You might also like

- Case 2 Han-Solar-And-The-Green-Supply-Chain-CaseDocument13 pagesCase 2 Han-Solar-And-The-Green-Supply-Chain-CaseGaurav Dm50% (2)

- SPIL-Annual Report 2015 Upload PDFDocument195 pagesSPIL-Annual Report 2015 Upload PDFVarun BansalNo ratings yet

- Tire City Company Case StudyDocument1 pageTire City Company Case StudySo goodNo ratings yet

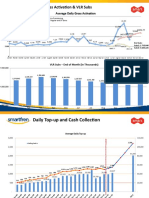

- Daily Gross Activation & VLR SubsDocument3 pagesDaily Gross Activation & VLR Subsdarwin.saragihNo ratings yet

- Icmd 2010Document2 pagesIcmd 2010meilindaNo ratings yet

- MDKA SucorDocument6 pagesMDKA SucorFathan MujibNo ratings yet

- Inception Report - DPL Roadmap 2030 - 25022022 - DraftDocument27 pagesInception Report - DPL Roadmap 2030 - 25022022 - Draftmintu halderNo ratings yet

- Mutual Fund Holding Report - Aug22-IDBICAPITALDocument56 pagesMutual Fund Holding Report - Aug22-IDBICAPITALJay SharmaNo ratings yet

- PT Inti Agri ResourcestbkDocument2 pagesPT Inti Agri ResourcestbkmeilindaNo ratings yet

- Lab AuditDocument9 pagesLab AuditPutrathe LonelydjNo ratings yet

- SOIC-Consitent CompoundersDocument28 pagesSOIC-Consitent CompoundersPrateekNo ratings yet

- DK Profile2010 2K 10mar2011Document48 pagesDK Profile2010 2K 10mar2011kodirNo ratings yet

- Mutual Fund Holding Report - Nov 22 - 13122022Document56 pagesMutual Fund Holding Report - Nov 22 - 13122022Ankit PandeNo ratings yet

- NAME: Ahmad Class: Mba ROLL NO: 18001 Presented To Kashif AlviDocument17 pagesNAME: Ahmad Class: Mba ROLL NO: 18001 Presented To Kashif AlviAsad AliNo ratings yet

- PT Astra Agro Lestari TBK.: Summary of Financial StatementDocument2 pagesPT Astra Agro Lestari TBK.: Summary of Financial StatementIntan Maulida SuryaningsihNo ratings yet

- AKUPREPSLPWDocument1 pageAKUPREPSLPWuzrabaig111No ratings yet

- (FM) AssignmentDocument7 pages(FM) Assignmentnuraini putriNo ratings yet

- Family Mart Annual Report1Document39 pagesFamily Mart Annual Report1태하No ratings yet

- 新城发展2022年中期业绩PPT 0830v1Document39 pages新城发展2022年中期业绩PPT 0830v1Muska ChiuNo ratings yet

- IDX Financial Data Ratios 2009Document8 pagesIDX Financial Data Ratios 2009Mohammad Noor SyahrielNo ratings yet

- English WG Compro LowDocument70 pagesEnglish WG Compro LowyosaNo ratings yet

- IcbpDocument2 pagesIcbpdennyaikiNo ratings yet

- BEPZA Re-Fixation of Minimum Wages & Benefits 2018Document5 pagesBEPZA Re-Fixation of Minimum Wages & Benefits 2018Mazharul IslamNo ratings yet

- Gross Domestic Product (GDP) at Current PricesDocument4 pagesGross Domestic Product (GDP) at Current PricesChakma MansonNo ratings yet

- Spyder Case Intro: See Templates On Blackboard For WACC and DCF OutputDocument11 pagesSpyder Case Intro: See Templates On Blackboard For WACC and DCF Outputrock sinhaNo ratings yet

- Notes For Coca Cola PresentationDocument16 pagesNotes For Coca Cola PresentationAsad AliNo ratings yet

- MS Client Portfolio 728725 R10728725 2022-11-30Document1 pageMS Client Portfolio 728725 R10728725 2022-11-30Darul kutni 111No ratings yet

- 2014 - AMRT - AMRT - Annual Report - 2014 PDFDocument207 pages2014 - AMRT - AMRT - Annual Report - 2014 PDFPalmaria SitanggangNo ratings yet

- PT Gozco Plantations TBK.: Summary of Financial StatementDocument2 pagesPT Gozco Plantations TBK.: Summary of Financial StatementMaradewiNo ratings yet

- Revised Alfalah Solar Financing - Mr. JahanzaibDocument3 pagesRevised Alfalah Solar Financing - Mr. JahanzaibChaudhary Muhammad Suban TasirNo ratings yet

