You might also like

- Summary: Financial Intelligence: Review and Analysis of Berman and Knight's BookFrom EverandSummary: Financial Intelligence: Review and Analysis of Berman and Knight's BookNo ratings yet

- Basic Security Guard Training Practice QuizDocument71 pagesBasic Security Guard Training Practice QuizNarmatha100% (2)

- Assumptions - : Cash Flow From Operations $ 0Document4 pagesAssumptions - : Cash Flow From Operations $ 0Krish HegdeNo ratings yet

- June 2014Document1 pageJune 2014Deepak GuptaNo ratings yet

- MR. Rosiak PerpetualDocument13 pagesMR. Rosiak PerpetualSelfi Riani100% (2)

- IA 3 MidtermDocument9 pagesIA 3 MidtermMelanie Samsona100% (1)

- Chapter 5 Principls and ConceptsDocument10 pagesChapter 5 Principls and ConceptsawlachewNo ratings yet

- Valuation Concepts and MethodsDocument5 pagesValuation Concepts and MethodsYami HeatherNo ratings yet

- Lecture 1 Intro To FA Jan2018Document33 pagesLecture 1 Intro To FA Jan2018IssacNo ratings yet

- Accounting Principles-Chp 02Document12 pagesAccounting Principles-Chp 02Md. RuHul A.No ratings yet

- OBLICON Definition of TermsDocument9 pagesOBLICON Definition of TermsKimmy ShawwyNo ratings yet

- Conceptual Framework: Theoretical FoundationDocument13 pagesConceptual Framework: Theoretical FoundationAnne Jeaneth SevillaNo ratings yet

- Qualitative Characteristics of Accounting InformationDocument3 pagesQualitative Characteristics of Accounting InformationKshaf SulemanNo ratings yet

- LS 1 - ACCOUNTING AND ITS ENVIRONMENT Part 2Document53 pagesLS 1 - ACCOUNTING AND ITS ENVIRONMENT Part 2Danielle Angel Malana100% (1)

- Chapter 2 - Actg Framework & ConceptsDocument16 pagesChapter 2 - Actg Framework & ConceptsHana YusriNo ratings yet

- CH.2.1 Accounting Concepts, Principles, PoliciesDocument12 pagesCH.2.1 Accounting Concepts, Principles, PoliciesNicole TaboralouisNo ratings yet

- Conceptual FrameworkDocument21 pagesConceptual FrameworkArafat Rahman TalukderNo ratings yet

- LESSON 6 Accounting Concepts and PrinciplesDocument5 pagesLESSON 6 Accounting Concepts and PrinciplesUnamadable UnleomarableNo ratings yet

- Accounting Principles1Document19 pagesAccounting Principles1Iqra ShahidNo ratings yet

- Basic Accounting Concepts and PrinciplesDocument16 pagesBasic Accounting Concepts and PrinciplesRenmar CruzNo ratings yet

- Accounting Concepts and PrinciplesDocument5 pagesAccounting Concepts and PrinciplesAlex EiyzNo ratings yet

- ACCOUNTINGDocument6 pagesACCOUNTINGFe VhieNo ratings yet

- Revised Conceptual Framework: Rainiel C. Soriano, CPA, MBADocument60 pagesRevised Conceptual Framework: Rainiel C. Soriano, CPA, MBAMila VeranoNo ratings yet

- Conceptual Framework & Accounting Standards: Three Important ActivitiesDocument12 pagesConceptual Framework & Accounting Standards: Three Important ActivitiesKendiNo ratings yet

- Module-1 Intro To AccountingDocument4 pagesModule-1 Intro To AccountingPam Salalima AlemaniaNo ratings yet

- Financial AccountingDocument8 pagesFinancial AccountingKetan ThakkarNo ratings yet

- Accounting PrinciplesDocument21 pagesAccounting PrinciplesJonas S. MsigalaNo ratings yet

- Discussion No. 3 Conceptual Framework and The Accounting ProcessDocument3 pagesDiscussion No. 3 Conceptual Framework and The Accounting ProcessJullianneBalaseNo ratings yet

- Accounting PrinciplesDocument22 pagesAccounting PrinciplesAshiq HossainNo ratings yet

- Chapter Two: Conceptual Framework Underlying Financial ReportingDocument39 pagesChapter Two: Conceptual Framework Underlying Financial ReportingSteveKingNo ratings yet

- Elements of Financial StatementDocument33 pagesElements of Financial StatementKertik Singh100% (1)

- Chapter 4 2019 0 NewDocument61 pagesChapter 4 2019 0 Newnomthandazomtshweni574No ratings yet

- Why Are Financial Statements Important?Document23 pagesWhy Are Financial Statements Important?Dylan AdrianNo ratings yet

