You might also like

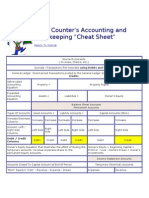

- Accounting Cheat SheetDocument7 pagesAccounting Cheat Sheetopty100% (16)

- Cheat Sheet Exam 1Document1 pageCheat Sheet Exam 1Shashi Gavini Keil100% (2)

- Becker CPA BEC Review CheatsheetDocument6 pagesBecker CPA BEC Review CheatsheetGabrielNo ratings yet

- Basic Everyday Journal EntriesDocument2 pagesBasic Everyday Journal EntriesMary73% (15)

- Finance Cheat SheetDocument2 pagesFinance Cheat SheetMarc MNo ratings yet

- Inbm 110 - Accounts Study Sheet: Chapter 1 & 2Document5 pagesInbm 110 - Accounts Study Sheet: Chapter 1 & 2Laura TaiNo ratings yet

- Closing Journal EntriesDocument1 pageClosing Journal EntriesMary91% (11)

- Schaum's Outline of Bookkeeping and Accounting, Fourth EditionFrom EverandSchaum's Outline of Bookkeeping and Accounting, Fourth EditionRating: 5 out of 5 stars5/5 (1)

- General Accounting Cheat SheetDocument35 pagesGeneral Accounting Cheat SheetZee Drake100% (6)

- Final Report InternshipDocument17 pagesFinal Report InternshipSAMARTH UPADHYAYANo ratings yet

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- Cheat Sheet For AccountingDocument4 pagesCheat Sheet For AccountingshihuiNo ratings yet

- Cheat Sheet Final - FMVDocument3 pagesCheat Sheet Final - FMVhanifakih100% (2)

- CorpFinance Cheat Sheet v2.2Document2 pagesCorpFinance Cheat Sheet v2.2subtle69100% (4)

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- What is Financial Accounting and BookkeepingFrom EverandWhat is Financial Accounting and BookkeepingRating: 4 out of 5 stars4/5 (10)

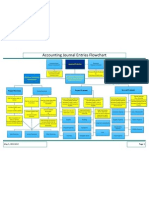

- Accounting Journal Entries Flowchart PDFDocument1 pageAccounting Journal Entries Flowchart PDFMary75% (4)

- Fnce 100 Final Cheat SheetDocument2 pagesFnce 100 Final Cheat SheetToby Arriaga100% (2)

- Intermediate Accounting 1: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 1: a QuickStudy Digital Reference GuideNo ratings yet

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- Accounting and Finance Formulas: A Simple IntroductionFrom EverandAccounting and Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- CheatDocument1 pageCheatIshmo KueedNo ratings yet

- Accounting Cheat SheetDocument2 pagesAccounting Cheat Sheetanoushes1100% (2)

- ACCT 101 Cheat SheetDocument1 pageACCT 101 Cheat SheetAndrea NingNo ratings yet

- Cheat Sheet For Financial AccountingDocument1 pageCheat Sheet For Financial Accountingmikewu101No ratings yet

- Accounting NotesDocument66 pagesAccounting NotesShashank Gadia71% (17)

- Fin Cheat SheetDocument3 pagesFin Cheat SheetChristina RomanoNo ratings yet

- FAR NotesDocument163 pagesFAR NotesClaire Antonette Limpangog100% (2)

- Learn Your Accounting Basics - A Step by Step Approach: Junior High School and beginners, #1From EverandLearn Your Accounting Basics - A Step by Step Approach: Junior High School and beginners, #1Rating: 1.5 out of 5 stars1.5/5 (2)

- General Accounting Cheat SheetDocument35 pagesGeneral Accounting Cheat Sheetazulceleste0_0100% (1)

- BEC Notes Chapter 3Document6 pagesBEC Notes Chapter 3cpacfa90% (10)

- Kelly's Finance Cheat Sheet V6Document2 pagesKelly's Finance Cheat Sheet V6Kelly Koh100% (4)

- Account ClassificationDocument2 pagesAccount ClassificationMary96% (23)

- Book of Facts by Isaac AsimovDocument158 pagesBook of Facts by Isaac AsimovMD. Monzurul Karim ShanchayNo ratings yet

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- Accounting Cheat Sheet FinalsDocument5 pagesAccounting Cheat Sheet FinalsRahel Charikar100% (1)

- Accounting Cheat SheetsDocument4 pagesAccounting Cheat SheetsGreg BealNo ratings yet

- ACC1002X Cheat Sheet 2Document1 pageACC1002X Cheat Sheet 2jieboNo ratings yet

- Accouting Finals Cheat SheetDocument1 pageAccouting Finals Cheat SheetpinkrocketNo ratings yet

