You might also like

- Chapters 10,11 and 12 Assessment QuestionsDocument10 pagesChapters 10,11 and 12 Assessment QuestionsSteven Sanderson100% (1)

- Chapter 19,20,21,22 Assesment QuestionsDocument19 pagesChapter 19,20,21,22 Assesment QuestionsSteven Sanderson100% (3)

- Reaction Paper To Chater 13Document2 pagesReaction Paper To Chater 13Steven Sanderson100% (5)

- Reaction Paper To Chapter 6Document3 pagesReaction Paper To Chapter 6Steven Sanderson100% (1)

- Reaction Report To Student OrientationDocument1 pageReaction Report To Student OrientationSteven SandersonNo ratings yet

- Chapter 10 Reactioin PaperDocument2 pagesChapter 10 Reactioin PaperSteven SandersonNo ratings yet

- Chapter 20 Reaction PaperDocument3 pagesChapter 20 Reaction PaperSteven Sanderson100% (4)

- Chapters 7,8,9 Assesment QuestionsDocument9 pagesChapters 7,8,9 Assesment QuestionsSteven Sanderson100% (3)

- Chapters 13, 14, 15, 16 Assessment QuestionsDocument11 pagesChapters 13, 14, 15, 16 Assessment QuestionsSteven Sanderson100% (5)

- Chapter 19,20,21,22 Assesment QuestionsDocument19 pagesChapter 19,20,21,22 Assesment QuestionsSteven Sanderson100% (3)

- Chapter One and 2 Assessment QuestionsDocument6 pagesChapter One and 2 Assessment QuestionsSteven Sanderson100% (3)

- Chap 19 - Selected Ex & ProbDocument6 pagesChap 19 - Selected Ex & ProbSteven Sanderson100% (1)

- Chapters 3,4,5 and 6 Assesment QuestionsDocument10 pagesChapters 3,4,5 and 6 Assesment QuestionsSteven Sanderson100% (4)

- Chapter 21 Reaction PaperDocument4 pagesChapter 21 Reaction PaperSteven Sanderson100% (1)

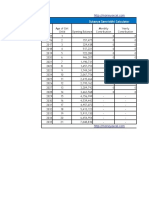

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Acct II - Chapter 15 Lecture NotesDocument4 pagesAcct II - Chapter 15 Lecture NotesSteven Sanderson100% (1)

- Accounting II - Chap 14 Lecture NotesDocument6 pagesAccounting II - Chap 14 Lecture NotesSteven Sanderson100% (4)

- Chap 12 - Selected Ex & ProbDocument2 pagesChap 12 - Selected Ex & ProbSteven SandersonNo ratings yet

- CH 14Document54 pagesCH 14Steven SandersonNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Chap 13 - Selected Ex & ProbDocument1 pageChap 13 - Selected Ex & ProbSteven SandersonNo ratings yet

- Chap 14 - Selected Ex & ProbDocument8 pagesChap 14 - Selected Ex & ProbSteven SandersonNo ratings yet

- Chap 15 - Selected Ex & ProbDocument7 pagesChap 15 - Selected Ex & ProbSteven SandersonNo ratings yet

- Acounting II - Chap 12 Accounting Principles - Part II - SLNDocument12 pagesAcounting II - Chap 12 Accounting Principles - Part II - SLNSteven Sanderson100% (2)

- Chapter 13 - Teaching ExhibitsDocument6 pagesChapter 13 - Teaching ExhibitsSteven SandersonNo ratings yet

- Chap 18 - Selected Ex & ProbDocument6 pagesChap 18 - Selected Ex & ProbSteven SandersonNo ratings yet

- Chap 16 - Selected Ex & ProbDocument3 pagesChap 16 - Selected Ex & ProbSteven SandersonNo ratings yet

- Chap. 23 - Selected Ex. & Prob.Document5 pagesChap. 23 - Selected Ex. & Prob.Steven SandersonNo ratings yet

- Chap 20 - Selected Ex & ProbDocument3 pagesChap 20 - Selected Ex & ProbSteven SandersonNo ratings yet

