You might also like

- HRM9 Employee Benefits and CompensationDocument11 pagesHRM9 Employee Benefits and CompensationarantonizhaNo ratings yet

- Midterm Lecture 2 Employee Benefits and ServicesDocument7 pagesMidterm Lecture 2 Employee Benefits and ServicesJohn LesterNo ratings yet

- Page 1Document14 pagesPage 1JohnNo ratings yet

- Lesson 1: Employee CompensationDocument22 pagesLesson 1: Employee Compensationwilhelmina romanNo ratings yet

- Tax on Compensation Income Activity SheetDocument14 pagesTax on Compensation Income Activity SheetJudylyn SakitoNo ratings yet

- Benefits of A Wage EarnerDocument49 pagesBenefits of A Wage EarnerAmore BuenafeNo ratings yet

- INTGR TAX 005 Compensation IncomeDocument5 pagesINTGR TAX 005 Compensation IncomeZatsumono YamamotoNo ratings yet

- Employee Benefits and ServicesDocument31 pagesEmployee Benefits and ServicesEva Barrios LaweyanNo ratings yet

- HRM Unit 4Document47 pagesHRM Unit 4Kaushal SabalNo ratings yet

- MMMMDocument9 pagesMMMMABMachineryNo ratings yet

- Module No 7 - Exclusions From Gross IncomeDocument6 pagesModule No 7 - Exclusions From Gross IncomeLysss Epssss100% (1)

- Lesson 4 and 5Document7 pagesLesson 4 and 5Fatima Elsan OrillanNo ratings yet

- Module 10 Compensation Income.1Document22 pagesModule 10 Compensation Income.1Jeon KookieNo ratings yet

- Business Taxation (Compensation Income)Document67 pagesBusiness Taxation (Compensation Income)Robelyn FabriquelNo ratings yet

- Topic 3 - Compensation IncomeDocument13 pagesTopic 3 - Compensation IncomeRoxanne DiazNo ratings yet

- Income Taxation NotesDocument35 pagesIncome Taxation NotesLILIANNo ratings yet

- Lesson 5 Employee Benefits and ServicesDocument9 pagesLesson 5 Employee Benefits and ServicesAsylum LabyrinthNo ratings yet

- Chapter 9 - Employee Benefits and ServicesDocument41 pagesChapter 9 - Employee Benefits and Serviceschari.cadizNo ratings yet

- Employee BenefitsDocument18 pagesEmployee BenefitsSabarish .SNo ratings yet

- Chap 10-14: Compensation IncomeDocument44 pagesChap 10-14: Compensation IncomeArna Kaira Kjell DiestraNo ratings yet

- Week 3 Fringe Benefits Part 2 2023Document30 pagesWeek 3 Fringe Benefits Part 2 2023Arellano Rhovic R.No ratings yet

- BUSINESS MATHEMATICS Lesson 5 IONDocument9 pagesBUSINESS MATHEMATICS Lesson 5 IONPurple. Queen95100% (2)

- Chapter 8 Compensation and BenefitsDocument31 pagesChapter 8 Compensation and BenefitsRosan YaniseNo ratings yet

- Compensation Income (Notes)Document6 pagesCompensation Income (Notes)Anonymous LC5kFdtc100% (1)

- Module No 7 - Exclusions From Gross IncomeDocument5 pagesModule No 7 - Exclusions From Gross IncomeKatherine June CaoileNo ratings yet

- Gross Income: Learning ObjectivesDocument12 pagesGross Income: Learning ObjectivesClaire BarbaNo ratings yet

- CHAPTER 10 - IncomeTaxDocument3 pagesCHAPTER 10 - IncomeTaxVicente, Liza Mae C.No ratings yet

- G8 Compensation and BenefitsDocument19 pagesG8 Compensation and BenefitsAngelu ReboiraNo ratings yet

- Module 10 - Compensation IncomeDocument26 pagesModule 10 - Compensation IncomeJANELLE NUEZNo ratings yet

- HRM FinalllDocument43 pagesHRM FinalllPriyanka ShahNo ratings yet

- Session 2 - Compensation Income and FBTDocument6 pagesSession 2 - Compensation Income and FBTMitzi WamarNo ratings yet

- Comm Corona Virus Smallbiz Loan Final Revised PDFDocument4 pagesComm Corona Virus Smallbiz Loan Final Revised PDFAlex LinNo ratings yet

