You might also like

- MTI MySQL Open Source Database in 2004Document38 pagesMTI MySQL Open Source Database in 2004mahtaabk100% (1)

- Robert Kiyosaki - Cashflow Quadrant - Rich Dad's Guide To Financial FreedomDocument135 pagesRobert Kiyosaki - Cashflow Quadrant - Rich Dad's Guide To Financial Freedomjetion8489% (9)

- Napkin ProblemDocument10 pagesNapkin ProblemDian SeptianaNo ratings yet

- Nvidia Sustainiblity ReviewDocument17 pagesNvidia Sustainiblity ReviewShreyank AnchanNo ratings yet

- Marketing Assignment Coca-Cola Great Britain Repaired)Document44 pagesMarketing Assignment Coca-Cola Great Britain Repaired)Hope Romain100% (1)

- Database and SQL LabDocument32 pagesDatabase and SQL LabAnonymous oDY1vW0% (1)

- HCL Scholar SummaryDocument22 pagesHCL Scholar SummaryDOORS_userNo ratings yet

- AssignmentDocument2 pagesAssignmentDinesh SaminathanNo ratings yet

- Contempt Issue On DHLDocument7 pagesContempt Issue On DHLCaleb Jung HaeNo ratings yet

- VML Legoland FinalDocument172 pagesVML Legoland FinalebsNo ratings yet

- EduCloud Pte LTDDocument17 pagesEduCloud Pte LTDMurtuzaNo ratings yet

- InterfaceDocument22 pagesInterfaceJUAN ROJASNo ratings yet

- Introduction To Operations Research (OR) and Linear Programming (LP)Document18 pagesIntroduction To Operations Research (OR) and Linear Programming (LP)Ruchi SharmaNo ratings yet

- Project Introduction: Chinook DatabaseDocument42 pagesProject Introduction: Chinook DatabaseFiveer FreelancerNo ratings yet

- Marketing ProjectDocument18 pagesMarketing Project...No ratings yet

- Principles of Marketing-HpDocument23 pagesPrinciples of Marketing-HpVarun KumarNo ratings yet

- (Case Study at Mampong-Akuapem Presby Senior High School) : Staff Assignment ProblemDocument3 pages(Case Study at Mampong-Akuapem Presby Senior High School) : Staff Assignment ProblemHELLONo ratings yet

- PGP PSM Group 3 - VoltasDocument14 pagesPGP PSM Group 3 - VoltasVaibhav SinghNo ratings yet

- Research Paper: Memory Management in Programming LanguagesDocument15 pagesResearch Paper: Memory Management in Programming Languagesmohdanas43No ratings yet

- Objective: " Layout of Basic Gates Using 0.25 Micron Technology in Microwind"Document7 pagesObjective: " Layout of Basic Gates Using 0.25 Micron Technology in Microwind"unity123d deew100% (1)

- Cost Accounting Practices in BD PDFDocument57 pagesCost Accounting Practices in BD PDFSadman Ar RahmanNo ratings yet

- M.E (Or) QBDocument21 pagesM.E (Or) QBkeerthi_sm180% (1)

- Report On Nestle PDFDocument11 pagesReport On Nestle PDFTasnim Tasfia SrishtyNo ratings yet

- Mid Assignment - ACT 202Document4 pagesMid Assignment - ACT 202ramisa tasrimNo ratings yet

- Chapter 7: International Production Networks (Ipns) and Global Value Chains (GVCS)Document39 pagesChapter 7: International Production Networks (Ipns) and Global Value Chains (GVCS)PARUL SINGH MBA 2019-21 (Delhi)No ratings yet

- New Solutions For MichiganDocument28 pagesNew Solutions For MichiganJustin HinkleyNo ratings yet

- Failure of Paktel 2Document80 pagesFailure of Paktel 2iftikhar_qta100% (1)

- Final Exam Prep OpsDocument9 pagesFinal Exam Prep OpsadarshNo ratings yet

- Seminar ReportDocument30 pagesSeminar ReportNazeem SiddiqueNo ratings yet

- OM Assessment Exam AnswersDocument13 pagesOM Assessment Exam AnswersStar Dimasaca BenturadoNo ratings yet

- OLAP OperationsDocument20 pagesOLAP OperationsShankar AggarwalNo ratings yet

- Case Study of Hand Made Silver Filigree / Jewellery Cluster at Cuttak - OrrisaDocument5 pagesCase Study of Hand Made Silver Filigree / Jewellery Cluster at Cuttak - OrrisasupriyadhageNo ratings yet

