You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Intro To ProbabilityDocument64 pagesIntro To ProbabilityyasheshgaglaniNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Random VariableDocument13 pagesRandom VariableyasheshgaglaniNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Psyc 235: Introduction To Statistics: Don'T Forget To Sign in For Credit!Document41 pagesPsyc 235: Introduction To Statistics: Don'T Forget To Sign in For Credit!yasheshgaglaniNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Confidence IntervalsDocument30 pagesConfidence IntervalsyasheshgaglaniNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Chi Square DefinitionDocument1 pageChi Square DefinitionyasheshgaglaniNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Descriptive Stats (E.g., Mean, Median, Mode, Standard Deviation) Z-Test &/or T-Test For A Single Population Parameter (E.g., Mean)Document43 pagesDescriptive Stats (E.g., Mean, Median, Mode, Standard Deviation) Z-Test &/or T-Test For A Single Population Parameter (E.g., Mean)yasheshgaglaniNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Statistical MethodsDocument16 pagesStatistical MethodsyasheshgaglaniNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Generations of ComputersDocument3 pagesGenerations of ComputersyasheshgaglaniNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Team Work & Team Building: M Sutapa LakshmananDocument22 pagesTeam Work & Team Building: M Sutapa LakshmananyasheshgaglaniNo ratings yet

- Pricing MethodsDocument11 pagesPricing MethodsyasheshgaglaniNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Project Study On Microsoft Office Sharepoint Server (Moss)Document46 pagesProject Study On Microsoft Office Sharepoint Server (Moss)yasheshgaglaniNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Managerial Defi Nature, ScopeDocument15 pagesManagerial Defi Nature, ScopeyasheshgaglaniNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Objectives of A FirmDocument3 pagesObjectives of A Firmyasheshgaglani100% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Excel FormulaeDocument6 pagesExcel FormulaeyasheshgaglaniNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Introduction To Computers and IT: Click To Edit Master Subtitle StyleDocument29 pagesIntroduction To Computers and IT: Click To Edit Master Subtitle StyleyasheshgaglaniNo ratings yet

- Inflation AccountingDocument9 pagesInflation AccountingyasheshgaglaniNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Inventory ManagementDocument5 pagesInventory ManagementyasheshgaglaniNo ratings yet

- Accounting StandardsDocument14 pagesAccounting StandardsyasheshgaglaniNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Ethical Issues in Accounting and FinanceDocument14 pagesEthical Issues in Accounting and Financeyasheshgaglani100% (1)

- High Performance Leadership-Overview: Prof M Sutapa LakshmananDocument15 pagesHigh Performance Leadership-Overview: Prof M Sutapa LakshmananyasheshgaglaniNo ratings yet

- Basic Concepts Session 2Document17 pagesBasic Concepts Session 2yasheshgaglaniNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Positive Thinking: M Sutapa LakshmananDocument19 pagesPositive Thinking: M Sutapa LakshmananyasheshgaglaniNo ratings yet

- Positive Psychology 9.12.10Document14 pagesPositive Psychology 9.12.10yasheshgaglaniNo ratings yet

- Conflict CHN 12.11.10Document22 pagesConflict CHN 12.11.10yasheshgaglaniNo ratings yet

- Conflict Management: Coping Strategies: M Sutapa LakshmananDocument14 pagesConflict Management: Coping Strategies: M Sutapa LakshmananyasheshgaglaniNo ratings yet

- High Performance Leadership-: Prof M Sutapa LakshmananDocument15 pagesHigh Performance Leadership-: Prof M Sutapa LakshmananyasheshgaglaniNo ratings yet

- HPL Leadership StylesDocument31 pagesHPL Leadership Stylesankushrasam700No ratings yet

- High Performance Leadership 1Document14 pagesHigh Performance Leadership 1yasheshgaglaniNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Multiple Choice 1Document5 pagesMultiple Choice 1віра сіркаNo ratings yet