- Compensation and Incentives for EmployeesDocument2 pagesCompensation and Incentives for EmployeesLuis WashingtonNo ratings yet

- Income Disability InsuranceDocument12 pagesIncome Disability InsuranceHumbulani VhuthuhaweNo ratings yet

- Tax Chapter 10, 11, 12Document13 pagesTax Chapter 10, 11, 12Sheraldine MendozaNo ratings yet

- COMPENSATONDocument13 pagesCOMPENSATONAfreen ShahNo ratings yet

- BUSINESS MATH MODULE 4B For MANDAUE CITY DIVISIONDocument34 pagesBUSINESS MATH MODULE 4B For MANDAUE CITY DIVISIONJASON DAVID AMARILANo ratings yet

- Practical Accounting 2: BSA51E1 &BSA51E2Document68 pagesPractical Accounting 2: BSA51E1 &BSA51E2Carmelyn GonzalesNo ratings yet

- Maximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryFrom EverandMaximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryNo ratings yet

- BUS. MATH Q2 - Week4Document5 pagesBUS. MATH Q2 - Week4DARLENE MARTIN100% (1)

- Wala LangDocument5 pagesWala LangHOSPITAL EMERGENCY ROOMNo ratings yet

- Compensating Human ResourcesDocument13 pagesCompensating Human ResourcesM RABOY,JOHN NEIL D.No ratings yet

- Income Taxation Chapter on Compensation IncomeDocument17 pagesIncome Taxation Chapter on Compensation IncomeSheilamae Sernadilla GregorioNo ratings yet

- 1647 Unit-4-Compensation ManagementDocument13 pages1647 Unit-4-Compensation ManagementNITISH BALIYANNo ratings yet

- Benefits 187Document2 pagesBenefits 187Naimi SmithNo ratings yet

- Institute of Management and Computer Studies. (Imcost)Document23 pagesInstitute of Management and Computer Studies. (Imcost)24utsavNo ratings yet

- Compensation Income RulesDocument8 pagesCompensation Income RulesStanley Renz Obaña Dela CruzNo ratings yet

- Tax43-013-Compensation IncomeDocument22 pagesTax43-013-Compensation Incomelowi shooNo ratings yet

- Essentials of Federal Taxation Chapyter5-8Document16 pagesEssentials of Federal Taxation Chapyter5-8Amanda_CChenNo ratings yet

- Compensation Income and Fringe Benefit Tax. ReviewerDocument4 pagesCompensation Income and Fringe Benefit Tax. RevieweryzaNo ratings yet

- Incentives and BenefitsDocument14 pagesIncentives and BenefitsAditya PandeyNo ratings yet

- Adobe Scan Dec 09, 2023Document7 pagesAdobe Scan Dec 09, 2023Renalyn Ps MewagNo ratings yet

- Ba 211-Module 22-ReportDocument46 pagesBa 211-Module 22-ReportAlma AgnasNo ratings yet

- Submitted To: Amita Sharma Submitted By: Aditya Kumar Section-A Enrollment No. - 16flicddno1006Document14 pagesSubmitted To: Amita Sharma Submitted By: Aditya Kumar Section-A Enrollment No. - 16flicddno1006Aditya PandeyNo ratings yet

- Chapter 3 Taxation Part 1Document28 pagesChapter 3 Taxation Part 1Alhysa Rosales CatapangNo ratings yet

- Chapter 10 Compensation IncomeDocument4 pagesChapter 10 Compensation IncomeJason MablesNo ratings yet

- Kpit BenefitsDocument12 pagesKpit BenefitsRAHUL DAM100% (1)

- Income From SalaryDocument21 pagesIncome From SalaryAditya Avasare60% (10)

- Chapters 11 13Document68 pagesChapters 11 13Shanley Duenn UdtohanNo ratings yet

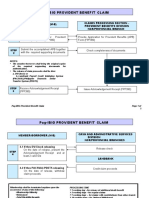

- Application For Provident Benefits (Apb) ClaimDocument2 pagesApplication For Provident Benefits (Apb) ClaimJoey Singson100% (1)

- ARC-Employee Handbook 09012016Document34 pagesARC-Employee Handbook 09012016Ann AyrosoNo ratings yet