- Materi Kuliah 2 - Financial Reporting and AnalysisDocument90 pagesMateri Kuliah 2 - Financial Reporting and Analysisvia nurainiNo ratings yet

- Accounting Concepts and ConventionsDocument29 pagesAccounting Concepts and ConventionsSaad SulemanNo ratings yet

- Summary Notes - Conceptual Framework - Objective of Financial ReportingDocument5 pagesSummary Notes - Conceptual Framework - Objective of Financial ReportingEDMARK LUSPENo ratings yet

- Accounting Studies Stage 2: The Role of Accounting (PART 2)Document23 pagesAccounting Studies Stage 2: The Role of Accounting (PART 2)Leanne TehNo ratings yet

- Revised Conceptual Framework 1st LessonDocument18 pagesRevised Conceptual Framework 1st LessonheeeyjanengNo ratings yet

- Basic Accounting ConceptsDocument3 pagesBasic Accounting ConceptsVanSendrel Parate100% (1)

- Accounting Is The - Of: - , - and - EconomicDocument48 pagesAccounting Is The - Of: - , - and - EconomicKristia AnagapNo ratings yet

- Handout 2 Concepts and Principles of AccountingDocument5 pagesHandout 2 Concepts and Principles of AccountingRyzha JoyNo ratings yet

- CFAS ReviewerDocument10 pagesCFAS ReviewerBrigit MartinezNo ratings yet

- Lesson 1 PPT AccountingDocument12 pagesLesson 1 PPT AccountingArchieliz Espinosa AsesorNo ratings yet

- What Are The Accounting Concepts and ConventionsDocument3 pagesWhat Are The Accounting Concepts and ConventionsPriyanka PatilNo ratings yet

- Accounting Principles: Second Canadian EditionDocument30 pagesAccounting Principles: Second Canadian EditionJain EktaNo ratings yet

- Management Accounting - Chapter 1Document23 pagesManagement Accounting - Chapter 1Gulush MammadhasanovaNo ratings yet

- Accounting Principles: Second Canadian EditionDocument30 pagesAccounting Principles: Second Canadian EditionAhmed FahmyNo ratings yet

- CFAS Reviewer TOSDocument16 pagesCFAS Reviewer TOSRyan Malanum AbrioNo ratings yet

- Kuliah 3 4 Analisis AkuntansiDocument52 pagesKuliah 3 4 Analisis AkuntansiAnne SilverstoneNo ratings yet

- Lesson 2 - Accounting Concepts and PrinciplesDocument5 pagesLesson 2 - Accounting Concepts and PrinciplesJeyem AscueNo ratings yet

- ABM ReviewerDocument5 pagesABM ReviewerKRISTELLE ROSARIONo ratings yet

- ACF 1101 Financial Accounting: Revised Conceptual FrameworkDocument12 pagesACF 1101 Financial Accounting: Revised Conceptual FrameworkKogularamanan NithiananthanNo ratings yet

- Accounting FOR ManagementDocument63 pagesAccounting FOR ManagementAnonymous 1ClGHbiT0JNo ratings yet

- Lecture 2A Purpose of Financial StatementsDocument14 pagesLecture 2A Purpose of Financial StatementsParadoxicalNo ratings yet

- IFRS Conceptual FrameworkDocument16 pagesIFRS Conceptual FrameworkSheikh Sahil MobinNo ratings yet

- Group 1Document19 pagesGroup 1Wambo MonsterrNo ratings yet

- Ch.2b Accounting QCs and AssumptionsDocument13 pagesCh.2b Accounting QCs and Assumptionsyfzhizhi0214No ratings yet

- CLASS NOTES Topic 8 Conceptual Framework of AccountingDocument11 pagesCLASS NOTES Topic 8 Conceptual Framework of AccountingKiasha WarnerNo ratings yet

- Chapter 2 - Basic Accounting ConceptsDocument29 pagesChapter 2 - Basic Accounting ConceptsDan RyanNo ratings yet

- Copyofcopy3ofapresentation 150501110626 Conversion Gate01Document11 pagesCopyofcopy3ofapresentation 150501110626 Conversion Gate01Gian LawrenceNo ratings yet

- Financial Accounting For The Lending BankerDocument3 pagesFinancial Accounting For The Lending BankerRobert NzulwaNo ratings yet

- Conceptual Framework (Part 1)Document3 pagesConceptual Framework (Part 1)Eui KimNo ratings yet

- Accounting ConceptsDocument12 pagesAccounting ConceptsRidz ZNo ratings yet

- Conceptual Framework and Accounting StandardsDocument34 pagesConceptual Framework and Accounting StandardsJuaymah SabaNo ratings yet

