You might also like

- The History of MoneyDocument29 pagesThe History of MoneyyannisxylasNo ratings yet

- Assignment: Littlefield Simulation - Game 2Document8 pagesAssignment: Littlefield Simulation - Game 2Sumit SinghNo ratings yet

- Nissan SwotDocument40 pagesNissan SwotAbhijit Kardekar0% (1)

- Brief Financial Report On Ford Versus ToyotaDocument8 pagesBrief Financial Report On Ford Versus ToyotaSayantani Nandy50% (2)

- LCD Loan PrimerDocument40 pagesLCD Loan PrimerMahesh Nagwan100% (2)

- Finance and AccountingDocument882 pagesFinance and Accountingabraham_simons67% (3)

- Lean-Mfg Basics r1Document54 pagesLean-Mfg Basics r1Agung CPNo ratings yet

- Global Auto IndustryDocument200 pagesGlobal Auto IndustryPRADITYO PUTRA PURNOMO ,100% (1)

- 02 Varun Nagar - Case HandoutDocument2 pages02 Varun Nagar - Case Handoutravi007kant100% (1)

- Payment Receipt: This Receipt Is Not Proof That Funds Have Reached The BeneficiaryDocument1 pagePayment Receipt: This Receipt Is Not Proof That Funds Have Reached The Beneficiarysunny tamrakar100% (2)

- Actrev2 - InvestmentsDocument19 pagesActrev2 - InvestmentsKenneth Bryan Tegerero Tegio100% (1)

- Disciplined Trader Trade Journal (Shares)Document851 pagesDisciplined Trader Trade Journal (Shares)Nirmal SthaNo ratings yet

- Company Profile of ToyotaDocument3 pagesCompany Profile of ToyotaAri Purnama Dewi100% (1)

- Toyota Success RecipeDocument7 pagesToyota Success Recipeapi-3740973No ratings yet

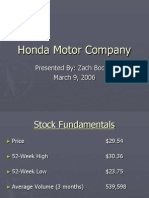

- Honda Motor Company: Presented By: Zach Bodine March 9, 2006Document25 pagesHonda Motor Company: Presented By: Zach Bodine March 9, 2006Rohit KatyalNo ratings yet

- Honda Final PPT To ShowDocument20 pagesHonda Final PPT To ShowParul ChughNo ratings yet

- Arun Bassi Sukrit Gupta Vikalp Garg Ajit PalDocument20 pagesArun Bassi Sukrit Gupta Vikalp Garg Ajit PalHarini VengalaNo ratings yet

- Presented By:: Anmol Kalucha Aniket Choudhary Animesh Batra Ashmik Paul Ashish Chawla Anshul AggarwalDocument25 pagesPresented By:: Anmol Kalucha Aniket Choudhary Animesh Batra Ashmik Paul Ashish Chawla Anshul AggarwalAniket ChoudharyNo ratings yet

- Honda Final PPT To ShowDocument20 pagesHonda Final PPT To Showvikalpgarg71% (7)

- Strategic Management Presentation On VW FINALDocument32 pagesStrategic Management Presentation On VW FINALSoham SahaNo ratings yet

- Business Management - Toyota CaseDocument14 pagesBusiness Management - Toyota CaseBilgiMBA100% (1)

- HondaDocument20 pagesHondaVivek DhandeNo ratings yet

- Honda Financial Report 2008 Analysis With Ratio AnalysisDocument14 pagesHonda Financial Report 2008 Analysis With Ratio Analysisblackhat911100% (15)

- Honda MarketingDocument29 pagesHonda MarketingAnkit GuptaNo ratings yet

- HondaDocument14 pagesHondaPawan GuptaNo ratings yet

- Honda MotorsDocument4 pagesHonda MotorsjadezzNo ratings yet

- SWOT NissanDocument7 pagesSWOT NissanWq Quan100% (1)

- GM MyDocument68 pagesGM MyRonak BhatiaNo ratings yet

- Company Analysis: Bajaj Auto LimitedDocument11 pagesCompany Analysis: Bajaj Auto LimitedNitin BaranawalNo ratings yet

- 3c Tata MotorsDocument13 pages3c Tata MotorsManjunath BaraddiNo ratings yet

- Reflective Paper - Ayush Arora (MGB18GL059)Document11 pagesReflective Paper - Ayush Arora (MGB18GL059)Ayush AroraNo ratings yet

- Company Background: Key FactsDocument10 pagesCompany Background: Key FactsShubham ShimpiNo ratings yet