- Cost Acctng Part2Document35 pagesCost Acctng Part2Genesis AuzaNo ratings yet

- DM Osds No. 094 S. 2021 Availment of Pag Ibig Loyalty Card PlusDocument2 pagesDM Osds No. 094 S. 2021 Availment of Pag Ibig Loyalty Card PlusRodel EstebanNo ratings yet

- Sample BudgetDocument109 pagesSample BudgetAnjannette SantosNo ratings yet

- Loyalty Card Plus: Application FormDocument2 pagesLoyalty Card Plus: Application FormJerome RealNo ratings yet

- CEBU NegoSale Batch 64042 060223Document21 pagesCEBU NegoSale Batch 64042 060223Shawn Gabriel EscasinasNo ratings yet

- Invitation To Submit Offer To PurchaseDocument32 pagesInvitation To Submit Offer To PurchaseCristina Dela CruzNo ratings yet

- Application For MRI - SRI ClaimDocument2 pagesApplication For MRI - SRI ClaimivyNo ratings yet

- A-Flour Co.: Acero, Crisha S. Galos, Eron G. Isaga, Sofia Pearl P. Pengson, Donna Lysa A. Reyes, Grant Dave RDocument94 pagesA-Flour Co.: Acero, Crisha S. Galos, Eron G. Isaga, Sofia Pearl P. Pengson, Donna Lysa A. Reyes, Grant Dave RxjammerNo ratings yet

- AEC - 12 - Q1 - 0402 - PS - Minimum Wages and Taxes Concerns of Filipino EntrepreneursDocument88 pagesAEC - 12 - Q1 - 0402 - PS - Minimum Wages and Taxes Concerns of Filipino EntrepreneursJust TinNo ratings yet

- Additional Examples of Income Tax For IndividualsDocument8 pagesAdditional Examples of Income Tax For IndividualsMary Rose BuaronNo ratings yet

- Bir and SssDocument5 pagesBir and SssJoselito de VeraNo ratings yet

- NegoSale Batch 15162 042823Document38 pagesNegoSale Batch 15162 042823Lee ViosaNo ratings yet

- Executive Order No. 90 Defines Housing AgenciesDocument11 pagesExecutive Order No. 90 Defines Housing AgenciesMarlon BertuldoNo ratings yet

- Chapter 6 8 Organization and ManagementDocument17 pagesChapter 6 8 Organization and Managementandrea balabatNo ratings yet

- Module 3 Moreno Darwin Leonardo BDocument4 pagesModule 3 Moreno Darwin Leonardo BVheronica StylesNo ratings yet

- Arc 150 Sas 7 Comprehensive Approach To HousingDocument18 pagesArc 150 Sas 7 Comprehensive Approach To HousingJhonkeneth ResolmeNo ratings yet

- PagIBIG Loan FormDocument2 pagesPagIBIG Loan FormgdlveeplNo ratings yet

- Provident Benefits Claim: Checklist of Requirements Member/ClaimantDocument4 pagesProvident Benefits Claim: Checklist of Requirements Member/ClaimantAlvin AbelloNo ratings yet

- Early Release of Gov't Employee Retirement Benefits LawDocument2 pagesEarly Release of Gov't Employee Retirement Benefits Lawhappy melsNo ratings yet

- Employee information payrollDocument6 pagesEmployee information payrollkimberly garcesNo ratings yet

- 09.19.22 TaxationDocument3 pages09.19.22 TaxationLeizzamar BayadogNo ratings yet

- Chapter 11 Compensation and BenefitsDocument43 pagesChapter 11 Compensation and BenefitsSunnieeNo ratings yet

- Staffing in the OrganizationDocument76 pagesStaffing in the OrganizationJaypee G. PolancosNo ratings yet

- 6 Basic Employee Benefits in The PhilippinesDocument7 pages6 Basic Employee Benefits in The PhilippinesgeLO36No ratings yet

- Claims - Process StepsDocument2 pagesClaims - Process StepsImelda Villareal MontarilNo ratings yet

- Pag Ibig Socialized HousingDocument31 pagesPag Ibig Socialized HousingDem Roger San PedroNo ratings yet

- Accounting For Labor CostDocument20 pagesAccounting For Labor CostDana TajedarNo ratings yet

- Invitation To Submit Offer To Purchase: Pampanga BranchDocument22 pagesInvitation To Submit Offer To Purchase: Pampanga BranchGregoria ReyesNo ratings yet