You might also like

- Ebay - Profit Tracking SpreadsheetDocument6 pagesEbay - Profit Tracking SpreadsheetSuzanne WellsNo ratings yet

- Materials Management Materials Management Materials Management Materials ManagementDocument19 pagesMaterials Management Materials Management Materials Management Materials ManagementMuralidhar DasariNo ratings yet

- Ballou Logistics Solved Problems Chapter 13Document42 pagesBallou Logistics Solved Problems Chapter 13RenTahL60% (5)

- Accounting Gov ReviewerDocument19 pagesAccounting Gov ReviewerAira Jaimee GonzalesNo ratings yet

- Guide to Japan-born Inventory and Accounts Receivable Freshness Control for Managers 2017From EverandGuide to Japan-born Inventory and Accounts Receivable Freshness Control for Managers 2017No ratings yet

- Accounting For Merchandising OperationsDocument31 pagesAccounting For Merchandising OperationsBülent Kılıç100% (1)

- Inventory Accounting: A Comprehensive GuideFrom EverandInventory Accounting: A Comprehensive GuideRating: 5 out of 5 stars5/5 (1)

- Chapter 8 Valuation of InventoriesDocument39 pagesChapter 8 Valuation of InventoriesMichelle Joy Nuyad-Pantinople100% (1)

- Inventories Valuation ConceptDocument13 pagesInventories Valuation ConceptSumit SahuNo ratings yet

- Comparative Ratio Analysis of Britannia Industries and Nestle IndiaDocument46 pagesComparative Ratio Analysis of Britannia Industries and Nestle Indiasafwan100% (4)

- Backflush CostingDocument7 pagesBackflush Costingsharminhoque100% (4)

- Abc Ved Analysis-Inventory ManagementDocument28 pagesAbc Ved Analysis-Inventory ManagementarunNo ratings yet

- InventoryDocument65 pagesInventoryArunkumar KalyanasundaramNo ratings yet

- Intermediate Financial Accounting I: Inventories: MeasurementDocument89 pagesIntermediate Financial Accounting I: Inventories: MeasurementDaphne BlakeNo ratings yet

- Lecture 4. StockDocument26 pagesLecture 4. StockazizbektokhirbekovNo ratings yet

- Backflush Accounting 1Document9 pagesBackflush Accounting 1Ai Lin ChenNo ratings yet

- 3 Resource Backflush AccountingDocument7 pages3 Resource Backflush AccountingNaveed Mughal AcmaNo ratings yet

- Merchandising Periodic SampleDocument14 pagesMerchandising Periodic SampleYam Pinoy100% (2)

- 100 Chap 6Document65 pages100 Chap 6RishiShuklaNo ratings yet

- IAS 2 - InventoriesDocument42 pagesIAS 2 - Inventorieswakemeup143100% (1)

- 3 Resource Backflush AccountingDocument7 pages3 Resource Backflush Accountingsanits591No ratings yet

- Inventory ManagementDocument22 pagesInventory ManagementYolowii XanaNo ratings yet

- Chapter 1 InventoryDocument12 pagesChapter 1 InventoryDaniel AssefsNo ratings yet

- P2 - New Ch2Document10 pagesP2 - New Ch2mulugetaNo ratings yet

- Lecture13 Accounting For Inventory&ContractWIP 12 13 BBDocument35 pagesLecture13 Accounting For Inventory&ContractWIP 12 13 BBHappy AdelaNo ratings yet

- Inventory Valuation (Ias 2)Document30 pagesInventory Valuation (Ias 2)Patric CletusNo ratings yet

- Accounting Indonesia Adaptation 4 TH Edition: - Volume 1Document51 pagesAccounting Indonesia Adaptation 4 TH Edition: - Volume 1Aura -No ratings yet

- PPAcct II InventoryDocument9 pagesPPAcct II InventoryNigussie BerhanuNo ratings yet

- POA1-Assignment - Chapter 6 - Q SentDocument6 pagesPOA1-Assignment - Chapter 6 - Q SentYusniagita EkadityaNo ratings yet

