You might also like

- Spyder Student ExcelDocument21 pagesSpyder Student ExcelNatasha PerryNo ratings yet

- Spyder Active SportsDocument12 pagesSpyder Active SportsShubham SharmaNo ratings yet

- Spyder Sports: Ashutosh DashDocument34 pagesSpyder Sports: Ashutosh DashSaurabh ChhabraNo ratings yet

- FBE 529 Lecture 1 PDFDocument26 pagesFBE 529 Lecture 1 PDFJIAYUN SHENNo ratings yet

- GMP Analysis of Crocs Share PriceDocument6 pagesGMP Analysis of Crocs Share PriceKshitishNo ratings yet

- SpyderDocument3 pagesSpyderHello100% (1)

- Ducati: In pursuit of MagicDocument12 pagesDucati: In pursuit of MagicGokul ChhabraNo ratings yet

- Sun Brewing Case ExhibitsDocument26 pagesSun Brewing Case ExhibitsShshankNo ratings yet

- CFP Revenue:: (Amounts in Thousands, Except Per Unit Prices and Monthly Subscription Prices)Document3 pagesCFP Revenue:: (Amounts in Thousands, Except Per Unit Prices and Monthly Subscription Prices)Shubham SharmaNo ratings yet

- LoeaDocument21 pagesLoeahddankerNo ratings yet

- Analisis Foda AirbnbDocument4 pagesAnalisis Foda AirbnbEliana MorilloNo ratings yet

- Fuel SalesDocument11 pagesFuel SalesFabiola SE100% (1)

- Nestle and Alcon - The Value of ADocument33 pagesNestle and Alcon - The Value of Akjpcs120% (1)

- Always Use 2 Decimal Places (When % As Percent - Not As Fractions) and Provide Detail of The Calculations MadeDocument2 pagesAlways Use 2 Decimal Places (When % As Percent - Not As Fractions) and Provide Detail of The Calculations MadeKirtiKishanNo ratings yet

- Panera BreadDocument23 pagesPanera BreadtomNo ratings yet

- USTDocument4 pagesUSTJames JeffersonNo ratings yet

- Ben & Jerry's Homemade Ice Cream Inc: A Period of Transition Case AnalysisDocument5 pagesBen & Jerry's Homemade Ice Cream Inc: A Period of Transition Case AnalysisSaad JavedNo ratings yet

- Toy WorldDocument4 pagesToy WorldDhirendra Kumar Sahu100% (1)

- Polar Sports 5 PDFDocument18 pagesPolar Sports 5 PDFPaolo SergioNo ratings yet

- Harley Davidson Case StudyDocument8 pagesHarley Davidson Case StudyfossacecaNo ratings yet

- Exhibit 1Document2 pagesExhibit 1Natasha PerryNo ratings yet

- Garanti Payment Systems:: Digital Transformation StrategyDocument12 pagesGaranti Payment Systems:: Digital Transformation StrategySwarnajit SahaNo ratings yet

- Impairing The Microsoft - Nokia PairingDocument54 pagesImpairing The Microsoft - Nokia Pairingjk kumarNo ratings yet

- GoodBelly Sales Data AnalysisDocument135 pagesGoodBelly Sales Data AnalysisCHEERAAYU CHOWHANNo ratings yet

- Computer AssociatesDocument18 pagesComputer AssociatesRosel RicafortNo ratings yet

- GE Health Care Case: Executive SummaryDocument4 pagesGE Health Care Case: Executive SummarykpraneethkNo ratings yet

- Sneaker Excel Sheet For Risk AnalysisDocument11 pagesSneaker Excel Sheet For Risk AnalysisSuperGuyNo ratings yet

- LUND Case 2 PDFDocument34 pagesLUND Case 2 PDFMarkus GunawanNo ratings yet

- Asahi Case Final FileDocument4 pagesAsahi Case Final FileRUPIKA R GNo ratings yet

- Creating Value in Private Equity with Strategic AcquisitionsDocument3 pagesCreating Value in Private Equity with Strategic AcquisitionsJitesh ThakurNo ratings yet

- Group-13 Case 12Document80 pagesGroup-13 Case 12Abu HorayraNo ratings yet

- Case Study Analysis: Chestnut FoodsDocument7 pagesCase Study Analysis: Chestnut FoodsNaman KohliNo ratings yet

- Tata Corus Acquisition and M&ADocument16 pagesTata Corus Acquisition and M&ASaurabh PaliwalNo ratings yet

- Clean SpritzDocument2 pagesClean SpritzSaurabh KadamNo ratings yet

- Kel017 PDF Eng PDFDocument6 pagesKel017 PDF Eng PDFDuc NguyenNo ratings yet

- 02 Kitty-Hawk Case NotesDocument2 pages02 Kitty-Hawk Case NotesGary Putra RizaldyNo ratings yet

- Maximizing Shareholder Value Through Optimal Dividend and Buyback PolicyDocument2 pagesMaximizing Shareholder Value Through Optimal Dividend and Buyback PolicyRichBrook7No ratings yet

