You might also like

- Schaum's Outline of Bookkeeping and Accounting, Fourth EditionFrom EverandSchaum's Outline of Bookkeeping and Accounting, Fourth EditionRating: 5 out of 5 stars5/5 (1)

- ch02 Recording Process RingkasDocument28 pagesch02 Recording Process Ringkasisma yantiNo ratings yet

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Accounting Circle PaDocument26 pagesAccounting Circle PaAisyah Ayu SaputriNo ratings yet

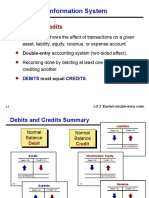

- Accounting Information System: Debits and CreditsDocument84 pagesAccounting Information System: Debits and CreditsDavid Bradley BeckNo ratings yet

- Unit 2 Accounting CycleDocument78 pagesUnit 2 Accounting Cyclemitiku kassaNo ratings yet

- Completion of The Accounting CycleDocument21 pagesCompletion of The Accounting Cyclekenshi ihsnekNo ratings yet

- Lecture TWO Accounting Fo ManagerDocument40 pagesLecture TWO Accounting Fo Managermohamed elsabahiNo ratings yet

- CH 2 Accounting CycleDocument72 pagesCH 2 Accounting CycleKirosTeklehaimanotNo ratings yet

- Chapter 2. The Recording ProcessDocument3 pagesChapter 2. The Recording ProcessÁlvaro Vacas González de EchávarriNo ratings yet

- Ch02 - THE RECORDING PROCESSDocument37 pagesCh02 - THE RECORDING PROCESSMahmud TazinNo ratings yet

- Understanding The Recording ProcessDocument36 pagesUnderstanding The Recording Processv4154l_4mirNo ratings yet

- Chapter 2Document33 pagesChapter 2Tam DoNo ratings yet

- Ifrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument49 pagesIfrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont Collegeahmed alkhajaNo ratings yet

- AbdulSamad - 12 - 16594 - 3 - CH 02 Preparation & Reporting of Financial InformationDocument57 pagesAbdulSamad - 12 - 16594 - 3 - CH 02 Preparation & Reporting of Financial InformationHassaan Qazi100% (1)

- Ch02 The Recording ProcessDocument58 pagesCh02 The Recording ProcessAndi Nisrina Nur Izza100% (1)

- Ifrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument58 pagesIfrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeTia NurhayatiNo ratings yet

- Ch.02 The Recording Process PDFDocument47 pagesCh.02 The Recording Process PDFSothcheyNo ratings yet

- Lecture 02 - Analyzing TransactionsDocument43 pagesLecture 02 - Analyzing Transactions6- Quang BáchNo ratings yet

- Chapter 2Document17 pagesChapter 2JNo ratings yet

- CH 03Document51 pagesCH 03Pham Phu Cuong B2108182No ratings yet

- Act201 Ch2 NNHDocument35 pagesAct201 Ch2 NNHTiloma M. ZannatNo ratings yet

- Act201 Ch2 NNHDocument35 pagesAct201 Ch2 NNHTiloma M. ZannatNo ratings yet

- 02 Slide Pertemuan 2Document68 pages02 Slide Pertemuan 2Dian MaulanaNo ratings yet

- The Recording Process: Accounting Principles, Ninth EditionDocument35 pagesThe Recording Process: Accounting Principles, Ninth EditionMehedi HasanNo ratings yet

- Chapter Two: Accounting Cycle For Service-Giving BusinessesDocument128 pagesChapter Two: Accounting Cycle For Service-Giving BusinessesMikias BekeleNo ratings yet

- The Accounting Information System: Learning ObjectivesDocument89 pagesThe Accounting Information System: Learning ObjectivesSunny SunnyNo ratings yet

- Chapter 3 Compelete Acct CycleDocument83 pagesChapter 3 Compelete Acct CycleSisay DeresaNo ratings yet

- Intermediate Acc Ch3Document112 pagesIntermediate Acc Ch3Dalia ElarabyNo ratings yet

- CH 02Document42 pagesCH 02fahad antalNo ratings yet

- CH 02Document42 pagesCH 02Sidra IqbalNo ratings yet

- Accountingcycle PreludeDocument49 pagesAccountingcycle PreludeIan BelmonteNo ratings yet

- IIMB Term1 PGP Chapter3Document14 pagesIIMB Term1 PGP Chapter3Arun SaktheeshNo ratings yet

- The Recording Process - Bisnis A - B 2014Document52 pagesThe Recording Process - Bisnis A - B 2014Hansel AddisonNo ratings yet

- Lecture 2 Part 1 - Recording ProcessDocument41 pagesLecture 2 Part 1 - Recording ProcessIsyraf Hatim Mohd Tamizam100% (1)