- Salary Attribution BesDocument3 pagesSalary Attribution BesEmmanuel CastroNo ratings yet

- Gita AgricultureDocument20 pagesGita AgriculturemrigendrarimalNo ratings yet

- Rmba - Icmd 2011 (B02)Document2 pagesRmba - Icmd 2011 (B02)annisa lahjieNo ratings yet

- AnalysisDocument20 pagesAnalysisSAHEB SAHANo ratings yet

- PT Astra Agro Lestari TBK.: Summary of Financial StatementDocument2 pagesPT Astra Agro Lestari TBK.: Summary of Financial Statementkurnia murni utamiNo ratings yet

- AC 414 814 - Exam 2 - Practice ProblemsDocument2 pagesAC 414 814 - Exam 2 - Practice ProblemsCameron McGaffiganNo ratings yet

- Microsoft Corporation Financial Statements and Supplementary DataDocument43 pagesMicrosoft Corporation Financial Statements and Supplementary DataDylan MakroNo ratings yet

- Cfin Assignment WorkingsDocument8 pagesCfin Assignment Workingspriyal batraNo ratings yet

- Google Q3 2008 Quarterly Earnings SummaryDocument15 pagesGoogle Q3 2008 Quarterly Earnings SummaryEd McManus100% (1)

- Analysis of Financial Statement: Khurram Mansoor Muhammad Noman Shaf Mubasher RehmanDocument31 pagesAnalysis of Financial Statement: Khurram Mansoor Muhammad Noman Shaf Mubasher RehmanNandakumarDuraisamyNo ratings yet

- Fsprojected 2016 May 24Document35 pagesFsprojected 2016 May 24CarloKCMigzGonzalesNo ratings yet

- Note:: Mengetahui, BendaharaDocument1 pageNote:: Mengetahui, Bendaharampwpterbaruu60No ratings yet

- Aces ICMD 2009Document2 pagesAces ICMD 2009abdillahtantowyjauhariNo ratings yet

- Hino Pak Limited IBFDocument16 pagesHino Pak Limited IBFOmerSyedNo ratings yet

- Kbri ICMD 2009Document2 pagesKbri ICMD 2009abdillahtantowyjauhariNo ratings yet

- Nyse WCN 2006Document106 pagesNyse WCN 2006ReswinNo ratings yet

- Investitionsanalyse - Polar Sports (A)Document8 pagesInvestitionsanalyse - Polar Sports (A)ScribdTranslationsNo ratings yet

- Commitment: To CareDocument100 pagesCommitment: To Carea769No ratings yet

- Excel For IS-tempDocument11 pagesExcel For IS-tempsaikrishnailuriNo ratings yet

- Financial Model of A Medical Software For ClinicsDocument16 pagesFinancial Model of A Medical Software For ClinicsAl KeyNo ratings yet

- NITORI FY2022 - 4Q - Financial Report EnglishDocument39 pagesNITORI FY2022 - 4Q - Financial Report Englishlofevi5003No ratings yet

- Revenue:: AssumptionsDocument38 pagesRevenue:: AssumptionsusmanthesaviorNo ratings yet

- Olam International Limited: Q1 2016 Results BriefingDocument24 pagesOlam International Limited: Q1 2016 Results Briefingashokdb2kNo ratings yet

- Hade PDFDocument2 pagesHade PDFMaradewiNo ratings yet

- PT Pelat Timah Nusantara TBK.: Summary of Financial StatementDocument2 pagesPT Pelat Timah Nusantara TBK.: Summary of Financial StatementTarigan SalmanNo ratings yet

- ط§ظƒط³ظ„ ط´ظٹطھ ط±ط§ط¦ط¹ ظپظٹ ط§ظ„طھطظ„ظٹظ„ ط§ظ„ظ…ط§ظ„ظٹDocument143 pagesط§ظƒط³ظ„ ط´ظٹطھ ط±ط§ط¦ط¹ ظپظٹ ط§ظ„طھطظ„ظٹظ„ ط§ظ„ظ…ط§ظ„ظٹaliNo ratings yet

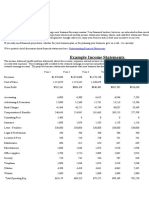

- Example Income Statements: Business Plan Financial ProjectionsDocument3 pagesExample Income Statements: Business Plan Financial ProjectionsSUMANTO SHARANNo ratings yet

- Guntur Break UpDocument1 pageGuntur Break UpKiran KumarNo ratings yet

- MRNOI00489060000017020Document1 pageMRNOI00489060000017020Ramesh MishraNo ratings yet

