You might also like

- Ebook How To Design and Evaluate Research in Education 11Th Edition PDF Full Chapter PDFDocument67 pagesEbook How To Design and Evaluate Research in Education 11Th Edition PDF Full Chapter PDFwayne.edwardson742100% (25)

- Alex Sharpe's PortfolioDocument3 pagesAlex Sharpe's PortfolioSiona Maria NathanielNo ratings yet

- PV Plant ControlDocument19 pagesPV Plant Controlhumberto ceballosNo ratings yet

- Case 100 Pressed Paper DirectedDocument8 pagesCase 100 Pressed Paper DirectedHaidar Ismail0% (1)

- Math 100 Detailed Course OutlineDocument2 pagesMath 100 Detailed Course OutlineDiyanika100% (1)

- Hedge Fund Modelling and Analysis Using Excel and VBA: WorksheetsDocument6 pagesHedge Fund Modelling and Analysis Using Excel and VBA: WorksheetsmarcoNo ratings yet

- AMOS Business Suite Vrs. 10.1.00 Getting Started User GuideDocument35 pagesAMOS Business Suite Vrs. 10.1.00 Getting Started User GuideAttrapezioNo ratings yet

- Matriz de Cotización de Precios de Cierre: Date Toyrus Bank of A PepsicoDocument7 pagesMatriz de Cotización de Precios de Cierre: Date Toyrus Bank of A PepsicoRogerNo ratings yet

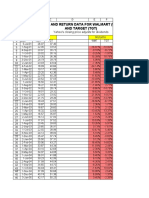

- Price and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsDocument13 pagesPrice and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsArisha KhanNo ratings yet

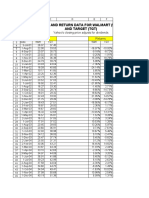

- Price and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsDocument19 pagesPrice and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsSyed Ameer Ali ShahNo ratings yet

- Alex Sharpe CaseDocument17 pagesAlex Sharpe Casemusunna galibNo ratings yet

- Alex Sharpe 1Document4 pagesAlex Sharpe 1Twisha Priya100% (1)

- TRK - ResultadosDocument37 pagesTRK - ResultadosFirst MídiaNo ratings yet

- Single Index ModelDocument3 pagesSingle Index ModelMemo NerNo ratings yet

- HC Investimentos - HedgeDocument11 pagesHC Investimentos - HedgeFabiano MorattiNo ratings yet

- VIDF - Monthly Returns May 2017Document2 pagesVIDF - Monthly Returns May 2017Ashwin HasyagarNo ratings yet

- Date Indiacpi Uscpi Inflation Differential Repoindia UsfedrateDocument7 pagesDate Indiacpi Uscpi Inflation Differential Repoindia UsfedrateRohan ShankpalNo ratings yet

- Crude Oil BrentDocument4 pagesCrude Oil BrentRoberto MartiasNo ratings yet

- Trabajo Listo Carteras ListasDocument49 pagesTrabajo Listo Carteras ListasSantiago SanchezNo ratings yet

- Average Monthly Returns: Date S&P 500 3 Month T-Bill RJR HasbroDocument16 pagesAverage Monthly Returns: Date S&P 500 3 Month T-Bill RJR HasbroKing CheungNo ratings yet

- HC Investimentos IBOV SMLL DiversificaçãoDocument7 pagesHC Investimentos IBOV SMLL DiversificaçãoFabiano MorattiNo ratings yet

- Excel Lecture 3a - SolvedDocument22 pagesExcel Lecture 3a - SolvedRimpy SondhNo ratings yet

- % Var - Mastercard: Gráfico de BetaDocument16 pages% Var - Mastercard: Gráfico de BetaMario RefNo ratings yet

- 02 Alex Sharpe - PreclassDocument11 pages02 Alex Sharpe - PreclassVijeta KatariaNo ratings yet

- Alex Case StudyDocument4 pagesAlex Case StudyPratiksha GhosalNo ratings yet

- Efficient FrontiersDocument10 pagesEfficient FrontiersMuhammad Ahsan MukhtarNo ratings yet