- Accounting Concepts and PrinciplesDocument43 pagesAccounting Concepts and PrinciplesOliver RomeroNo ratings yet

- Powerpoint Individual PartDocument7 pagesPowerpoint Individual PartHarshveerNo ratings yet

- Powerpoint Individual PartDocument7 pagesPowerpoint Individual PartHarshveerNo ratings yet

- Module 2 - Starting FileDocument1 pageModule 2 - Starting FileHarshveerNo ratings yet

- CEF Broshure PACT Final NM - 210 X 210 MM - ENG - Web - PagesDocument24 pagesCEF Broshure PACT Final NM - 210 X 210 MM - ENG - Web - PagesСметководство & Ревизија «Калиман»No ratings yet

- Hilton7e PrefaceDocument37 pagesHilton7e PrefaceErma WulandariNo ratings yet

- Cae15 Chap16 TheoriesDocument21 pagesCae15 Chap16 TheoriesJomarNo ratings yet

- PGDM I Semester I Management Accounting - 1 (Ma-1) : 1. Course ObjectiveDocument4 pagesPGDM I Semester I Management Accounting - 1 (Ma-1) : 1. Course Objectivecooldude690No ratings yet

- How To Use This Competency-Based Learning MaterialDocument29 pagesHow To Use This Competency-Based Learning Materialaldren cedamon0% (1)

- The Accounting Cycle: Capturing Economic EventsDocument55 pagesThe Accounting Cycle: Capturing Economic EventsK KNo ratings yet

- CH 3.3 Errors - SDocument10 pagesCH 3.3 Errors - Sসাঈদ আহমদ0% (1)

- UPDATED SCHEDULE Departmental Quiz 1Document1 pageUPDATED SCHEDULE Departmental Quiz 1Elaine AntonioNo ratings yet

- 01 x01 Basic ConceptsDocument10 pages01 x01 Basic ConceptsXandae MempinNo ratings yet

- Oracle Fusion Enterprise StructureDocument59 pagesOracle Fusion Enterprise Structurepradeep191988No ratings yet

- Deloitte-A Roadmap To Accounting For Income Taxes (Nov2011)Document505 pagesDeloitte-A Roadmap To Accounting For Income Taxes (Nov2011)mistercobalt3511No ratings yet

- 08 Identifying & Assessing The Risks of Material MisstatementDocument5 pages08 Identifying & Assessing The Risks of Material Misstatementrandomlungs121223No ratings yet

- Acctng 304Document3 pagesAcctng 304Lloyd Lameon0% (1)

- Primary Books of AccountsDocument16 pagesPrimary Books of AccountsSaptha Gowda100% (1)

- Jad Payroll April 01-07 2022Document9 pagesJad Payroll April 01-07 2022Jervie JalaNo ratings yet

- Chapter 20: Audit of Other Accounts in The Statement of Profit or Loss and Comprehensive IncomeDocument9 pagesChapter 20: Audit of Other Accounts in The Statement of Profit or Loss and Comprehensive IncomeAnna TaylorNo ratings yet

- WWF Tanzania Vacancies AugustDocument24 pagesWWF Tanzania Vacancies AugustSaumu MbanoNo ratings yet

- Essentials of Accounting For Governmental and Not For Profit Organizations 11th Edition by Copley ISBN Solution ManualDocument9 pagesEssentials of Accounting For Governmental and Not For Profit Organizations 11th Edition by Copley ISBN Solution Manualbeatrice100% (24)

- Class 14 ExampleDocument4 pagesClass 14 Exampledeepanshu guptaNo ratings yet

- Iowa Judicial Branch State Court Administration: Todd NuccioDocument15 pagesIowa Judicial Branch State Court Administration: Todd Nucciovicki forchtNo ratings yet

- Particulars: Rs. RsDocument7 pagesParticulars: Rs. RsAnmol ChawlaNo ratings yet

- The Deferred COGS of Goods Account Is The New Feature Introduced in Release 12Document8 pagesThe Deferred COGS of Goods Account Is The New Feature Introduced in Release 12abhi210800% (1)

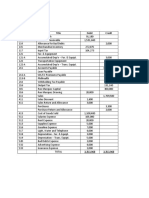

- Trial Balance February 28, 20X1Document3 pagesTrial Balance February 28, 20X1Angelica MaeNo ratings yet

- Admission ST James Naman& AnshuDocument7 pagesAdmission ST James Naman& AnshuDaleep SinghNo ratings yet

- Accounting For Income Taxes Accounting For Income TaxesDocument41 pagesAccounting For Income Taxes Accounting For Income TaxesankitmogheNo ratings yet