaswal Neco Industries LTDMannu SinghNo ratings yet

- RiskCalc 3.1 WhitepaperDocument36 pagesRiskCalc 3.1 Whitepaperiver2340_729926247No ratings yet

- Ibu Dyah Anjarwati - Materi Workshop WP&B Schedules - Batam 300710 (Compatibility Mode)Document70 pagesIbu Dyah Anjarwati - Materi Workshop WP&B Schedules - Batam 300710 (Compatibility Mode)mohammad basukiNo ratings yet

- CFAS Module Week 3-4Document13 pagesCFAS Module Week 3-4Yamit, Angel Marie A.No ratings yet

- Cpa Review School of The Philippines ManilaDocument6 pagesCpa Review School of The Philippines ManilaKyrie Gwynette OlarveNo ratings yet

- The Professional CPA Review School: Advanced Financial Accounting & Reporting Summary Notes On Government AccountingDocument14 pagesThe Professional CPA Review School: Advanced Financial Accounting & Reporting Summary Notes On Government Accountingjohn francisNo ratings yet

- Day1 IAS-16Document44 pagesDay1 IAS-16tariq hassaNo ratings yet

- IDEAL RICE INDUSTRIES AccountsDocument89 pagesIDEAL RICE INDUSTRIES Accountsahmed.zjcNo ratings yet

- Financial Management Handbook 1704942604Document45 pagesFinancial Management Handbook 1704942604alenNo ratings yet

- Fabm1 q3 Mod3 Accountingequation FinalDocument28 pagesFabm1 q3 Mod3 Accountingequation FinalAdonis Zoleta Aranillo50% (8)

- Caplin Point LabDocument76 pagesCaplin Point Lab40 Sai VenkatNo ratings yet

- Afar302 A - PD 3Document5 pagesAfar302 A - PD 3Nicole TeruelNo ratings yet

- AS-2-Valuation of Inventories PDFDocument6 pagesAS-2-Valuation of Inventories PDFRanjith Kumar CANo ratings yet