- Abba PDFDocument2 pagesAbba PDFAndriPigeonNo ratings yet

- Cambridge O Level: Accounting 7707/22 October/November 2022Document16 pagesCambridge O Level: Accounting 7707/22 October/November 2022Marlene BandaNo ratings yet

- OM 1st SemesterDocument32 pagesOM 1st Semestermenna mokhtarNo ratings yet

- Masters in Business Administration-MBA Semester-4 MF0007 - Treasury Management - 2 Credits Assignment Set-1Document9 pagesMasters in Business Administration-MBA Semester-4 MF0007 - Treasury Management - 2 Credits Assignment Set-1kipokhriyalNo ratings yet

- McDonalds Marketing SwotDocument4 pagesMcDonalds Marketing SwotHarsh AhujaNo ratings yet

- Constellation Energy Group Inc: FORM 425Document9 pagesConstellation Energy Group Inc: FORM 425Anonymous Feglbx5No ratings yet

- Gadia v. Sykes Asia, Inc., G.R. No. 209499, January 28, 2015Document2 pagesGadia v. Sykes Asia, Inc., G.R. No. 209499, January 28, 2015Karra Mae Changiwan CrisostomoNo ratings yet

- Entrepreneurship-11 12 Q2 SLM WK2Document6 pagesEntrepreneurship-11 12 Q2 SLM WK2MattNo ratings yet

- The Smiths Supplier Code of Business EthicsDocument6 pagesThe Smiths Supplier Code of Business EthicsAris SuwandiNo ratings yet

- Intermediate Accounting Chap 10Document192 pagesIntermediate Accounting Chap 10Gaurav NagpalNo ratings yet

- Introduction To FinTechDocument34 pagesIntroduction To FinTechvarun022084100% (4)

- BANKING ALLIED LAWS 10 November 2019Document19 pagesBANKING ALLIED LAWS 10 November 2019David YapNo ratings yet

- Philippine PovertyDocument2 pagesPhilippine PovertyHannah BarandaNo ratings yet

- Objectives: Brand Positioning: Positioning StatementDocument10 pagesObjectives: Brand Positioning: Positioning StatementMohsin NadeemNo ratings yet

- Jensen-1991-Corporate Control and The Politics of FinanceDocument23 pagesJensen-1991-Corporate Control and The Politics of Financeebrahimnejad64No ratings yet

- 7-Niranjanamurthy-Analysis of E-Commerce and M-Commerce AdvantagesDocument13 pages7-Niranjanamurthy-Analysis of E-Commerce and M-Commerce AdvantagesHuyen NguyenNo ratings yet

- Intermediate Accounting: Non-Financial and Current LiabilitiesDocument79 pagesIntermediate Accounting: Non-Financial and Current LiabilitiesShuo LuNo ratings yet

- Lheo Lee Gara My Dream Profession: ENTREPRENEURDocument2 pagesLheo Lee Gara My Dream Profession: ENTREPRENEURNolan GaraNo ratings yet

- Supply Curve of LabourDocument3 pagesSupply Curve of LabourTim InawsavNo ratings yet

- Chapter 9 Review QuestionsDocument8 pagesChapter 9 Review QuestionsKanika DahiyaNo ratings yet

- Societe Generale-Mind Matters-James Montier-Vanishing Value-Has The Market Rallied Too Far, Too Fast - 090520Document6 pagesSociete Generale-Mind Matters-James Montier-Vanishing Value-Has The Market Rallied Too Far, Too Fast - 090520yhlung2009No ratings yet

- Over Not Over Tax: Basic Income Table (Tax Code, Section 24 A)Document2 pagesOver Not Over Tax: Basic Income Table (Tax Code, Section 24 A)Juliana ChengNo ratings yet

- International Career & Talent ManagementDocument15 pagesInternational Career & Talent ManagementCHINAR GUPTANo ratings yet

- Make in India Advantages, Disadvantages and Impact On Indian EconomyDocument8 pagesMake in India Advantages, Disadvantages and Impact On Indian EconomyAkanksha SinghNo ratings yet

- ACC 201 Cheat Sheet: by ViaDocument1 pageACC 201 Cheat Sheet: by ViaAnaze_hNo ratings yet

- Economics PDFDocument44 pagesEconomics PDFyesuNo ratings yet

- Fall10mid1 ProbandsolnDocument8 pagesFall10mid1 Probandsolnivanata72No ratings yet

- Unit 2 Human Resource PlanningDocument18 pagesUnit 2 Human Resource PlanningGaurav vaidyaNo ratings yet

- InvestmentDocument9 pagesInvestmentJade Malaque0% (1)

- Correction of ErrorsDocument15 pagesCorrection of ErrorsEliyah Jhonson100% (1)