- BANGLALINKDocument48 pagesBANGLALINKNasrullah Khan AbidNo ratings yet

- MKT 501 - Group 3 - Mini Assignment - Holistic Marketing - ACI LimitedDocument8 pagesMKT 501 - Group 3 - Mini Assignment - Holistic Marketing - ACI LimitedMd. Rafsan Jany (223052005)No ratings yet

- Makeup Behind The Mirror Going Beyond Delisting? - A Case of NIRMADocument30 pagesMakeup Behind The Mirror Going Beyond Delisting? - A Case of NIRMAEdzwan RedzaNo ratings yet

- PROJECT REPORT taBLEAU 2 PDFDocument12 pagesPROJECT REPORT taBLEAU 2 PDFrahulsg0358No ratings yet

- The Formula:: No Pressure - ObidiponbedeDocument3 pagesThe Formula:: No Pressure - Obidiponbedejinnah kayNo ratings yet

- AmulDocument9 pagesAmulAshik NavasNo ratings yet

- ICT Tata Sky Project FinalDocument24 pagesICT Tata Sky Project FinalSaurabh GuptaNo ratings yet

- Birlasoft CaseA PDFDocument30 pagesBirlasoft CaseA PDFRitika SharmaNo ratings yet

- General Objectives: Unit 1 - Computer-Based Information Systems (Cbis)Document9 pagesGeneral Objectives: Unit 1 - Computer-Based Information Systems (Cbis)alia_aziziNo ratings yet

- Machine Learning by Andrew NG CourseraDocument5 pagesMachine Learning by Andrew NG Courserasameeksha chiguruNo ratings yet

- UntitledDocument10 pagesUntitledmehvishNo ratings yet

- Supply Chain Management NotesDocument35 pagesSupply Chain Management NotesRazin GajiwalaNo ratings yet

- Assignment - 2 AIT580: Shravan Chintha G01064991 Big DataDocument5 pagesAssignment - 2 AIT580: Shravan Chintha G01064991 Big DataMulya ShreeNo ratings yet

- Lecture 6 - Introduction To Networking ConceptsDocument14 pagesLecture 6 - Introduction To Networking ConceptsNelsonMoseMNo ratings yet

- Global Footprint of Pran RFL GroupDocument23 pagesGlobal Footprint of Pran RFL GroupShaffyNo ratings yet

- Alex Wilson MKT 510 Nestle QuestionsDocument6 pagesAlex Wilson MKT 510 Nestle QuestionsALEX WILSONNo ratings yet

- OcadoDocument4 pagesOcadoanoop godaraNo ratings yet

- PowerPC AssignmentDocument5 pagesPowerPC AssignmentArkadip RayNo ratings yet

- Rahimafrooz MKT PlanDocument35 pagesRahimafrooz MKT Plantoufiq1111No ratings yet

- 0-1 Integer Linear Programming Model For Location Selection of Fire Station: A Case Study in IndonesiaDocument8 pages0-1 Integer Linear Programming Model For Location Selection of Fire Station: A Case Study in IndonesiaAbed Soliman100% (1)

- Unit 7Document27 pagesUnit 7Pawan SinghNo ratings yet

- Assignment 2Document9 pagesAssignment 2azisNo ratings yet

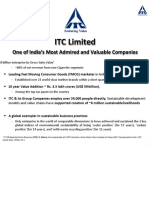

- ITC Corporate PresentationDocument59 pagesITC Corporate Presentationpankaj kumar singhNo ratings yet

- TM351 Data Management and Analysis: Prepared by Eng. A.Samy Tel: 99941566Document7 pagesTM351 Data Management and Analysis: Prepared by Eng. A.Samy Tel: 99941566Christina FingtonNo ratings yet

- +road Development Program by NHAIDocument12 pages+road Development Program by NHAIsumit pamechaNo ratings yet

- Pricing Answers PDFDocument12 pagesPricing Answers PDFvineel kumarNo ratings yet

- Q:2 Draw and Explain A Model For Thinking About Ethical, Social and Political Issues?Document5 pagesQ:2 Draw and Explain A Model For Thinking About Ethical, Social and Political Issues?Shahbaz ArtsNo ratings yet

- Data Base Normalization and ERDDocument23 pagesData Base Normalization and ERDsxurdcNo ratings yet

- Ogonquit Enterprises Prepares Annual Financial Statements and Adjusts Its AccountsDocument1 pageOgonquit Enterprises Prepares Annual Financial Statements and Adjusts Its AccountsMiroslav GegoskiNo ratings yet

- R WorkshopDocument47 pagesR WorkshopAmitNo ratings yet

- Cancer in Thailand - VII PDFDocument232 pagesCancer in Thailand - VII PDFPonlapat YonglitthipagonNo ratings yet