- Sealed Air Corporation's Leveraged RecapitalizationDocument7 pagesSealed Air Corporation's Leveraged RecapitalizationKumarNo ratings yet

- TDC Case FinalDocument3 pagesTDC Case Finalbjefferson21No ratings yet

- This Spreadsheet Supports STUDENT Analysis of The Case "Bob's Baloney" (UVA-F-1942)Document4 pagesThis Spreadsheet Supports STUDENT Analysis of The Case "Bob's Baloney" (UVA-F-1942)LAWZ1017No ratings yet

- Aleph Farms Case Analysis Highlights Company's Focus on SustainabilityDocument7 pagesAleph Farms Case Analysis Highlights Company's Focus on SustainabilityOlivia HorvathNo ratings yet

- Comparing Depreciation at Delta Air Lines and Singapore AirlinesDocument110 pagesComparing Depreciation at Delta Air Lines and Singapore AirlinesSiratullah ShahNo ratings yet

- Section E - Group 1 - RegionFly CaseDocument6 pagesSection E - Group 1 - RegionFly CaseAshish VijayaratnaNo ratings yet

- Case Study - GMDocument8 pagesCase Study - GMAustin Bray100% (1)

- M&A - Valuation - Expanded - BV - SS EQUIPODocument3 pagesM&A - Valuation - Expanded - BV - SS EQUIPOGianina Mendoza NestaresNo ratings yet

- How Southwest Airlines Reduces Costs with Rapid Turnaround TimesDocument2 pagesHow Southwest Airlines Reduces Costs with Rapid Turnaround TimesAli MalikNo ratings yet

- Lille Tissage WorksheetDocument19 pagesLille Tissage WorksheetJaouadiNo ratings yet

- Dastin Brass: Cost Activity AnalysisDocument11 pagesDastin Brass: Cost Activity AnalysisHamed Khazaee100% (1)

- On Nirma CaseDocument36 pagesOn Nirma CaseMuskaan ChaudharyNo ratings yet

- Creative Sports Solution-RevisedDocument4 pagesCreative Sports Solution-RevisedRohit KumarNo ratings yet

- Forecasting Case - XlxsDocument8 pagesForecasting Case - Xlxsmayank.dce123No ratings yet

- World Wide Paper CompanyDocument2 pagesWorld Wide Paper CompanyAshwinKumarNo ratings yet

- OM Scott Case AnalysisDocument20 pagesOM Scott Case AnalysissushilkhannaNo ratings yet

- VALUATIONS Methods and Tools for Assessing Company WorthDocument8 pagesVALUATIONS Methods and Tools for Assessing Company WorthVishwajeet_Pat_7360100% (1)

- Classic Knitwear and Guardian - A Perfect FitDocument6 pagesClassic Knitwear and Guardian - A Perfect FitSHRUTI100% (1)

- Does IT Payoff Strategies of Two Banking GiantsDocument10 pagesDoes IT Payoff Strategies of Two Banking GiantsScyfer_16031991No ratings yet

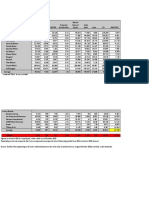

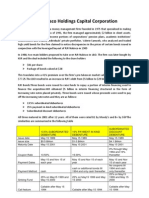

- RJR Nabisco Holdings Capital CorporationDocument3 pagesRJR Nabisco Holdings Capital CorporationManogana RasaNo ratings yet

- Spyder Case Intro: See Templates On Blackboard For WACC and DCF OutputDocument11 pagesSpyder Case Intro: See Templates On Blackboard For WACC and DCF Outputrock sinhaNo ratings yet

- Macro OB Case QuestionsDocument4 pagesMacro OB Case Questionsrock sinhaNo ratings yet

- Question: Consider Country X With A GDP Level of 210.000 and A GrowthDocument2 pagesQuestion: Consider Country X With A GDP Level of 210.000 and A Growthrock sinhaNo ratings yet

- Give Two Examples Where An Indian Company Entering...Document2 pagesGive Two Examples Where An Indian Company Entering...rock sinhaNo ratings yet

- Question: (20 PTS) The Early 1980's: The Early 1980s Were An Exciting TimDocument2 pagesQuestion: (20 PTS) The Early 1980's: The Early 1980s Were An Exciting Timrock sinhaNo ratings yet

- Design Thinking and Innovation at Apple: Think DifferentDocument10 pagesDesign Thinking and Innovation at Apple: Think DifferentWarm PrinceNo ratings yet

- Question: Consider Country X With A GDP Level of 210.000 and A GrowthDocument2 pagesQuestion: Consider Country X With A GDP Level of 210.000 and A Growthrock sinhaNo ratings yet

- Question: (20 PTS) The Early 1980's: The Early 1980s Were An Exciting TimDocument2 pagesQuestion: (20 PTS) The Early 1980's: The Early 1980s Were An Exciting Timrock sinhaNo ratings yet

- Get Set Go - Case StudyDocument1 pageGet Set Go - Case Studyrock sinhaNo ratings yet

- We Are Targeting Schools That Have Many Branches Across The Country and Have A Good Student BaseDocument1 pageWe Are Targeting Schools That Have Many Branches Across The Country and Have A Good Student Baserock sinhaNo ratings yet

