You might also like

- Economic Analysis of India and Industry Analysis of Chemical IndustryDocument28 pagesEconomic Analysis of India and Industry Analysis of Chemical IndustrySharanyaNo ratings yet

- Proposed Report: Public FinancesDocument15 pagesProposed Report: Public FinancesChetan KhannaNo ratings yet

- Fundamental Analysis of TCSDocument15 pagesFundamental Analysis of TCSarupritNo ratings yet

- India Macro Presentation - Reliance Format Final 01Document27 pagesIndia Macro Presentation - Reliance Format Final 01nitesh chhutaniNo ratings yet

- Indian EconomyDocument12 pagesIndian Economyarchana_anuragiNo ratings yet

- Indian Economic Survey 2012Document10 pagesIndian Economic Survey 2012Krunal KeniaNo ratings yet

- Grant Thornton FICCI MSMEDocument76 pagesGrant Thornton FICCI MSMEIshan GuptaNo ratings yet

- State of EconomyDocument21 pagesState of EconomyHarsh KediaNo ratings yet

- KPMG Flash News Economic Survey 2010 11Document10 pagesKPMG Flash News Economic Survey 2010 11Neel GargNo ratings yet

- NagpalDocument21 pagesNagpalthakursahbNo ratings yet

- 2012 Budget PublicationDocument71 pages2012 Budget PublicationPushpa PatilNo ratings yet

- FMCG 1H10 IndustryDocument32 pagesFMCG 1H10 Industrycoolvik87No ratings yet

- Investment and Growth: 1.1 Contribution AnalysisDocument5 pagesInvestment and Growth: 1.1 Contribution AnalysisaoulakhNo ratings yet

- Slowdown of Global Economy Opportunity For India & ChinaDocument13 pagesSlowdown of Global Economy Opportunity For India & ChinaMitul Kirtania50% (2)

- Recent Development in Global Financial MarketDocument8 pagesRecent Development in Global Financial MarketBini MathewNo ratings yet

- Suyash Agarwal Research Report2023Document62 pagesSuyash Agarwal Research Report2023Lucky SrivastavaNo ratings yet

- Current Affairs 2012Document5 pagesCurrent Affairs 2012Indranil MandalNo ratings yet

- 2.1. Economic Analysis:: Boom Recovery Recession Depression Invest DisinvestDocument5 pages2.1. Economic Analysis:: Boom Recovery Recession Depression Invest DisinvestbatkiNo ratings yet

- MSMEs in IndiaDocument3 pagesMSMEs in IndianiyanmiloNo ratings yet

- Unit - 2 IBDocument6 pagesUnit - 2 IBAyush devdaNo ratings yet

- Getting To The Core: Budget AnalysisDocument37 pagesGetting To The Core: Budget AnalysisfaizanbhamlaNo ratings yet

- India Special Report - Assessing The Economic Impact of India's Real Estate Sector - CREDAI CBREDocument20 pagesIndia Special Report - Assessing The Economic Impact of India's Real Estate Sector - CREDAI CBRErealtywatch108No ratings yet

- Assignment On Fundamental Analysis of IdbiDocument11 pagesAssignment On Fundamental Analysis of IdbifiiimpactNo ratings yet

- Challenges and Coners of RbiDocument17 pagesChallenges and Coners of RbiParthiban RajendranNo ratings yet

- LenovoDocument84 pagesLenovoasifanis100% (1)

- GR Eco121Document20 pagesGR Eco121Nguyen Thi Nhung (K16HL)No ratings yet

- Economic Survey 2012Document20 pagesEconomic Survey 2012SandeepBoseNo ratings yet

- Performance ApppraidDocument81 pagesPerformance ApppraidManisha LatiyanNo ratings yet

- State of The Economy 2011Document8 pagesState of The Economy 2011agarwaldipeshNo ratings yet

- Summer Internship Report On LenovoDocument74 pagesSummer Internship Report On Lenovoshimpi244197100% (1)

- Bangladesh Quarterly Economic Update: September 2014From EverandBangladesh Quarterly Economic Update: September 2014No ratings yet

