You might also like

- Pro Forma COP - Open Pit - 0Document101 pagesPro Forma COP - Open Pit - 0Gurinder ParmarNo ratings yet

- Splitting The Roles of CEO and ChairmanDocument2 pagesSplitting The Roles of CEO and Chairmanmelrandal7No ratings yet

- Bylaws of CorporationDocument9 pagesBylaws of CorporationAboromo LimotoNo ratings yet

- Compelling Returns: A Practical Guide to Socially Responsible InvestingFrom EverandCompelling Returns: A Practical Guide to Socially Responsible InvestingNo ratings yet

- Pro Forma Models - StudentsDocument9 pagesPro Forma Models - Studentsshanker23scribd100% (1)

- IC Pro Forma Balance Sheets Template 10510Document4 pagesIC Pro Forma Balance Sheets Template 10510Royd BeñasNo ratings yet

- Forms of Business OwnershipDocument23 pagesForms of Business OwnershipPhoebe Dangel100% (1)

- Cedi Sika Investment Club ProspectusDocument16 pagesCedi Sika Investment Club ProspectusIsaac Dwimoh-OpokuNo ratings yet

- First Round Capital Slide Deck PDFDocument10 pagesFirst Round Capital Slide Deck PDFEmily StanfordNo ratings yet

- Corporate Turnaround TheoryDocument4 pagesCorporate Turnaround TheoryabeeraNo ratings yet

- Private Equity Unchained: Strategy Insights for the Institutional InvestorFrom EverandPrivate Equity Unchained: Strategy Insights for the Institutional InvestorNo ratings yet

- The Growing Importance of Fund Governance - ILPA Principles and BeyondDocument3 pagesThe Growing Importance of Fund Governance - ILPA Principles and BeyondErin GriffithNo ratings yet

- Investment Banking, Equity Research, Valuation Interview Handpicked Questions and AnswerDocument17 pagesInvestment Banking, Equity Research, Valuation Interview Handpicked Questions and AnswerStudy FreakNo ratings yet

- Social Impact Bond CaseDocument21 pagesSocial Impact Bond CaseTest123No ratings yet

- Term Sheet: NBAD GCC Opportunities Fund (AJAJ)Document12 pagesTerm Sheet: NBAD GCC Opportunities Fund (AJAJ)gaceorNo ratings yet

- SERIES 24 EXAM STUDY GUIDE 2021 + TEST BANKFrom EverandSERIES 24 EXAM STUDY GUIDE 2021 + TEST BANKNo ratings yet

- Corporate Governance OverviewDocument16 pagesCorporate Governance OverviewBie RenNo ratings yet

- Best Execution and Client Order Handling PolicyDocument6 pagesBest Execution and Client Order Handling PolicyLiliko Shergelashvili100% (1)

- Dissertation - Socially Responsible Investment in Indonesia-1Document70 pagesDissertation - Socially Responsible Investment in Indonesia-1Riani LaurensiaNo ratings yet

- Sweeney P 2007 Forensic AccountingDocument5 pagesSweeney P 2007 Forensic AccountingbobNo ratings yet

- Pro Forma StatementDocument14 pagesPro Forma StatementEse Peace100% (1)

- Pro Forma Balance Sheet Template: Company NameDocument5 pagesPro Forma Balance Sheet Template: Company NamePhương ĐinhNo ratings yet

- Managing Financial Resources and DecisionsDocument11 pagesManaging Financial Resources and DecisionsangelomercedeblogNo ratings yet

- Control Environment Tone at The Top and EthicsDocument57 pagesControl Environment Tone at The Top and EthicstechcertNo ratings yet

- HNA Investment Fund Slide Deck Draft 1Document54 pagesHNA Investment Fund Slide Deck Draft 1WentNo ratings yet

- Quality of EarningsDocument8 pagesQuality of EarningsOlsjon BaxhijaNo ratings yet

- Defenses Against Hostile TakeoversDocument30 pagesDefenses Against Hostile TakeoversNeerav SharmaNo ratings yet

- Sample Term Sheet: Series A Convertible Preferred Stock FinancingDocument2 pagesSample Term Sheet: Series A Convertible Preferred Stock FinancingJennifer LeeNo ratings yet

- Basic Understanding of Financial Investment, Book 6- For Teens and Young AdultsFrom EverandBasic Understanding of Financial Investment, Book 6- For Teens and Young AdultsNo ratings yet

- l9 Credit Derivatives 2011Document51 pagesl9 Credit Derivatives 2011vladanNo ratings yet

- CH 3 - The Problems With Conventional AccountingDocument52 pagesCH 3 - The Problems With Conventional AccountingCondro TriharyonoNo ratings yet

- Amy Domini - Socially Responsible Investing - Making A Difference and Making Money-Kaplan Business (2001)Document317 pagesAmy Domini - Socially Responsible Investing - Making A Difference and Making Money-Kaplan Business (2001)DaviSilva0% (1)

- 17 Best Investment Vehicles For Filipinos - 1Document58 pages17 Best Investment Vehicles For Filipinos - 1Jewelyn CioconNo ratings yet

