0% found this document useful (0 votes)

106 views2 pagesOption Greeks Calculation Tool

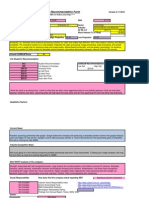

This document provides inputs and outputs for calculating option Greeks. It allows the user to input either an option price or implied volatility. Given the inputs, it will calculate the common Greeks - delta, gamma, theta, vega, and rho - for the option. The document was last updated on April 16, 2005 to fix a math error involving the risk-free interest rate.

Uploaded by

shiva19892006Copyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as XLS, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

106 views2 pagesOption Greeks Calculation Tool

This document provides inputs and outputs for calculating option Greeks. It allows the user to input either an option price or implied volatility. Given the inputs, it will calculate the common Greeks - delta, gamma, theta, vega, and rho - for the option. The document was last updated on April 16, 2005 to fix a math error involving the risk-free interest rate.

Uploaded by

shiva19892006Copyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as XLS, PDF, TXT or read online on Scribd