- Year GDPDocument9 pagesYear GDPishwaryaNo ratings yet

- India Union Budget 2013 PWC Analysis BookletDocument40 pagesIndia Union Budget 2013 PWC Analysis BookletsuchjazzNo ratings yet

- Ias Prelim 2011 Current Affairs Notes Economic Survey 2010 11Document13 pagesIas Prelim 2011 Current Affairs Notes Economic Survey 2010 11prashant_kaushal_2No ratings yet

- Bangladesh Quarterly Economic Update - March 2012Document28 pagesBangladesh Quarterly Economic Update - March 2012Asian Development BankNo ratings yet

- Interim Budget Speech of PchidambramDocument14 pagesInterim Budget Speech of PchidambramSankalp KumarNo ratings yet

- Indian EconomyDocument35 pagesIndian EconomyNeeraj ChadawarNo ratings yet

- Chapter 4 Policy ImperativesDocument8 pagesChapter 4 Policy ImperativesRituNo ratings yet

- Economy in The Last DecadeDocument42 pagesEconomy in The Last Decadedcs019No ratings yet

- Economic Slowdown and Macro Economic PoliciesDocument38 pagesEconomic Slowdown and Macro Economic PoliciesRachitaRattanNo ratings yet

- Sector-Wise Contribution of GDP of India: CIA FackbookDocument8 pagesSector-Wise Contribution of GDP of India: CIA FackbookPrakash VadavadagiNo ratings yet

- Indian Economy OverviewDocument3 pagesIndian Economy OverviewAkshar AminNo ratings yet

- GDP: Comparative Analysis: Submitted By: Jerin JoyDocument6 pagesGDP: Comparative Analysis: Submitted By: Jerin JoyJerin JoyNo ratings yet

- Kushal Jesrani 26 Research MethodologyDocument70 pagesKushal Jesrani 26 Research MethodologyKushal JesraniNo ratings yet

- India Market Report-2013Document15 pagesIndia Market Report-2013Chelladurai KrishnasamyNo ratings yet

- Fundamental Analysis of Airtel ReportDocument29 pagesFundamental Analysis of Airtel ReportKoushik G SaiNo ratings yet

- Helping You Spot Opportunities: Investment Update - August, 2013Document55 pagesHelping You Spot Opportunities: Investment Update - August, 2013akcool91No ratings yet

- Economic Growth of India and ChinaDocument4 pagesEconomic Growth of India and Chinaswatiram_622012No ratings yet

- Chapter 1: The Indian Economy: An OverviewDocument14 pagesChapter 1: The Indian Economy: An OverviewJaya NairNo ratings yet

- Fundamental AnalysisDocument8 pagesFundamental AnalysisJithin ManoharNo ratings yet

- Mets September 2010 Ver4Document44 pagesMets September 2010 Ver4bsa375No ratings yet

- Rakesh Mohan NotesDocument3 pagesRakesh Mohan Notesun3709579No ratings yet

- IndiaEconomicGrowth SDocument16 pagesIndiaEconomicGrowth SAmol SaxenaNo ratings yet

- Isc Economics Project 2Document15 pagesIsc Economics Project 2ashmit26007No ratings yet

- Overcoming COVID-19 in Bhutan: Lessons from Coping with the Pandemic in a Tourism-Dependent EconomyFrom EverandOvercoming COVID-19 in Bhutan: Lessons from Coping with the Pandemic in a Tourism-Dependent EconomyNo ratings yet

- Fundamentals of Business Economics Study Resource: CIMA Study ResourcesFrom EverandFundamentals of Business Economics Study Resource: CIMA Study ResourcesNo ratings yet

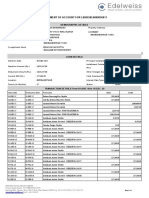

- 16 StatementofAccount LBHBSBL0000036011Document4 pages16 StatementofAccount LBHBSBL0000036011girija mohapatraNo ratings yet

- Genova Matter Opinion and OrderDocument6 pagesGenova Matter Opinion and OrderNewsdayNo ratings yet

- Tax Invoice/ Tax Credit Note: You Can Find More Information On Where and How To Pay Your Bill byDocument42 pagesTax Invoice/ Tax Credit Note: You Can Find More Information On Where and How To Pay Your Bill byahsanukkakarNo ratings yet