- ASEAN Corporate Governance Scorecard Country Reports and Assessments 2019From EverandASEAN Corporate Governance Scorecard Country Reports and Assessments 2019No ratings yet

- Investor Exit StrategyDocument11 pagesInvestor Exit Strategypaul5463No ratings yet

- Investment Policy StatementDocument14 pagesInvestment Policy StatementHamis Rabiam MagundaNo ratings yet

- The Hampshire College Report On Socially Responsible Investment (1983)Document119 pagesThe Hampshire College Report On Socially Responsible Investment (1983)DLTooleyNo ratings yet

- Legal Aspects of M&ADocument1 pageLegal Aspects of M&AGeetika Patney0% (1)

- Role of Institutional Investors in Corporate GovernanceDocument17 pagesRole of Institutional Investors in Corporate GovernanceRaj KumarNo ratings yet

- CMA PrivatizationDocument4 pagesCMA PrivatizationInvest StockNo ratings yet

- Advantages and Disadvantages of An IPODocument2 pagesAdvantages and Disadvantages of An IPOHemali100% (1)

- Corporate Governance Lectures 1Document29 pagesCorporate Governance Lectures 1RewardMaturureNo ratings yet

- Corporate Behavioural Finance Chap06Document14 pagesCorporate Behavioural Finance Chap06zeeshanshanNo ratings yet

- 8.corporate ReorganizationDocument2 pages8.corporate ReorganizationMuhammad Usman Ashraf100% (1)

- Private Equity Fund Study PDFDocument237 pagesPrivate Equity Fund Study PDFprasan gudeNo ratings yet

- Listing Procedure and IPO ProcessDocument27 pagesListing Procedure and IPO ProcessJade EdajNo ratings yet

- Lbo Model Short FormDocument4 pagesLbo Model Short FormAkash PrasadNo ratings yet

- BitShares White PaperDocument18 pagesBitShares White PaperMichael WebbNo ratings yet

- Cogent Analytics M&A ManualDocument19 pagesCogent Analytics M&A Manualvan070100% (1)

- Hostile TakeoverDocument15 pagesHostile TakeoverKiran MankodiNo ratings yet

- Wage FixationDocument6 pagesWage FixationDurga Prasad Dash25% (4)

- Job Evaluting 2Document3 pagesJob Evaluting 2Durga Prasad Dash100% (1)

- Wage Determination in IndiaDocument3 pagesWage Determination in IndiaDurga Prasad Dash86% (7)

- Trade Union 2Document8 pagesTrade Union 2Durga Prasad Dash100% (1)

- Wage DifferentialDocument3 pagesWage DifferentialDurga Prasad Dash100% (4)

- Emerging Trends in HRMDocument3 pagesEmerging Trends in HRMDurga Prasad DashNo ratings yet

- Definition of Job EvaluationDocument4 pagesDefinition of Job EvaluationDurga Prasad DashNo ratings yet

- Theory of Trade UnionDocument3 pagesTheory of Trade UnionDurga Prasad Dash100% (1)

- Recognition of Trade UnionDocument6 pagesRecognition of Trade UnionDurga Prasad DashNo ratings yet

- Industrial RelationsDocument12 pagesIndustrial RelationsDurga Prasad Dash100% (2)

- Economic Environment ofDocument5 pagesEconomic Environment ofDurga Prasad DashNo ratings yet

- National Income123Document15 pagesNational Income123Durga Prasad DashNo ratings yet

- Collective BargainingDocument10 pagesCollective BargainingDurga Prasad Dash100% (2)

- Performance Mgt.Document26 pagesPerformance Mgt.Durga Prasad DashNo ratings yet

- National IncomeDocument10 pagesNational IncomeDurga Prasad DashNo ratings yet

- Analyzing Performance ProblemDocument14 pagesAnalyzing Performance ProblemDurga Prasad DashNo ratings yet

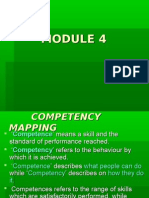

- Module 4Document17 pagesModule 4Durga Prasad DashNo ratings yet

- Economic Environment OF BusinessDocument5 pagesEconomic Environment OF BusinessDurga Prasad DashNo ratings yet

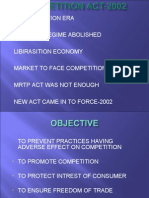

- Globolisation Era Control Regime Abolished Libirasition Economy Market To Face Competition MRTP Act Was Not Enough New Act Came in To Force-2002Document12 pagesGlobolisation Era Control Regime Abolished Libirasition Economy Market To Face Competition MRTP Act Was Not Enough New Act Came in To Force-2002Durga Prasad DashNo ratings yet

- Competition CommDocument5 pagesCompetition CommDurga Prasad DashNo ratings yet

- Service RecoveryDocument22 pagesService RecoveryDurga Prasad Dash100% (1)

- SERVQUAL - Measuring Service QualityDocument18 pagesSERVQUAL - Measuring Service QualityDurga Prasad DashNo ratings yet