- Inventory Management: Presented By: Apple MagpantayDocument31 pagesInventory Management: Presented By: Apple MagpantayRuth Ann DimalaluanNo ratings yet

- Exercise 1 - Inventory ManagementDocument3 pagesExercise 1 - Inventory ManagementChristian BalanquitNo ratings yet

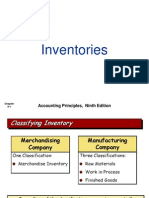

- Inventories: Accounting Principles, Ninth EditionDocument48 pagesInventories: Accounting Principles, Ninth Editionpiash246No ratings yet

- Inventory ValuationDocument19 pagesInventory ValuationJohn Patterson100% (1)

- Financial Accounting Mid Term ExamDocument4 pagesFinancial Accounting Mid Term ExamMamoonah HassanNo ratings yet

- Kelompok 6 Chapter 6Document11 pagesKelompok 6 Chapter 6leoni pannaNo ratings yet

- Inventory LastDocument27 pagesInventory LastNigus AyeleNo ratings yet

- A2 Sample Chapter Inventory ValuationDocument19 pagesA2 Sample Chapter Inventory ValuationIlmi Dewi ANo ratings yet

- Test Chapter 8 Principles Sample TestDocument9 pagesTest Chapter 8 Principles Sample TestJacob WagenknechtNo ratings yet

- SCR SwotDocument6 pagesSCR SwotamitguptaujjNo ratings yet

- CH 06 SMDocument94 pagesCH 06 SMapi-234680678No ratings yet

- Ch06. TranslationDocument56 pagesCh06. TranslationNaviaNo ratings yet

- Act 201 Chapter 6Document36 pagesAct 201 Chapter 6Amir HossainNo ratings yet

- Unit 2Document30 pagesUnit 2yebegashet100% (1)

- Inventory Accounting and ValuationDocument4 pagesInventory Accounting and ValuationFathi Salem Mohammed Abdullah100% (1)

- 1.1. Inventory Costing Methods Under A Periodic SystemDocument6 pages1.1. Inventory Costing Methods Under A Periodic Systembeth elNo ratings yet

- 1 Lecture Financial Statements Is and BSDocument60 pages1 Lecture Financial Statements Is and BSby Scribd100% (1)

- Advanced Accounting Unit 2Document15 pagesAdvanced Accounting Unit 2yasinNo ratings yet

- Accounting English IIDocument14 pagesAccounting English IIJaprax LailyasNo ratings yet

- Inventory AccDocument15 pagesInventory Accnewaybeyene5No ratings yet

- HWChap 006Document67 pagesHWChap 006hellooceanNo ratings yet

- Chap015.ppt Independent-Demand InventoryDocument44 pagesChap015.ppt Independent-Demand InventorySaad Khadur Eilyes100% (1)

- ACC213 ReviewerDocument6 pagesACC213 ReviewerSHAZ NAY GULAYNo ratings yet

- Paper - 4: Cost Accounting and Financial Management All Questions Are CompulsoryDocument24 pagesPaper - 4: Cost Accounting and Financial Management All Questions Are CompulsoryAkela FatimaNo ratings yet

- Inventory Records CHA 1Document10 pagesInventory Records CHA 1cherinetNo ratings yet

- Chapter 06 - InventoriesDocument57 pagesChapter 06 - InventoriesDrake AdamNo ratings yet

- Unit 2: Inventories: Special Valuation Methods 2.0 Aims and ObjectivesDocument17 pagesUnit 2: Inventories: Special Valuation Methods 2.0 Aims and ObjectivesNesru SirajNo ratings yet

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument66 pagesPrepared by Coby Harmon University of California, Santa Barbara Westmont CollegenaeemakhtaracmaNo ratings yet

- Summary After MidDocument40 pagesSummary After Midmc2hin9No ratings yet

- TQ Ans Wk9 2016Document10 pagesTQ Ans Wk9 2016seling97No ratings yet

- Exam - Chapter 006Document19 pagesExam - Chapter 006abdullahsikander4237No ratings yet

- Inventories - Inventory Estimation MethodsDocument17 pagesInventories - Inventory Estimation MethodsmarkNo ratings yet