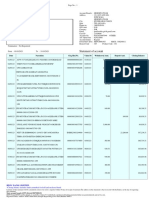

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument3 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceSakethNo ratings yet

- Layman's Guide To Pair TradingDocument9 pagesLayman's Guide To Pair TradingaporatNo ratings yet

- B2B Marketing Attribution 101 EbookDocument48 pagesB2B Marketing Attribution 101 EbookThuyDuongNo ratings yet

- Standard Financial Analysis Tool: Project Name HereDocument15 pagesStandard Financial Analysis Tool: Project Name HereBharath.v kumarNo ratings yet

- 6481 01 Ansoff Growth MatrixDocument11 pages6481 01 Ansoff Growth MatrixKarim2030No ratings yet

- WalmartDocument14 pagesWalmartMashal IdreesNo ratings yet

- Kotler Pom 15e Inppt 07 GEDocument49 pagesKotler Pom 15e Inppt 07 GEMohammed ElmisinyNo ratings yet

- 2 Hour Agency QuickstartDocument14 pages2 Hour Agency QuickstartMing Xiu Ho100% (1)

- ITR Compilation 4u5346Document4 pagesITR Compilation 4u5346akhil kwatraNo ratings yet

- Supply Chain Management: Author: B. Mahadevan Operations Management: Theory and Practice, 3eDocument31 pagesSupply Chain Management: Author: B. Mahadevan Operations Management: Theory and Practice, 3eAjmal sNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Omoré: Marketing MixDocument3 pagesOmoré: Marketing MixImran HanifNo ratings yet

- FinalDocument28 pagesFinalAvik NaskarNo ratings yet

- Recalde Karla ComplejoSatori Partial3Report PDFDocument6 pagesRecalde Karla ComplejoSatori Partial3Report PDFKarlita RecaldeNo ratings yet

- Exo UnileverDocument4 pagesExo UnileverfadilaNo ratings yet

- Joint ArrangementDocument3 pagesJoint ArrangementAlliah Mae AcostaNo ratings yet

- Economics Term II PDFDocument69 pagesEconomics Term II PDFAlans TechnicalNo ratings yet

- Corporate Growth MaximizationDocument13 pagesCorporate Growth MaximizationUmesh SahNo ratings yet

- Report On Surya NepalDocument22 pagesReport On Surya NepalBinay Giri40% (10)

- Fuyao Group 10Document6 pagesFuyao Group 10Kundan Thakan0% (1)

- Job Description Tower LeadDocument3 pagesJob Description Tower Leadpune1faultsNo ratings yet

- Chapter 1 GlobalizationDocument5 pagesChapter 1 GlobalizationEdwin SuparmanNo ratings yet

- Technical Finance Prep AnswersDocument28 pagesTechnical Finance Prep Answersajaw267No ratings yet

- Chapter4 Feasibility of Idea ContinueDocument27 pagesChapter4 Feasibility of Idea ContinueCao ChanNo ratings yet

- Homework - Set - Solutions Finance 2.2 PDFDocument18 pagesHomework - Set - Solutions Finance 2.2 PDFAnonymous EgWT5izpNo ratings yet

- TOWS Matrix (Zomato)Document3 pagesTOWS Matrix (Zomato)Prinsa SankhavaraNo ratings yet

- Inventory System SummaryDocument3 pagesInventory System SummaryDayanara CuevasNo ratings yet

- Sify Sample Aptitude Placement Paper Level1Document7 pagesSify Sample Aptitude Placement Paper Level1placementpapersampleNo ratings yet

- King Enterprises Is A Book Wholesaler King Hired A NewDocument1 pageKing Enterprises Is A Book Wholesaler King Hired A Newtrilocksp SinghNo ratings yet

- RedSeer Etailing Leadership Index AMJ 17Document17 pagesRedSeer Etailing Leadership Index AMJ 17Danish ShaikhNo ratings yet