- Toyota MarketingDocument291 pagesToyota Marketing2mq55dkbm6No ratings yet

- BUY BUY BUY BUY: Toyota Motor CorpDocument5 pagesBUY BUY BUY BUY: Toyota Motor CorpBrenda WijayaNo ratings yet

- Toyota Motor Corporation: A Wright Investors' Service Research ReportDocument46 pagesToyota Motor Corporation: A Wright Investors' Service Research ReportImran Max SaleemNo ratings yet

- Honda Motor Co., LTD.: Company ProfileDocument11 pagesHonda Motor Co., LTD.: Company ProfileYeo Pei ShiNo ratings yet

- Global Auto Industry: Franklin Guo Dat Hong Rex Liu Reya LuDocument200 pagesGlobal Auto Industry: Franklin Guo Dat Hong Rex Liu Reya LuHARSHIT SINGHNo ratings yet

- Acorda, Keanna Micha Ella DDocument20 pagesAcorda, Keanna Micha Ella DLennox Llew HensleyNo ratings yet

- Global Auto Industry: Franklin Guo Dat Hong Rex Liu Reya LuDocument200 pagesGlobal Auto Industry: Franklin Guo Dat Hong Rex Liu Reya LuRafee HossainNo ratings yet

- Strategic ThinkingDocument22 pagesStrategic ThinkingMashkoor KhanNo ratings yet

- Honda FinalDocument18 pagesHonda FinalSaurabh GuptaNo ratings yet

- J.P. Morgan Auto Conference Dana IncorporatedDocument11 pagesJ.P. Morgan Auto Conference Dana IncorporatedAndy HuffNo ratings yet

- Industry Overview: Marketing Issues in Automobile IndustryDocument29 pagesIndustry Overview: Marketing Issues in Automobile IndustryAbid IqbalNo ratings yet

- Assignment 2 - HondaDocument8 pagesAssignment 2 - HondaMabu MabuNo ratings yet

- Swot AnalysisDocument13 pagesSwot AnalysisPurva Bhandari0% (1)

- Honda Motor CoDocument8 pagesHonda Motor Cowe are IndiansNo ratings yet

- Internship at Rosy Blue SecuritiesDocument12 pagesInternship at Rosy Blue SecuritiesKrish JoganiNo ratings yet

- Final Report Tata MotorsdoneDocument10 pagesFinal Report Tata Motorsdone2K20MC10 AdityaNo ratings yet

- Automobile Sales - September 2013: Car, CV Sales Stay Weak, But Improvement in Two-WheelersDocument3 pagesAutomobile Sales - September 2013: Car, CV Sales Stay Weak, But Improvement in Two-WheelersTariq HaqueNo ratings yet

- RBC Motor WeeklyDocument11 pagesRBC Motor WeeklyJean Paul BésNo ratings yet

- Question 5: Can The Brand Survive Next Decade? If Yes, Then What Is Their Sustainability Plan? AnswerDocument7 pagesQuestion 5: Can The Brand Survive Next Decade? If Yes, Then What Is Their Sustainability Plan? AnswershonnashiNo ratings yet

- The Indian Automobile Industry: Presented By-Aabir Ahmad Rohit Gupta Gagandeep SinghDocument22 pagesThe Indian Automobile Industry: Presented By-Aabir Ahmad Rohit Gupta Gagandeep SinghAabir AhmadNo ratings yet

- Report BMW PDFDocument23 pagesReport BMW PDFVMMNo ratings yet

- STMGT Toyota FINAAALLLLDocument10 pagesSTMGT Toyota FINAAALLLLRasika KambliNo ratings yet

- Nada Data 2010 f2Document21 pagesNada Data 2010 f2colinsox007No ratings yet

- NissanDocument31 pagesNissanRomilio CarpioNo ratings yet

- FordDocument27 pagesFordSara MujawarNo ratings yet

- Strategic Marketing Group Volkswagen By: Max Haustein, Moyo, Tatiana MonserratDocument15 pagesStrategic Marketing Group Volkswagen By: Max Haustein, Moyo, Tatiana MonserratAhlam KassemNo ratings yet

- Business Paper - 3 Mock - October 2022Document8 pagesBusiness Paper - 3 Mock - October 2022Rashedul HassanNo ratings yet

- DownloadDocument8 pagesDownloadKevin Dani JobiliusNo ratings yet

- Ford 'S Competitors AnalysisDocument19 pagesFord 'S Competitors Analysism 144702778% (9)

- Ignition Coils, Distributors, Leads & Associated Parts (Car OE & Aftermarket) World Summary: Market Values & Financials by CountryFrom EverandIgnition Coils, Distributors, Leads & Associated Parts (Car OE & Aftermarket) World Summary: Market Values & Financials by CountryNo ratings yet

