You might also like

- Accounting NotesDocument66 pagesAccounting NotesShashank Gadia71% (17)

- Finance DefinitionsDocument17 pagesFinance DefinitionsvigneshNo ratings yet

- Audit of Income and Expenditure Account 1.1Document27 pagesAudit of Income and Expenditure Account 1.1Akshata Masurkar100% (1)

- The Accounting Process: Adjusting The Accounts Cash Versus Accrual Basis of AccountingDocument12 pagesThe Accounting Process: Adjusting The Accounts Cash Versus Accrual Basis of AccountingKim Patrick Victoria100% (1)

- 1587226653unit 4, Cost Accounting, Sem4Document5 pages1587226653unit 4, Cost Accounting, Sem4Sanjukta Das100% (1)

- Accounting Basics 1Document3 pagesAccounting Basics 1Irene the Fire CatNo ratings yet

- Cost Accounting 1-7 Lessons PDFDocument130 pagesCost Accounting 1-7 Lessons PDFRupak ChandnaNo ratings yet

- Unit V Reconciliation of Cost and Financial AccountingDocument10 pagesUnit V Reconciliation of Cost and Financial AccountingDrJay DaveNo ratings yet

- Acc. 101-True or False and IdentificationDocument9 pagesAcc. 101-True or False and IdentificationAuroraNo ratings yet

- SM-2 - Lesson - 1 To 7 in EnglishDocument128 pagesSM-2 - Lesson - 1 To 7 in EnglishMayank RajputNo ratings yet

- Cost Accounting Vol-IDocument48 pagesCost Accounting Vol-ImanoNo ratings yet

- Adjusting Entries HandoutsDocument12 pagesAdjusting Entries HandoutsKim Patrick VictoriaNo ratings yet

- Objects of Using Accounting Information IncludeDocument2 pagesObjects of Using Accounting Information IncludeTrí NguyễnNo ratings yet

- Acc NotesDocument1 pageAcc NotesBenjaminNo ratings yet

- Explain The Difference Between Sales Revenue and Net Sales. Sales RevenueDocument3 pagesExplain The Difference Between Sales Revenue and Net Sales. Sales RevenueHuda waseemNo ratings yet

- What Is The Difference Between Job Costing and Process Costing?Document31 pagesWhat Is The Difference Between Job Costing and Process Costing?Muhammad AsimNo ratings yet

- Meaning of Cost Reconciliation StatementDocument5 pagesMeaning of Cost Reconciliation StatementmahendrabpatelNo ratings yet

- Reconciliation of Cost & Financial AccountsDocument13 pagesReconciliation of Cost & Financial AccountsRahulNo ratings yet

- FABM2-Chapter 2Document31 pagesFABM2-Chapter 2Marjon GarabelNo ratings yet

- ReconciliationDocument7 pagesReconciliationHemant bhanawatNo ratings yet

- Tugas Resume Chapter 2 Dan Chapter 3Document3 pagesTugas Resume Chapter 2 Dan Chapter 3sri wahyuniNo ratings yet

- Quiz 5 MidtermDocument3 pagesQuiz 5 Midtermdanica gomez100% (1)

- Glossary of AccountingDocument8 pagesGlossary of AccountingSarbuland Khan LodhiNo ratings yet

- Questions and AnswersDocument27 pagesQuestions and AnswersAmalia BejenariuNo ratings yet

- Afm Mod 2Document4 pagesAfm Mod 2Manas MohapatraNo ratings yet

- Account Titles and ExplanationDocument4 pagesAccount Titles and ExplanationKaye VillaflorNo ratings yet

- StarFarm Finance OfficerDocument7 pagesStarFarm Finance OfficerZany KhanNo ratings yet

- Econ 303Document5 pagesEcon 303ali abou aliNo ratings yet

- Glossary of Terms For FA2 and MA2 AmendedDocument12 pagesGlossary of Terms For FA2 and MA2 AmendedS RaihanNo ratings yet

- Financial AnalysisDocument22 pagesFinancial Analysisnomaan khanNo ratings yet

- Accounting Terms and DefinitionsDocument120 pagesAccounting Terms and DefinitionsYellow BelleNo ratings yet

- Accenture - 1 B Com ProfileDocument7 pagesAccenture - 1 B Com ProfileTHIMMAIAH B CNo ratings yet

- Note On End of The YearDocument5 pagesNote On End of The YearojimawilliamsNo ratings yet

- Accounting Terminology GuideDocument133 pagesAccounting Terminology Guidetony25252000No ratings yet

- Lesson 3: Basic Accounting: Completing The Accounting Cycle Adjusting The AccountsDocument18 pagesLesson 3: Basic Accounting: Completing The Accounting Cycle Adjusting The AccountsAra ArinqueNo ratings yet

- Allowance For Bad Debts: Allowance Method Direct Write-Off MethodDocument5 pagesAllowance For Bad Debts: Allowance Method Direct Write-Off MethodChandradhari JhaNo ratings yet

- A Primer On Financial StatementsDocument11 pagesA Primer On Financial StatementsPranay NarayaniNo ratings yet

- Understated or OverstatedDocument1 pageUnderstated or OverstatedJaimee CruzNo ratings yet

- Financial and Economic TermsDocument4 pagesFinancial and Economic TermsShaggy DuraiNo ratings yet

- Unit 11 Reconciliation of Cost Financial: AccountsDocument18 pagesUnit 11 Reconciliation of Cost Financial: AccountsDrJay DaveNo ratings yet

- Accounting DocumentsDocument6 pagesAccounting DocumentsMae AroganteNo ratings yet

- Introduction To Social MediaDocument176 pagesIntroduction To Social MediaLiiNo ratings yet