- Kieso Inter Ch03 IFRSDocument107 pagesKieso Inter Ch03 IFRSIrmaParamitaS.AfghanyNo ratings yet

- Chapter 2 PPT - UpdatedDocument58 pagesChapter 2 PPT - UpdatedmmNo ratings yet

- Chapter 2, Fundamentals of Accounting IDocument149 pagesChapter 2, Fundamentals of Accounting IMustefa UsmaelNo ratings yet

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument39 pagesPrepared by Coby Harmon University of California, Santa Barbara Westmont CollegeMahdi MohammedNo ratings yet

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument52 pagesPrepared by Coby Harmon University of California, Santa Barbara Westmont CollegeTarif Azad KhanNo ratings yet

- Financial Accounting: Tools For Business Decision-Making, Third Canadian EditionDocument6 pagesFinancial Accounting: Tools For Business Decision-Making, Third Canadian Editionapi-19743565100% (1)

- Lecture 2 Part 1 - PPTDocument42 pagesLecture 2 Part 1 - PPTOmar SanadNo ratings yet

- Ch03 Accounting Information SystemDocument56 pagesCh03 Accounting Information SystemdadiiNo ratings yet

- Ch02-Online MOduleDocument70 pagesCh02-Online MOduleNazmul Ahshan SawonNo ratings yet

- Akuntansi & Komputerisasi Akuntansi: Oleh: Dr. Zaenal Fanani, SE., MSA., AkDocument62 pagesAkuntansi & Komputerisasi Akuntansi: Oleh: Dr. Zaenal Fanani, SE., MSA., AkwuisanNo ratings yet

- Accounting Principles: Rapid ReviewDocument3 pagesAccounting Principles: Rapid ReviewAhmedNiazNo ratings yet

- Akuntansi & Komputerisasi Akuntansi: Oleh: Dr. Zaenal Fanani, SE., MSA., AkDocument63 pagesAkuntansi & Komputerisasi Akuntansi: Oleh: Dr. Zaenal Fanani, SE., MSA., AkFarrell DmNo ratings yet

- Financial Accounting: Quiz 1Document30 pagesFinancial Accounting: Quiz 1Thu Phuong NguyenNo ratings yet

- Powerpoint Chapter 3Document69 pagesPowerpoint Chapter 31234778No ratings yet

- Chapter Two The Recording Process FinalDocument35 pagesChapter Two The Recording Process Finalsolomon takeleNo ratings yet

- The Recording Process: Learning ObjectivesDocument23 pagesThe Recording Process: Learning ObjectivesSakib RafeeNo ratings yet

- CH 02Document46 pagesCH 02martinus linggoNo ratings yet

- CH 02Document37 pagesCH 02Tosuki HarisNo ratings yet

- LC Acct Chapter 2 CycleDocument97 pagesLC Acct Chapter 2 Cyclenewaybeyene5No ratings yet

- Akuntansi PerpajakanDocument63 pagesAkuntansi PerpajakanAngestika WilandariNo ratings yet

- Complete Accounting CycleDocument106 pagesComplete Accounting CycleFely MaataNo ratings yet

- The Recording ProcessDocument39 pagesThe Recording ProcessTasim IshraqueNo ratings yet

- Accounting SystemDocument53 pagesAccounting SystemdipanajnNo ratings yet

- The Recording Process: Accounting Principles, Eighth EditionDocument32 pagesThe Recording Process: Accounting Principles, Eighth EditionSourav DebnathNo ratings yet

- CIA1002 - Review of The Accounting Cycle Semester 20192020 - 1Document82 pagesCIA1002 - Review of The Accounting Cycle Semester 20192020 - 1Iman NessaNo ratings yet

- Chapter 9Document13 pagesChapter 9abdelamuzemil8No ratings yet

- FA I, Chapter 3@acfnDocument72 pagesFA I, Chapter 3@acfnabdelamuzemil8No ratings yet

- CHAPTER ONE New Service MarketingDocument17 pagesCHAPTER ONE New Service Marketingabdelamuzemil8No ratings yet

- Chapter 3 Measures of Central TendencyDocument46 pagesChapter 3 Measures of Central Tendencyabdelamuzemil8No ratings yet

- Chapter 2 Methods of Data Collection and PresentationDocument82 pagesChapter 2 Methods of Data Collection and Presentationabdelamuzemil8No ratings yet

- Social Marketing Course OutlineDocument9 pagesSocial Marketing Course Outlineabdelamuzemil8No ratings yet

- Ch-4 and Ch-5 E MarketingDocument39 pagesCh-4 and Ch-5 E Marketingabdelamuzemil8No ratings yet

- Marketing Management ?general QuestionsDocument94 pagesMarketing Management ?general Questionsabdelamuzemil8No ratings yet