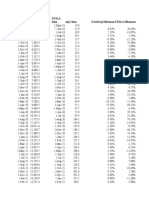

- Regression Beta of TeslaDocument5 pagesRegression Beta of TeslaNikhil AnantNo ratings yet

- HC Investimentos - Como Calcular A Correlação Entre InvestimentosDocument7 pagesHC Investimentos - Como Calcular A Correlação Entre InvestimentosMario Sergio GouveaNo ratings yet

- Ejercicio Portafolio Óptimo A (DESARROLLO)Document5 pagesEjercicio Portafolio Óptimo A (DESARROLLO)Valeria MaldonadoNo ratings yet

- Date S&P500 Aapl MSFT BAC XOM PFE Month TDocument17 pagesDate S&P500 Aapl MSFT BAC XOM PFE Month TZeynep DerinözNo ratings yet

- WACCDocument18 pagesWACCaditya chandNo ratings yet

- Fin RatiosDocument7 pagesFin Ratiosakankshag_13No ratings yet

- Alex Sharpe S PortfolioDocument3 pagesAlex Sharpe S Portfolionishnath satyaNo ratings yet

- Fase Planeado Actual Ingenieria de Detalle Suministro de Equipos Y Materiales Construccion Progreso de ProyectoDocument26 pagesFase Planeado Actual Ingenieria de Detalle Suministro de Equipos Y Materiales Construccion Progreso de ProyectoArturo Saenz ArteagaNo ratings yet

- Nuevo Hoja de Cálculo de Microsoft ExcelDocument14 pagesNuevo Hoja de Cálculo de Microsoft ExcelMarcelo SalasNo ratings yet

- MF Risk CalculationDocument10 pagesMF Risk CalculationBhaskar RawatNo ratings yet

- Alex Sharp's PortfolioDocument6 pagesAlex Sharp's PortfolioFurqanTariqNo ratings yet

- Final DataDocument66 pagesFinal DataDilshadNo ratings yet

- Grasim Industries LTD.: Group HeadDocument4 pagesGrasim Industries LTD.: Group Headsanchit bhasinNo ratings yet

- Efficient Frontier: Month HDFC TCS % Return TCS % Return HDFC HDFC TCS RP S.D Portfolio Mix (W)Document1 pageEfficient Frontier: Month HDFC TCS % Return TCS % Return HDFC HDFC TCS RP S.D Portfolio Mix (W)Rajarshi DaharwalNo ratings yet

- Date S&P500 Aapl MSFT BAC XOM PFE Correlation MatrixDocument14 pagesDate S&P500 Aapl MSFT BAC XOM PFE Correlation MatrixZeynep DerinözNo ratings yet

- Beta Management CorpDocument11 pagesBeta Management CorpKaneez FatimaNo ratings yet

- Escritorio Retornos IpsaDocument2 pagesEscritorio Retornos IpsaJoaquinDesriviersNo ratings yet

- Plan Vs ActDocument1 pagePlan Vs Actsyednehal21No ratings yet

- Fin Mod AssignmentDocument1 pageFin Mod Assignmentsabariaz5309No ratings yet

- Select-Special-F5-Exercise - SolvedDocument3 pagesSelect-Special-F5-Exercise - SolvedShubham GuptaNo ratings yet

- EJERICICIO 3 - Valor en Riesgo (VAR) - SEMANA 12Document299 pagesEJERICICIO 3 - Valor en Riesgo (VAR) - SEMANA 12aidaNo ratings yet

- 2017 Alex Sharpes Portfolio FSDocument2 pages2017 Alex Sharpes Portfolio FSWilson Jose Soto De LeonNo ratings yet

- Beta Management SolutionDocument5 pagesBeta Management SolutionMuhammad IlyasNo ratings yet

- Beta Management Company r2Document17 pagesBeta Management Company r2Yash AgarwalNo ratings yet

- Sumativa 1 Exp 2 FinDocument14 pagesSumativa 1 Exp 2 FinRoger Danilo Lujan ArmasNo ratings yet