- Chapter 13 - Lecture NotesDocument6 pagesChapter 13 - Lecture NotesSteven Sanderson100% (3)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Holder in Due Course CasesDocument9 pagesHolder in Due Course CasesGela Bea BarriosNo ratings yet

- Compilation of Cases Credit TransactionsDocument347 pagesCompilation of Cases Credit TransactionsebenezermanzanormtNo ratings yet

- General Awareness MCQ New AugDocument7 pagesGeneral Awareness MCQ New AugManish SinghNo ratings yet

- Epilogue Magazine, September 2009Document80 pagesEpilogue Magazine, September 2009Epilogue MagazineNo ratings yet

- KYC Master Directions 2016 - Presentations For RefDocument15 pagesKYC Master Directions 2016 - Presentations For RefAnagha LokhandeNo ratings yet

- Boa HelpDocument2 pagesBoa HelpJorge LuissNo ratings yet

- FIN80004 Lecture1Document28 pagesFIN80004 Lecture1visha183240No ratings yet

- Subprime CrisisDocument18 pagesSubprime CrisisRicha SinghNo ratings yet

- Department of Financial Institutions ESBMDocument34 pagesDepartment of Financial Institutions ESBMAnu VanuNo ratings yet

- TVM Complete TemplateDocument17 pagesTVM Complete TemplateAlok RajNo ratings yet

- Welcome Package (GIC-220610049)Document3 pagesWelcome Package (GIC-220610049)vivekNo ratings yet

- GW 2013 Arab World Sample PagesDocument9 pagesGW 2013 Arab World Sample PagesAlaaNo ratings yet

- 6 PakistanDocument62 pages6 PakistanKhalil Ur Rehman YousafzaiNo ratings yet

- HSBC 1billon Euro e Clear 16 Pages of SBLC 62+2% LoiDocument12 pagesHSBC 1billon Euro e Clear 16 Pages of SBLC 62+2% LoiKaran LA100% (2)

- How To Configure SSL For SAP HANA XS Engine Using SAPCryptoDocument4 pagesHow To Configure SSL For SAP HANA XS Engine Using SAPCryptopraveenr5883No ratings yet

- Saji DDDD DDDDDocument37 pagesSaji DDDD DDDDTalha Iftekhar Khan SwatiNo ratings yet

- Proforma 1EDocument3 pagesProforma 1EEric HernandezNo ratings yet

- Gov Uscourts Nysd 524076 1 0Document95 pagesGov Uscourts Nysd 524076 1 0ForkLogNo ratings yet

- Kalpana Bisen Paper On Dress CodeDocument19 pagesKalpana Bisen Paper On Dress CodeKalpana BisenNo ratings yet

- Vietnam Financial Structure: The Overview of Direct and Indirect Finance in Viet Nam 1Document5 pagesVietnam Financial Structure: The Overview of Direct and Indirect Finance in Viet Nam 1Hiền NguyễnNo ratings yet

- Sukanya Samriddhi Calculator VariableDocument38 pagesSukanya Samriddhi Calculator VariableRam SewakNo ratings yet

- 0813897476 (1)Document2 pages0813897476 (1)Raja RazaliaNo ratings yet

- NPO Master ProblemDocument3 pagesNPO Master ProblemSaurabh AdakNo ratings yet

- VII Semester QuestionsDocument8 pagesVII Semester QuestionsRadha SundarNo ratings yet

- Universak BankingDocument33 pagesUniversak BankingprashantgoruleNo ratings yet

- People Vs Puig and PorrasDocument1 pagePeople Vs Puig and Porraskarl doceoNo ratings yet

- Allahabad Bank - Internet Banking System 6 PDFDocument1 pageAllahabad Bank - Internet Banking System 6 PDFarjunv_14No ratings yet

- Power of AttorneyDocument1 pagePower of AttorneyAubrien Fachi MusambakarumeNo ratings yet

- Banking Law (Part 7 Case Digests)Document14 pagesBanking Law (Part 7 Case Digests)Justice PajarilloNo ratings yet

- Bet You Thought (Federal Reserve) PDFDocument21 pagesBet You Thought (Federal Reserve) PDFtdon777100% (6)