- Service CHP 7 MineDocument11 pagesService CHP 7 Mineabdelamuzemil8No ratings yet

- Social Marketing All ChaptersDocument65 pagesSocial Marketing All Chaptersabdelamuzemil8No ratings yet

- Social MKTG PPT 3Document17 pagesSocial MKTG PPT 3abdelamuzemil8No ratings yet

- CH-6 E MarketingDocument17 pagesCH-6 E Marketingabdelamuzemil8No ratings yet

- Social MKT Degr Ppt3Document23 pagesSocial MKT Degr Ppt3abdelamuzemil8No ratings yet

- Reaction Paper ElasticityDocument2 pagesReaction Paper Elasticityelizabeth_cruz_53100% (1)

- Monmouth Student Template UpdatedDocument14 pagesMonmouth Student Template Updatedhao pengNo ratings yet

- f5 SQB 15 Sample PDFDocument51 pagesf5 SQB 15 Sample PDFCecilia Mfene Sekubuwane0% (1)

- EconomicsDocument10 pagesEconomicsAbhinav Chauhan50% (2)

- DR Lal Pathlabs LTD - Samplestudy - ElearnMarketDocument33 pagesDR Lal Pathlabs LTD - Samplestudy - ElearnMarketNarendraDugarNo ratings yet

- Course SyllabusDocument11 pagesCourse SyllabusLiwayNo ratings yet

- ChapterI Introduction To Economics 1Document37 pagesChapterI Introduction To Economics 1VirencarpediemNo ratings yet

- Royal AholdDocument13 pagesRoyal AholdgayatrichaudharyNo ratings yet

- Berger PaintsDocument18 pagesBerger PaintsPaul GeorgeNo ratings yet

- Business Valuations: Net Asset Value (Nav)Document9 pagesBusiness Valuations: Net Asset Value (Nav)Artwell ZuluNo ratings yet

- CCH Test BankDocument41 pagesCCH Test Bankdoug1190% (8)

- Aso SyllabusDocument5 pagesAso SyllabusMuniNo ratings yet

- Afscme Works Fall 2011Document32 pagesAfscme Works Fall 2011local1086100% (1)

- MercedesDocument138 pagesMercedesMihaela DavidoaiaNo ratings yet

- City Government of San Pablo V ReyesDocument2 pagesCity Government of San Pablo V ReyesNikita BayotNo ratings yet

- Concierge Service Business PlanDocument35 pagesConcierge Service Business PlanTamer KhattabNo ratings yet

- A Project Report On Analysis of Financial Statement of ICICI Bank LimitedDocument5 pagesA Project Report On Analysis of Financial Statement of ICICI Bank Limitedhandsomedevil1990No ratings yet

- Cross Border Tax LeasingDocument4 pagesCross Border Tax LeasingDuncan_Low_4659No ratings yet

- Matapang Computer Repairs Journal Entries For The Month Ended February 29,2016 Date Account Title & Explanation Debit CreditDocument4 pagesMatapang Computer Repairs Journal Entries For The Month Ended February 29,2016 Date Account Title & Explanation Debit CreditAaroneZulueta50% (4)

- 2113T Feasibility Study TempateDocument27 pages2113T Feasibility Study TempateRA MagallanesNo ratings yet

- Gul Ahmed ReportDocument1 pageGul Ahmed ReportfahadaijazNo ratings yet

- IAS 17 LeaseDocument7 pagesIAS 17 LeaseMaqsoodNo ratings yet

- CIR vs. Cebu Portland Cement Company and CTA, G.R. No. L-29059, December 15, 1987Document6 pagesCIR vs. Cebu Portland Cement Company and CTA, G.R. No. L-29059, December 15, 1987Emil BautistaNo ratings yet

- Non Current AssetsDocument44 pagesNon Current AssetsSandee Angeli Maceda Villarta100% (1)

- Transfer PricingDocument19 pagesTransfer PricingamanNo ratings yet

- AllGreen AR 2010Document135 pagesAllGreen AR 2010Yeong Chiang TanNo ratings yet

- LBO PowerpointDocument36 pagesLBO Powerpointfalarkys100% (1)

- Pre-Feasibility Study: Tea CompanyDocument20 pagesPre-Feasibility Study: Tea CompanyIPro PkNo ratings yet

- Income Taxation (Principles of Taxation) : Fritz A. Perez, Cpa, CTT, Mritax, Mba (O.G)Document40 pagesIncome Taxation (Principles of Taxation) : Fritz A. Perez, Cpa, CTT, Mritax, Mba (O.G)JessaNo ratings yet

- Costacctg13 SolPPT ch02Document18 pagesCostacctg13 SolPPT ch02eriski_1100% (2)