- Financial Accounting: Tools For Business Decision-Making, Third Canadian EditionDocument6 pagesFinancial Accounting: Tools For Business Decision-Making, Third Canadian Editionapi-19743565100% (1)

- BEC CPA Formulas - November 2015 - Becker CPA ReviewDocument20 pagesBEC CPA Formulas - November 2015 - Becker CPA Reviewgavka100% (1)

- General Accounting Cheat SheetDocument35 pagesGeneral Accounting Cheat SheetHectorNo ratings yet

- Accounting Cheat SheetDocument2 pagesAccounting Cheat SheetvgirotraNo ratings yet

- Class of AccountsDocument5 pagesClass of AccountssalynnaNo ratings yet

- Accounting GuideDocument153 pagesAccounting Guidebam04100% (1)

- Basics of AccountingDocument20 pagesBasics of AccountingvirtualNo ratings yet

- Expressed As A Percentage of The Value of Revenue or Sales.: Balance Sheet: Reports What The Organization Owns and OwesDocument3 pagesExpressed As A Percentage of The Value of Revenue or Sales.: Balance Sheet: Reports What The Organization Owns and OwesDGNo ratings yet

- Cheat Sheet - Financial STDocument2 pagesCheat Sheet - Financial STMohammad DaulehNo ratings yet

- Basic Accounting Concepts - GE AccountingDocument62 pagesBasic Accounting Concepts - GE AccountingTarun ChawlaNo ratings yet

- Cheat Sheet - AccountingDocument2 pagesCheat Sheet - AccountingJeffery KaoNo ratings yet

- Midterm Cheat SheetDocument4 pagesMidterm Cheat SheetvikasNo ratings yet

- The Everything Accounting Book: Balance Your Budget, Manage Your Cash Flow, And Keep Your Books in the BlackFrom EverandThe Everything Accounting Book: Balance Your Budget, Manage Your Cash Flow, And Keep Your Books in the BlackRating: 1 out of 5 stars1/5 (1)

- BEC Notes Chapter 3Document13 pagesBEC Notes Chapter 3bobby100% (1)

- Financial Accounting Is The Process of Preparing Financial Statements For A BusinessDocument11 pagesFinancial Accounting Is The Process of Preparing Financial Statements For A Businesshemanth727100% (1)

- The Holy AL-Quran (Bengali Translation)Document701 pagesThe Holy AL-Quran (Bengali Translation)MD. Monzurul Karim ShanchayNo ratings yet

- Best Stories of The Quran-Part 3Document244 pagesBest Stories of The Quran-Part 3MD. Monzurul Karim Shanchay100% (1)

- News Writting and Editing-Sikandar FayezDocument190 pagesNews Writting and Editing-Sikandar FayezMD. Monzurul Karim ShanchayNo ratings yet

- The Treasures of Good DeedsDocument24 pagesThe Treasures of Good DeedsMD. Monzurul Karim Shanchay100% (1)

- Mirza Galib's PoetryDocument93 pagesMirza Galib's PoetryMD. Monzurul Karim ShanchayNo ratings yet

- Regular Irregularities-Hanif SanketDocument75 pagesRegular Irregularities-Hanif SanketMD. Monzurul Karim ShanchayNo ratings yet

- Entire Travel-Humayun AhmedDocument360 pagesEntire Travel-Humayun AhmedMD. Monzurul Karim Shanchay100% (1)

- Bengali Grammar by Jyotibhusan ChakiDocument309 pagesBengali Grammar by Jyotibhusan ChakiMD. Monzurul Karim Shanchay100% (2)

- Thinking and Writing From Word To Sentence To Paragraph To EssayDocument238 pagesThinking and Writing From Word To Sentence To Paragraph To EssayMD. Monzurul Karim Shanchay50% (2)

- Sustho Deho Prashanto MonDocument210 pagesSustho Deho Prashanto MonmamunngsNo ratings yet

- Kidney DiseasesDocument136 pagesKidney DiseasesMD. Monzurul Karim ShanchayNo ratings yet

- Bengali Grammar-Exam. PreparationDocument43 pagesBengali Grammar-Exam. PreparationMD. Monzurul Karim Shanchay100% (2)

- Learning The Holy AL-QuranDocument128 pagesLearning The Holy AL-QuranMD. Monzurul Karim ShanchayNo ratings yet

- ShortCut MathDocument299 pagesShortCut MathMD. Monzurul Karim Shanchay100% (3)

- Allah's Names and AttributesDocument256 pagesAllah's Names and AttributesMD. Monzurul Karim ShanchayNo ratings yet

- Advanced Learner's Functional EnglishDocument448 pagesAdvanced Learner's Functional EnglishMD. Monzurul Karim Shanchay88% (8)