- Guide to Japan-born Inventory and Accounts Receivable Freshness Control for managersFrom EverandGuide to Japan-born Inventory and Accounts Receivable Freshness Control for managersNo ratings yet

- Guide to Japan-born Inventory and Accounts Receivable Freshness Control for Managers: English versionFrom EverandGuide to Japan-born Inventory and Accounts Receivable Freshness Control for Managers: English versionNo ratings yet

- Guide to Japan-Born Inventory and Accounts Receivable Freshness Control for Managers 2017 (English Version)From EverandGuide to Japan-Born Inventory and Accounts Receivable Freshness Control for Managers 2017 (English Version)No ratings yet

- Final Internship ReportDocument10 pagesFinal Internship ReportMaryam NisarNo ratings yet

- Perpetual System, Problem #17Document2 pagesPerpetual System, Problem #17Feiya LiuNo ratings yet

- Etengine-Erp Techno-Functional Information: ContentDocument14 pagesEtengine-Erp Techno-Functional Information: ContentHarshit VermaNo ratings yet

- Overall and Spares Inventory Over Last Five Years (Whole NTPC)Document16 pagesOverall and Spares Inventory Over Last Five Years (Whole NTPC)SamNo ratings yet

- Coa C2015-002Document71 pagesCoa C2015-002Pearl AudeNo ratings yet

- Homework Week1 Dragan MilosavljevicDocument4 pagesHomework Week1 Dragan MilosavljevicDragan MilosavljevicNo ratings yet

- Accenture Reducing The Quantity and Cost of Customer ReturnsDocument20 pagesAccenture Reducing The Quantity and Cost of Customer ReturnsKyriakos FarmakisNo ratings yet

- Britannia Industries Financial ReportDocument15 pagesBritannia Industries Financial ReportKunal DesaiNo ratings yet

- SureshkumarDocument4 pagesSureshkumarsureshsri1976No ratings yet

- Gina Bayona HospitalityDocument2 pagesGina Bayona HospitalityHana KimNo ratings yet

- SAP B1 On Cloud - Accounting Information Systems OutlineDocument2 pagesSAP B1 On Cloud - Accounting Information Systems OutlineChristine Jane LaciaNo ratings yet

- New Resume Azwari Bin OthmanDocument6 pagesNew Resume Azwari Bin OthmanAchik AzieNo ratings yet

- Topic 6 Accounting For Joint Products, by Products and ScrapsDocument37 pagesTopic 6 Accounting For Joint Products, by Products and ScrapsFD ReynosoNo ratings yet

- Darin Armstead Resume 10.20.2019Document3 pagesDarin Armstead Resume 10.20.2019Darin ArmsteadNo ratings yet

- Ba7101 - PomDocument7 pagesBa7101 - PomanglrNo ratings yet

- Cost Accounting Question BankDocument48 pagesCost Accounting Question BankShedrine WamukekheNo ratings yet

- Performance Task in Business Finance: Submitted byDocument10 pagesPerformance Task in Business Finance: Submitted byemerencianajoshua25No ratings yet

- Units in Beginning Inventory 0 Units ProducedDocument25 pagesUnits in Beginning Inventory 0 Units ProducedAli Wiz KhalifaNo ratings yet

- OPIM101 5 UpdatedDocument49 pagesOPIM101 5 UpdatedJia YiNo ratings yet

- A Study of JIT Implementation and Operating ProblemsDocument9 pagesA Study of JIT Implementation and Operating ProblemsAshish Edwin HansdaArtsNo ratings yet

- 2.2 Company ProfileDocument43 pages2.2 Company ProfileKRISHNA SASTRYNo ratings yet

- Kinney 8e - IM - CH 11 PDFDocument14 pagesKinney 8e - IM - CH 11 PDFWeirdNo ratings yet

- My Farm, My Plan - Planning For My FutureDocument39 pagesMy Farm, My Plan - Planning For My FuturenuniNo ratings yet

- Hotel Management System ProjectDocument11 pagesHotel Management System ProjectFARHAN AHMEDNo ratings yet