- Pages '09: User GuideDocument279 pagesPages '09: User GuideKarl DavisNo ratings yet

- MeV Manual 4.0Document276 pagesMeV Manual 4.0Ponlapat Yonglitthipagon100% (1)

- Iworks WorkshopDocument4 pagesIworks WorkshopPonlapat YonglitthipagonNo ratings yet

- Write Better Essays 2eDocument208 pagesWrite Better Essays 2eyear2009100% (4)

- Introduction To Microarray Technology: PresenterDocument59 pagesIntroduction To Microarray Technology: PresenteranilNo ratings yet

- R12 Compensation Activity GuideDocument224 pagesR12 Compensation Activity Guidepersonifiedgenius0% (1)

- Empowerment Technologies11 12 - q1 - wk2 - Online Safety and Contextualized SearchDocument18 pagesEmpowerment Technologies11 12 - q1 - wk2 - Online Safety and Contextualized SearchRadian LacuestaNo ratings yet

- Surescripts Connectivity Questionnaire 20110822Document12 pagesSurescripts Connectivity Questionnaire 20110822Rabindra P.SinghNo ratings yet

- Question Bank Unit I and IIDocument3 pagesQuestion Bank Unit I and IIHariesh SNo ratings yet

- Configuring MIB SupportDocument6 pagesConfiguring MIB SupportSalkovićElvisNo ratings yet

- Worksheet - 1.1: Name: Tarun Bisht Branch/Sec: CSE/29 - B UID: 20BCS6130 Subject: DS LabDocument5 pagesWorksheet - 1.1: Name: Tarun Bisht Branch/Sec: CSE/29 - B UID: 20BCS6130 Subject: DS Lababhishek kumarNo ratings yet

- Analysis Toolbox (Psat) 2.1.7 Dengan Metode Newton RaphsonDocument7 pagesAnalysis Toolbox (Psat) 2.1.7 Dengan Metode Newton RaphsonAhmad MuzammilNo ratings yet

- Apollo Guidance ComputerDocument61 pagesApollo Guidance ComputerMarco CisnerosNo ratings yet

- Module-6 Repetition LoopingDocument6 pagesModule-6 Repetition LoopingjunNo ratings yet

- Oracle ServersDocument302 pagesOracle ServerseromerocNo ratings yet

- V7 QBR Ad Hoc Reporting Release Rev4Document94 pagesV7 QBR Ad Hoc Reporting Release Rev4blademakerNo ratings yet

- Accuvix XQDocument8 pagesAccuvix XQbashir019No ratings yet

- Networking Reference GuideDocument564 pagesNetworking Reference GuideJuan EspinozaNo ratings yet

- Special Publication: Sensor AutomaticDocument504 pagesSpecial Publication: Sensor Automaticfarfarfifi3No ratings yet

- River Flood Modelling For Nzoia River - A Quasi 2-D ApproachDocument14 pagesRiver Flood Modelling For Nzoia River - A Quasi 2-D Approachsalt2009No ratings yet

- CFL Pumping LemmaDocument11 pagesCFL Pumping LemmawithoutnonsenseNo ratings yet

- MongoDB CommandsDocument3 pagesMongoDB CommandsprabindasNo ratings yet

- Back SheetDocument3 pagesBack SheetAkande AbdulazeezNo ratings yet

- International Journal of Computer Technologie Volume 3 - Issue 3 - International Journal of Computer and Information Technology (IJCIT)Document2 pagesInternational Journal of Computer Technologie Volume 3 - Issue 3 - International Journal of Computer and Information Technology (IJCIT)StellaEstelNo ratings yet

- Computer Applications Technology: Teacher's GuideDocument220 pagesComputer Applications Technology: Teacher's GuideMelanieNo ratings yet

- SchneiderDocument64 pagesSchneiderJhon Benites TenorioNo ratings yet

- README!!!Document5 pagesREADME!!!AlcaNo ratings yet

- 04 SAS With IEC 61850Document26 pages04 SAS With IEC 61850sridhar30481647No ratings yet

- The Book of (PLC & SCADA) Dosing System by HMIDocument102 pagesThe Book of (PLC & SCADA) Dosing System by HMIAwidhi KresnawanNo ratings yet

- DSP Integrated Circuits 3Document3 pagesDSP Integrated Circuits 3brindkowsiNo ratings yet

- Starting Forth PDFDocument166 pagesStarting Forth PDFnitetrkrNo ratings yet

- Ec160 English ManualDocument227 pagesEc160 English ManualYudi Widodo Louser100% (2)

- Q&A Deniz KoyuDocument4 pagesQ&A Deniz KoyuJosé Carlos Guillén ZambranoNo ratings yet