- Plano Do MilhãoDocument22 pagesPlano Do Milhãoindi.queirozNo ratings yet

- ABEV3 BetaDocument23 pagesABEV3 BetaFlathon CardosoNo ratings yet

- Trabajo de MacrooDocument5 pagesTrabajo de MacrooMiracle -No ratings yet

- Fast Scrolling Exercise SolvedDocument16 pagesFast Scrolling Exercise SolvedAnil Kumar AkNo ratings yet

- Corporate Finance ProjectDocument12 pagesCorporate Finance ProjectKanishk SinghNo ratings yet

- Beta Management Company: Case DetailsDocument6 pagesBeta Management Company: Case DetailsAninda DuttaNo ratings yet

- Ch8 VaRCVaROptDocument229 pagesCh8 VaRCVaROptvaskoreNo ratings yet

- Plano Do MilhãoDocument24 pagesPlano Do MilhãoEmerson TorresNo ratings yet

- Descri TivaDocument6 pagesDescri TivaAriani FotNo ratings yet

- WoW TrendDocument5 pagesWoW TrendidinuvNo ratings yet

- 03 24 Select Special F5 SolvedDocument3 pages03 24 Select Special F5 SolvedRakaNo ratings yet

- اسايمنت المحافظ معاوية مسلمانيDocument25 pagesاسايمنت المحافظ معاوية مسلمانيMemo NerNo ratings yet

- Potfolio ManagementDocument3 pagesPotfolio Managementsomya guptaNo ratings yet

- Unit Root & Augmented Dickey-Fuller (ADF) Test: How To Check Whether The Given Time Series Is Stationary or Integrated?Document15 pagesUnit Root & Augmented Dickey-Fuller (ADF) Test: How To Check Whether The Given Time Series Is Stationary or Integrated?Haidar IsmailNo ratings yet

- Adding Getformula To Your WorkbookDocument1 pageAdding Getformula To Your WorkbookHaidar IsmailNo ratings yet

- Correlation Matrix FunctionDocument1 pageCorrelation Matrix FunctionHaidar IsmailNo ratings yet

- Case SolutionDocument4 pagesCase SolutionHaidar IsmailNo ratings yet

- Review Test Submission CH 1Document13 pagesReview Test Submission CH 1Haidar IsmailNo ratings yet

- St. John's University Student Managed Investment Fund Investment ResearchDocument17 pagesSt. John's University Student Managed Investment Fund Investment ResearchHaidar IsmailNo ratings yet

- Derivatives Market Mohammad Ismail HaidarDocument12 pagesDerivatives Market Mohammad Ismail HaidarHaidar IsmailNo ratings yet

- Chapter 01Document4 pagesChapter 01Haidar IsmailNo ratings yet

- Fritz - Cherubin02@stjohns - Edu Jillian - Negron02@stjohns - Edu Jabar - Smith02@stjohns - EduDocument36 pagesFritz - Cherubin02@stjohns - Edu Jillian - Negron02@stjohns - Edu Jabar - Smith02@stjohns - EduHaidar IsmailNo ratings yet

- Case 42 West Coast DirectedDocument6 pagesCase 42 West Coast DirectedHaidar IsmailNo ratings yet

- Case 42 West Coast DirectedDocument6 pagesCase 42 West Coast DirectedHaidar IsmailNo ratings yet

- Year Beginning Amount Payment Interest Repayment of Principle Ending BalanceDocument6 pagesYear Beginning Amount Payment Interest Repayment of Principle Ending BalanceHaidar IsmailNo ratings yet

- Decision Making in An Integrated Business Process Context: Learning Using An ERP Simulation GameDocument2 pagesDecision Making in An Integrated Business Process Context: Learning Using An ERP Simulation GameHaidar IsmailNo ratings yet

- Case 75 The Western Co DirectedDocument10 pagesCase 75 The Western Co DirectedHaidar IsmailNo ratings yet

- Climatic Subdivisions in Saudi Arabia: An Application of Principal Component AnalysisDocument17 pagesClimatic Subdivisions in Saudi Arabia: An Application of Principal Component AnalysisirfanNo ratings yet