- Kalimatus ShahadahDocument98 pagesKalimatus ShahadahMD. Monzurul Karim Shanchay100% (1)

- Women's Prayer PDFDocument98 pagesWomen's Prayer PDFMD. Monzurul Karim ShanchayNo ratings yet

- Market Structure-Perfect CompetitionDocument72 pagesMarket Structure-Perfect CompetitionUtsav AaryaNo ratings yet

- Answer Key Far Assessment Questionairre 1Document22 pagesAnswer Key Far Assessment Questionairre 1Johnfree VallinasNo ratings yet

- ZAFRA Hannah Mae S. Income Statement and Balance Sheet Ferna CompanyDocument2 pagesZAFRA Hannah Mae S. Income Statement and Balance Sheet Ferna CompanyAngeliePanerioGonzagaNo ratings yet

- Solution Manual For Advanced Accounting 13Th Edition Beams Anthony Bettinghaus Smith 0134472144 9780134472140 Full Chapter PDFDocument30 pagesSolution Manual For Advanced Accounting 13Th Edition Beams Anthony Bettinghaus Smith 0134472144 9780134472140 Full Chapter PDFrose.carvin242100% (11)

- Ratio Analysis: Ratio Analysis Is The Process of Establishing and Interpreting Various RatiosDocument26 pagesRatio Analysis: Ratio Analysis Is The Process of Establishing and Interpreting Various RatiosTarpan Mannan100% (2)

- E-Commerce UNIT-1Document12 pagesE-Commerce UNIT-1Bhavan YadavNo ratings yet

- Intenship Project Omkar Sir Final 2Document20 pagesIntenship Project Omkar Sir Final 2Saurabh KumbharNo ratings yet

- Credit Memo - MH3M300182Document1 pageCredit Memo - MH3M300182AltafNo ratings yet

- Assignment Kinetic Honda Case Study Consumer Buying JourneyDocument3 pagesAssignment Kinetic Honda Case Study Consumer Buying JourneyAnnu ChandraNo ratings yet

- Revenue RecognitionDocument8 pagesRevenue RecognitionSedrick ChiongNo ratings yet

- Hul Lime IimiDocument25 pagesHul Lime Iimirsriram84No ratings yet

- Lat TakeDocument8 pagesLat TakeCamila Gail GumbanNo ratings yet

- Strategic ManagementDocument56 pagesStrategic Managementobsinan dejene100% (3)

- The Merit Corporation IDocument2 pagesThe Merit Corporation IMOHIT MALVIYA PGP 2020 BatchNo ratings yet

- A Construction Company Entered Into A FixedDocument40 pagesA Construction Company Entered Into A FixedDiaиa Diaz50% (2)

- Organization Chart - Marketing 2017 (Rev 5)Document2 pagesOrganization Chart - Marketing 2017 (Rev 5)Nam CHNo ratings yet

- Mas MCQDocument13 pagesMas MCQIm In TroubleNo ratings yet

- Main Cirque Du Soleil FinalDocument4 pagesMain Cirque Du Soleil FinalFarhan HossainNo ratings yet

- Connor Med SystemsDocument5 pagesConnor Med SystemsAndrii DutchakNo ratings yet

- Sample Client: CLS Investments, LLC Is Independent of Your Advisor's Broker/dealer And/or Registered Investment AdvisorDocument15 pagesSample Client: CLS Investments, LLC Is Independent of Your Advisor's Broker/dealer And/or Registered Investment AdvisorLaskar PejuangNo ratings yet

- Wellhead Procurement StrategyDocument2 pagesWellhead Procurement StrategyYougchu LuanNo ratings yet

- A Study On Customer Satisfaction of FMCG in Pathanjali ProductsDocument13 pagesA Study On Customer Satisfaction of FMCG in Pathanjali ProductseswariNo ratings yet

- Test Bank For Advertising Imc Principles and Practice 10e by Moriarty 0133763536Document44 pagesTest Bank For Advertising Imc Principles and Practice 10e by Moriarty 0133763536JeremySotofmwa100% (43)

- Chapter 6 Test: InventoriesDocument129 pagesChapter 6 Test: InventoriesQueen Nikki MinajNo ratings yet

- A021221078 - Akuntansi Dasar Pekan 5Document2 pagesA021221078 - Akuntansi Dasar Pekan 5Nazwa AuliaNo ratings yet

- Absorption Vs Marginal CostingDocument24 pagesAbsorption Vs Marginal CostingPoint BlankNo ratings yet

- Quiz 1 SolutionsDocument5 pagesQuiz 1 Solutionsgovt2No ratings yet

- 5 - DepreciationDocument22 pages5 - Depreciationnhel estalloNo ratings yet

- Marketing Plan TemplateDocument9 pagesMarketing Plan TemplateAzeb SeidNo ratings yet