- Strategic Marketing Decisions and ChoicesDocument18 pagesStrategic Marketing Decisions and ChoicesDurga Prasad DashNo ratings yet

- Service Quality FINALDocument28 pagesService Quality FINALDurga Prasad DashNo ratings yet

- 6 Cathay vs. VazquezDocument2 pages6 Cathay vs. VazquezErwin BernardinoNo ratings yet

- Flex Li3 21 VAADocument1 pageFlex Li3 21 VAAAyman Al-YafeaiNo ratings yet

- Vodafone Idea MergerDocument20 pagesVodafone Idea MergerCyvita Veigas100% (1)

- Natural Wonders of The World: I:GrammarDocument8 pagesNatural Wonders of The World: I:GrammarNhị NguyễnNo ratings yet

- Events ProposalsDocument19 pagesEvents ProposalsRam-tech Jackolito FernandezNo ratings yet

- Comics Trip MasterpiecesDocument16 pagesComics Trip MasterpiecesDaniel Constantine100% (2)

- Chen, Y.-K., Shen, C.-H., Kao, L., & Yeh, C. Y. (2018) .Document40 pagesChen, Y.-K., Shen, C.-H., Kao, L., & Yeh, C. Y. (2018) .Vita NataliaNo ratings yet

- Influence of Brand Experience On CustomerDocument16 pagesInfluence of Brand Experience On Customerarif adrianNo ratings yet

- MCQ Class VDocument9 pagesMCQ Class VSneh MahajanNo ratings yet

- Course Welcome and Overview ACADocument20 pagesCourse Welcome and Overview ACAAlmerNo ratings yet

- A Psychological Crusade by Fernando Sorrentino - Text 7Document2 pagesA Psychological Crusade by Fernando Sorrentino - Text 7Donnie DominguezNo ratings yet

- MKT305 (Module 6 Segmentation)Document53 pagesMKT305 (Module 6 Segmentation)Ngọc AnhhNo ratings yet

- H.P. Elementary Education Code Chapter - 4 - 2012 SMC by Vijay Kumar HeerDocument7 pagesH.P. Elementary Education Code Chapter - 4 - 2012 SMC by Vijay Kumar HeerVIJAY KUMAR HEERNo ratings yet

- Yeb2019 Template MhayDocument9 pagesYeb2019 Template MhayloretaNo ratings yet

- Q. 15 Insurance Regulatory and Development AuthorityDocument2 pagesQ. 15 Insurance Regulatory and Development AuthorityMAHENDRA SHIVAJI DHENAKNo ratings yet

- The Honey Gatherers - Travels With The Bauls - The Wandering Minstrels of Rural India - Mimlu Sen PDFDocument16 pagesThe Honey Gatherers - Travels With The Bauls - The Wandering Minstrels of Rural India - Mimlu Sen PDFAurko F AhmadNo ratings yet

- Bibliografia Antenas y RadioDocument3 pagesBibliografia Antenas y RadioJorge HerreraNo ratings yet

- Narrative Report PatternDocument2 pagesNarrative Report PatternAngelo DomingoNo ratings yet

- Coin Operated Short Movie AnalysisDocument17 pagesCoin Operated Short Movie AnalysisA 29 Nathaniela Devany MiramaNo ratings yet

- Fig. 6.14 Circular WaveguideDocument16 pagesFig. 6.14 Circular WaveguideThiagu RajivNo ratings yet

- Camp High Harbour at Lake LanierDocument3 pagesCamp High Harbour at Lake LaniermetroatlantaymcaNo ratings yet

- 5130 - 05 5G Industrial Applications and SolutionsDocument113 pages5130 - 05 5G Industrial Applications and SolutionsMauricio SantosNo ratings yet

- ShowBoats International (May 2016)Document186 pagesShowBoats International (May 2016)LelosPinelos123100% (1)

- CJ1W-PRT21 PROFIBUS-DP Slave Unit: Operation ManualDocument100 pagesCJ1W-PRT21 PROFIBUS-DP Slave Unit: Operation ManualSergio Eu CaNo ratings yet

- Righeimer ComplaintDocument45 pagesRigheimer ComplaintSarah BatchaNo ratings yet

- Siy Cong Bien Vs HSBCDocument2 pagesSiy Cong Bien Vs HSBCMJ Decolongon100% (1)

- Juzaili Alias SSB Jadual Perubahan PDP Dan Penilaian AlternatifDocument1 pageJuzaili Alias SSB Jadual Perubahan PDP Dan Penilaian Alternatifkar afiNo ratings yet

- Assignment 1684490923Document16 pagesAssignment 1684490923neha.engg45755No ratings yet

- Fin - e - 178 - 2022-Covid AusterityDocument8 pagesFin - e - 178 - 2022-Covid AusterityMARUTHUPANDINo ratings yet

- Question Paper Code:: (10×2 20 Marks)Document2 pagesQuestion Paper Code:: (10×2 20 Marks)Umesh Harihara sudan0% (1)