- Magnetic and Gravity Toolface and How To Interpret The Meaning For Directional Drilling - PDFDocument17 pagesMagnetic and Gravity Toolface and How To Interpret The Meaning For Directional Drilling - PDFHeberth DesbloqueoNo ratings yet

- Arduino SARA-R4 DataSheet (UBX-16024152)Document43 pagesArduino SARA-R4 DataSheet (UBX-16024152)abdullahNo ratings yet

- Implementation of Integrated OBD-II Connector Whith External NetworkDocument7 pagesImplementation of Integrated OBD-II Connector Whith External NetworkKelvin PárragaNo ratings yet

- qt5 Cadaques PDFDocument263 pagesqt5 Cadaques PDFAndré CastroNo ratings yet

- KR C1 A: Technical DataDocument11 pagesKR C1 A: Technical Dataayxworks eurobotsNo ratings yet

- Edexcel IGCSE Unit 2E Homeostasis and Excretion - Self-Assessment SheetDocument6 pagesEdexcel IGCSE Unit 2E Homeostasis and Excretion - Self-Assessment SheetAli ALEBRAHIMNo ratings yet

- District Reading Monitoring and EvaluationDocument8 pagesDistrict Reading Monitoring and EvaluationMerafe Ebreo AluanNo ratings yet

- Gas Detection and Mapping Using An Autonomous Mobile Robot: September 2015Document7 pagesGas Detection and Mapping Using An Autonomous Mobile Robot: September 2015Jake StorageNo ratings yet

- Automated Zone Speci C Irrigation With Wireless Sensor Actuator Network and Adaptable Decision SupportDocument28 pagesAutomated Zone Speci C Irrigation With Wireless Sensor Actuator Network and Adaptable Decision SupportNakal Hans Beta VersionNo ratings yet

- Phy 308 Electronics IDocument310 pagesPhy 308 Electronics ISuresh LNo ratings yet

- Extended AbstractDocument10 pagesExtended AbstractSarang GohNo ratings yet

- Basic Data Science Interview QuestionsDocument18 pagesBasic Data Science Interview QuestionsRamesh kNo ratings yet

- PVGIS-5 GridConnectedPV 46.047 14.545 Undefined Crystsi 0.6kWp 15 90deg 0deg-1Document1 pagePVGIS-5 GridConnectedPV 46.047 14.545 Undefined Crystsi 0.6kWp 15 90deg 0deg-1FinanceNo ratings yet

- Segmented Shaft Seal Brochure Apr 08Document4 pagesSegmented Shaft Seal Brochure Apr 08Zohaib AnserNo ratings yet

- PROBABILITY It Is A Numerical Measure Which Indicates The ChanceDocument20 pagesPROBABILITY It Is A Numerical Measure Which Indicates The ChancePolice stationNo ratings yet

- Frictional Properties of Textile FiberDocument8 pagesFrictional Properties of Textile FiberMD Nazrul IslamNo ratings yet

- Math 115 Uiuc Written Homework 6 SolutionsDocument4 pagesMath 115 Uiuc Written Homework 6 Solutionsafmspqvdy100% (1)

- CSWIP 3 1 PracticalDocument4 pagesCSWIP 3 1 PracticalAhmed Al-Emarah100% (1)

- Formatting Numbers, Currency, and Percents in VB: ThevbprogramerDocument5 pagesFormatting Numbers, Currency, and Percents in VB: ThevbprogramerNoldy SinsuNo ratings yet

- SBA5089ZDocument6 pagesSBA5089ZFrancisca Iniesta TortosaNo ratings yet

- CompletionDocument128 pagesCompletionMelgie Mae Matulin DikitananNo ratings yet

- Burnishing Is A Process by Which A Smooth Hard Tool (UsingDocument9 pagesBurnishing Is A Process by Which A Smooth Hard Tool (UsingΒασίλης ΜπουντιούκοςNo ratings yet

- Physical: MetallurgyDocument4 pagesPhysical: MetallurgySanjanaNo ratings yet

- Quantitative Analysis 1Document20 pagesQuantitative Analysis 1FirdoseNo ratings yet

- Ibm Rs G8124eDocument40 pagesIbm Rs G8124edanibrbNo ratings yet