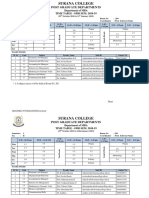

- Post Graduate Departments: Department of MBA Time Table - Odd Sem. 2018-19Document2 pagesPost Graduate Departments: Department of MBA Time Table - Odd Sem. 2018-19Divakar GowdaNo ratings yet

- Module 4-Operating, Financial, and Total LeverageDocument45 pagesModule 4-Operating, Financial, and Total LeverageAna ValenovaNo ratings yet

- Financial Reporting Standards CouncilDocument6 pagesFinancial Reporting Standards CouncilFrancis Jerome Cuarteros0% (1)

- Mutual Funds in IndiaDocument66 pagesMutual Funds in IndiaUtsav ThakkarNo ratings yet

- Contract Sounds and LightsDocument2 pagesContract Sounds and LightsHosting by Miss RuthNo ratings yet

- Pre Issue ManagementDocument19 pagesPre Issue Managementbs_sharathNo ratings yet

- Property, Plant and Equipment (IAS-16)Document2 pagesProperty, Plant and Equipment (IAS-16)Raneem BilalNo ratings yet

- Assignment FMDocument2 pagesAssignment FMKartik AhirNo ratings yet

- 10 Steps To Building A Winning Trading Plan PDFDocument8 pages10 Steps To Building A Winning Trading Plan PDFscreen1 record100% (1)

- Continental CarriersDocument10 pagesContinental Carriersnipun9143No ratings yet

- Money & BankingDocument46 pagesMoney & BankingAbdihakimNo ratings yet

- As Per Annexure Attached: MF DRF (Destatementization Request Form)Document3 pagesAs Per Annexure Attached: MF DRF (Destatementization Request Form)Mutual Fund JunctionNo ratings yet

- Dubai Islamic Bank January June 2021 SOCDocument26 pagesDubai Islamic Bank January June 2021 SOCAD ADNo ratings yet

- Full Download Test Bank For Auditing The Art and Science of Assurance Engagements Fourteenth Canadian Edition Plus Mylab Accounting With Pearson Etext Package 14th Edition PDF Full ChapterDocument36 pagesFull Download Test Bank For Auditing The Art and Science of Assurance Engagements Fourteenth Canadian Edition Plus Mylab Accounting With Pearson Etext Package 14th Edition PDF Full Chaptersiccaganoiddz6x100% (15)

- Acctng ProcessDocument4 pagesAcctng ProcessElaine YapNo ratings yet

- Numerology by MonthDocument8 pagesNumerology by Monthmaurice bertrandNo ratings yet

- 100 149 PDFDocument53 pages100 149 PDFSamuelNo ratings yet

- Investor PPPDocument43 pagesInvestor PPPGeraldNo ratings yet

- Energy Summit SampleDocument10 pagesEnergy Summit SampleVikramNo ratings yet

- CAIIB BRBL Marathon 1 PDF by ABDocument32 pagesCAIIB BRBL Marathon 1 PDF by ABAkshay SathianNo ratings yet

- Anatomy of A Stock PitchDocument15 pagesAnatomy of A Stock Pitchadm2143No ratings yet

- Partnership Accounts FormatDocument7 pagesPartnership Accounts FormatJamsheed Rasheed100% (1)

- Financial CIMA F3 CalculationsDocument23 pagesFinancial CIMA F3 CalculationsQasim DhillonNo ratings yet

- Report of The President B/A Keith D. Hill OCTOBER 2021Document29 pagesReport of The President B/A Keith D. Hill OCTOBER 2021Chicago Transit Justice CoalitionNo ratings yet

- Per Capita Income of BangladeshDocument5 pagesPer Capita Income of BangladeshRain StarNo ratings yet

- MERU SPORTS FIELDS BLANK BOQ FOR TENDER Main Works PDFDocument381 pagesMERU SPORTS FIELDS BLANK BOQ FOR TENDER Main Works PDFMADUHU KISUJA100% (1)

- BOLIVIA-BRAZIL GAS PIPELINE ReportDocument6 pagesBOLIVIA-BRAZIL GAS PIPELINE ReportnelsonmcamachoNo ratings yet