- General Automotive Repair Revenues World Summary: Market Values & Financials by CountryFrom EverandGeneral Automotive Repair Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Wiper Motors, Wiper Blades & Parts (Car OE & Aftermarket) World Summary: Market Values & Financials by CountryFrom EverandWiper Motors, Wiper Blades & Parts (Car OE & Aftermarket) World Summary: Market Values & Financials by CountryNo ratings yet

- Batteries (Commercial Vehicle OE & Aftermarket) World Summary: Market Values & Financials by CountryFrom EverandBatteries (Commercial Vehicle OE & Aftermarket) World Summary: Market Values & Financials by CountryNo ratings yet

- Interior Fittings, Trim, Seats, Heating & Ventilation (Car OE & Aftermarket) World Summary: Market Values & Financials by CountryFrom EverandInterior Fittings, Trim, Seats, Heating & Ventilation (Car OE & Aftermarket) World Summary: Market Values & Financials by CountryNo ratings yet

- Shock Absorbers, Dampers, Springs & Parts (Car OE & Aftermarket) World Summary: Market Values & Financials by CountryFrom EverandShock Absorbers, Dampers, Springs & Parts (Car OE & Aftermarket) World Summary: Market Values & Financials by CountryNo ratings yet

- Invitation For Renewal: Bajaj Allianz General Insurance Company LTDDocument2 pagesInvitation For Renewal: Bajaj Allianz General Insurance Company LTDSulekha BhattacherjeeNo ratings yet

- Creating A World Without Poverty Yunus en 9413 PDFDocument7 pagesCreating A World Without Poverty Yunus en 9413 PDFASyaukiMahmudiNo ratings yet

- Advanced Corporate Finance Course OutlineDocument10 pagesAdvanced Corporate Finance Course OutlineGilbert ShonhiwaNo ratings yet

- Mercantile Law: Arranged and SequencedDocument31 pagesMercantile Law: Arranged and SequencedSGNo ratings yet

- 3 Financial Statement AnalysisDocument45 pages3 Financial Statement AnalysisOmar Faruk 2235292660No ratings yet

- Anasco, Act6 EcoDocument6 pagesAnasco, Act6 EcoDolph Allyn AñascoNo ratings yet

- ProblemsDocument3 pagesProblemsshreya chapagainNo ratings yet

- Annex A Form 101 Checklist of DocumentsDocument3 pagesAnnex A Form 101 Checklist of DocumentsAdrian joseph AdrianoNo ratings yet

- Introducing A Travel Agency in BangladeshDocument40 pagesIntroducing A Travel Agency in BangladeshZubairia KhanNo ratings yet

- Meucci 2011 - The PrayerDocument29 pagesMeucci 2011 - The PrayershuuchuuNo ratings yet

- Acc Account Name Trial Balance Debit CreditDocument6 pagesAcc Account Name Trial Balance Debit CreditNofi NurlailaNo ratings yet

- Cash Flow Template From Xlteq LimitedDocument12 pagesCash Flow Template From Xlteq LimitedmuhammadhideyosiNo ratings yet

- Kalbe Farma TBK Billingual 31 Des 2021 ReleasedDocument163 pagesKalbe Farma TBK Billingual 31 Des 2021 ReleasedNanda IshermawanNo ratings yet

- Tax Invoice / Bill of SupplyDocument1 pageTax Invoice / Bill of SupplyCruise Films ProductionsNo ratings yet

- Nations TailDex Tail Risk IndexesDocument2 pagesNations TailDex Tail Risk IndexesEmanuele QuagliaNo ratings yet

- Fin 334-Corporate Bond Analysis 2014Document5 pagesFin 334-Corporate Bond Analysis 2014HelplineNo ratings yet

- 62287bos50449 Mod1 cp3Document51 pages62287bos50449 Mod1 cp3monicabhat96No ratings yet

- 6-7 Strategic CoorporateDocument50 pages6-7 Strategic CoorporateMoh SabilNo ratings yet

- Investment LawDocument12 pagesInvestment LawGauravKrishnaNo ratings yet

- Corporate Code of The PhilippinesDocument11 pagesCorporate Code of The PhilippinesDanJalbunaNo ratings yet

- DBFX Trading Station User GuideDocument28 pagesDBFX Trading Station User GuideSiddharth DurbhaNo ratings yet

- Exchange 2023 06 22Document1 pageExchange 2023 06 22Md Mintu MiahNo ratings yet

- REER & NeeRDocument19 pagesREER & NeeRhimanshu22109No ratings yet