- Acc Imp Points 2Document10 pagesAcc Imp Points 2AnilisaNo ratings yet

- Accounting Terms & DefinitionsDocument6 pagesAccounting Terms & DefinitionsMir Wajid KhanNo ratings yet

- CHAPTER 2-Statement of Comprehensive IncomeDocument4 pagesCHAPTER 2-Statement of Comprehensive IncomeDan GalvezNo ratings yet

- Full Disclosure PrincipleDocument7 pagesFull Disclosure PrincipleVirgo CruzNo ratings yet

- Prepare Basic Financial StatementsDocument6 pagesPrepare Basic Financial StatementsMujieh NkengNo ratings yet

- Analysis of Trial Balance-: Solution 2Document3 pagesAnalysis of Trial Balance-: Solution 2BUNTY GUPTANo ratings yet

- IMP Abt Oracle FinancialsDocument12 pagesIMP Abt Oracle FinancialsRohit DaswaniNo ratings yet

- Book Keeping TheoryDocument16 pagesBook Keeping TheoryamitNo ratings yet

- Account DefinationsDocument7 pagesAccount DefinationsManasa GuduruNo ratings yet

- Chapter 5 Financial StatementsDocument8 pagesChapter 5 Financial StatementshwhwhwhjiiiNo ratings yet

- Deferred Charge: DEFINITION of 'Regulatory Asset'Document6 pagesDeferred Charge: DEFINITION of 'Regulatory Asset'Joie CruzNo ratings yet

- Unit - 1 - FIN ACCDocument7 pagesUnit - 1 - FIN ACCTif ShawNo ratings yet

- Finals ReviewerDocument5 pagesFinals ReviewerGaia BautistaNo ratings yet

- 9 Non-Integrated AccountsDocument12 pages9 Non-Integrated Accountscsgurpreet100% (1)

- Statement of Comprehensive IncomeDocument42 pagesStatement of Comprehensive IncomeClove WallNo ratings yet

- 3Document1 page3Sara AlnahdiNo ratings yet

- Costing Ledger Control AccountDocument6 pagesCosting Ledger Control AccountHelen MoyoNo ratings yet

- 2211posting 061cab6e3d56f89 03363994Document12 pages2211posting 061cab6e3d56f89 03363994Saleh RaoufNo ratings yet

- Arens Aas17 PPT 24Document53 pagesArens Aas17 PPT 24Saleh RaoufNo ratings yet

- Lecture8 Cost AccountingDocument8 pagesLecture8 Cost AccountingSaleh RaoufNo ratings yet

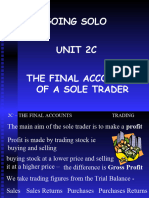

- Final Accounts - 2CDocument8 pagesFinal Accounts - 2CSaleh RaoufNo ratings yet

- CompaniesDocument39 pagesCompaniesSaleh RaoufNo ratings yet

- Lecture7 Cost AccountingDocument9 pagesLecture7 Cost AccountingSaleh RaoufNo ratings yet

- Auditing Chapter (1) - Four Part 2023Document12 pagesAuditing Chapter (1) - Four Part 2023Saleh RaoufNo ratings yet

- Macabacus Fundamentals Demo - BlankDocument16 pagesMacabacus Fundamentals Demo - BlankSaleh Raouf100% (1)

- Proofing DemoDocument2 pagesProofing DemoSaleh RaoufNo ratings yet

- Auditing Chapter (1) Three Part 2023Document22 pagesAuditing Chapter (1) Three Part 2023Saleh RaoufNo ratings yet

- CH 14Document6 pagesCH 14Saleh RaoufNo ratings yet

- Auditing LectureDocument13 pagesAuditing LectureSaleh RaoufNo ratings yet

- Auditing Chapter (1) - Second Part 2023Document10 pagesAuditing Chapter (1) - Second Part 2023Saleh RaoufNo ratings yet

- CIB Practice Numerical Reasoning Test SolutionDocument22 pagesCIB Practice Numerical Reasoning Test SolutionSaleh RaoufNo ratings yet

- Auditing Chapter (1) First Part 2023Document26 pagesAuditing Chapter (1) First Part 2023Saleh RaoufNo ratings yet

- B Exercises: E24-1B (Post-Balance-Sheet Events) (A) (B)Document4 pagesB Exercises: E24-1B (Post-Balance-Sheet Events) (A) (B)Saleh RaoufNo ratings yet

- CH 20Document8 pagesCH 20Saleh RaoufNo ratings yet

- Macabacus Fundamentals Demo - BlankDocument16 pagesMacabacus Fundamentals Demo - BlankSaleh Raouf100% (1)

- Lesson 1: Learning ObjectivesDocument7 pagesLesson 1: Learning ObjectivesSaleh RaoufNo ratings yet

- CH 21Document6 pagesCH 21Saleh RaoufNo ratings yet

- CH 22Document8 pagesCH 22Saleh RaoufNo ratings yet

- CH 23Document8 pagesCH 23Saleh RaoufNo ratings yet

- CH 06Document4 pagesCH 06Saleh RaoufNo ratings yet

- CH 19Document8 pagesCH 19Saleh RaoufNo ratings yet

- CH 16Document8 pagesCH 16Saleh RaoufNo ratings yet

- CH 15Document8 pagesCH 15Saleh RaoufNo ratings yet

- B Exercises: E3-1B (Transaction Analysis-Service Company)Document8 pagesB Exercises: E3-1B (Transaction Analysis-Service Company)Saleh RaoufNo ratings yet

- CH 11Document6 pagesCH 11Saleh RaoufNo ratings yet

- CH 13Document6 pagesCH 13Saleh RaoufNo ratings yet

- CH 07Document8 pagesCH 07Saleh RaoufNo ratings yet