- Parleremo Pzfra1Document218 pagesParleremo Pzfra1Lucia FerentNo ratings yet

- EPON ONU with 4FE+WiFi EONU-04WDocument4 pagesEPON ONU with 4FE+WiFi EONU-04WAndres Alberto ParraNo ratings yet

- Calendula EbookDocument12 pagesCalendula EbookCeciliaNo ratings yet

- Day3 PESTLE AnalysisDocument13 pagesDay3 PESTLE AnalysisAmit AgrawalNo ratings yet

- Viennot - 1979 - Spontaneous Reasoning in Elementary DynamicsDocument18 pagesViennot - 1979 - Spontaneous Reasoning in Elementary Dynamicsjumonteiro2000No ratings yet

- Ndeb Bned Reference Texts 2019 PDFDocument11 pagesNdeb Bned Reference Texts 2019 PDFnavroop bajwaNo ratings yet

- 1 MergedDocument93 pages1 MergedAditiNo ratings yet

- Readings On The History and System of The Common Law - Roscoe PoundDocument646 pagesReadings On The History and System of The Common Law - Roscoe PoundpajorocNo ratings yet

- Assessment of Concrete Strength Using Flyash and Rice Husk AshDocument10 pagesAssessment of Concrete Strength Using Flyash and Rice Husk AshNafisul AbrarNo ratings yet

- Quick Reference To Psychotropic Medications: AntidepressantsDocument2 pagesQuick Reference To Psychotropic Medications: AntidepressantsNaiana PaulaNo ratings yet

- Invoice Request for Digitize Global InovasiDocument1 pageInvoice Request for Digitize Global InovasiAsa Arya SudarmanNo ratings yet

- CFPA E Guideline No 2 2013 FDocument39 pagesCFPA E Guideline No 2 2013 Fmexo62No ratings yet

- 2010 - Caliber JEEP BOITE T355Document484 pages2010 - Caliber JEEP BOITE T355thierry.fifieldoutlook.comNo ratings yet

- Biokimia - DR - Maehan Hardjo M.biomed PHDDocument159 pagesBiokimia - DR - Maehan Hardjo M.biomed PHDHerryNo ratings yet

- BW Query GuidelinesDocument10 pagesBW Query GuidelinesyshriniNo ratings yet

- 2746 PakMaster 75XL Plus (O)Document48 pages2746 PakMaster 75XL Plus (O)Samuel ManducaNo ratings yet

- Update 2.9?new Best Sensitivity + Code & Basic Setting Pubg Mobile 2024?gyro On, 60fps, 5 Fingger. - YoutubeDocument1 pageUpdate 2.9?new Best Sensitivity + Code & Basic Setting Pubg Mobile 2024?gyro On, 60fps, 5 Fingger. - Youtubepiusanthony918No ratings yet

- Organic Vapour List PDFDocument1 pageOrganic Vapour List PDFDrGurkirpal Singh MarwahNo ratings yet

- Grammar Notes-February2017 - by Aslinda RahmanDocument41 pagesGrammar Notes-February2017 - by Aslinda RahmanNadia Anuar100% (1)

- Programmer Competency Matrix - Sijin JosephDocument8 pagesProgrammer Competency Matrix - Sijin JosephkikiNo ratings yet

- Sublime Union: A Womans Sexual Odyssey Guided by Mary Magdalene (Book Two of The Magdalene Teachings) Download Free BookDocument4 pagesSublime Union: A Womans Sexual Odyssey Guided by Mary Magdalene (Book Two of The Magdalene Teachings) Download Free Bookflavia cascarinoNo ratings yet

- Course 4Document3 pagesCourse 4Ibrahim SalahudinNo ratings yet

- Gec-Art Art Appreciation: Course Code: Course Title: Course DescriptionsDocument14 pagesGec-Art Art Appreciation: Course Code: Course Title: Course Descriptionspoleene de leonNo ratings yet

- Indigo Vision CatalogDocument117 pagesIndigo Vision CatalogWAEL50% (2)

- Luxand FaceSDK DocumentationDocument117 pagesLuxand FaceSDK DocumentationrdhartzNo ratings yet

- An Improvement in Endodontic Therapy You Will AppreciateDocument2 pagesAn Improvement in Endodontic Therapy You Will AppreciateIs MNo ratings yet

- 41-How To Calculate Air Temp in Unconditioned SpacesDocument3 pages41-How To Calculate Air Temp in Unconditioned Spacesalmig200No ratings yet

- APMP Certification Syllabus and Program V3.1 March 2019 PDFDocument20 pagesAPMP Certification Syllabus and Program V3.1 March 2019 PDFMuhammad ZubairNo ratings yet

- Administration and Supervisory Uses of Test and Measurement - Coronado, Juliet N.Document23 pagesAdministration and Supervisory Uses of Test and Measurement - Coronado, Juliet N.Juliet N. Coronado89% (9)

- Lesson Plan in ESPDocument4 pagesLesson Plan in ESPkaren daculaNo ratings yet