You might also like

- Course Name: Course Code: EC Examiner: Number of Credits: 7,5 Credits Date of Exam: Examination Time: 3 HoursDocument2 pagesCourse Name: Course Code: EC Examiner: Number of Credits: 7,5 Credits Date of Exam: Examination Time: 3 HoursPetter AndreassonNo ratings yet

- Assessment Case Paper Analysis / Tutorialoutlet Dot ComDocument37 pagesAssessment Case Paper Analysis / Tutorialoutlet Dot Comjorge0048No ratings yet

- 2306xi B s2 EconomicsDocument5 pages2306xi B s2 EconomicsSoniya Omir VijanNo ratings yet

- April 2020 Examinations UG PG FinalTime TableDocument19 pagesApril 2020 Examinations UG PG FinalTime TablePanthalaraja JagaaNo ratings yet

- Project Final Marking SchemeDocument2 pagesProject Final Marking SchemejaldesaNo ratings yet

- Midterm1 2016-02-16 SolutionsDocument10 pagesMidterm1 2016-02-16 SolutionskahwahcheongNo ratings yet

- Practical List Solution (DBMS) LabDocument12 pagesPractical List Solution (DBMS) Labjaypal_mca71% (7)

- Test 2 Chapters 4-7Document10 pagesTest 2 Chapters 4-7GauravNo ratings yet

- Grade X Sample Paper IIDocument6 pagesGrade X Sample Paper IIbekar1012No ratings yet

- Dwnload Full Financial Management For Public Health and Not For Profit Organizations 3rd Edition Finkler Test Bank PDFDocument11 pagesDwnload Full Financial Management For Public Health and Not For Profit Organizations 3rd Edition Finkler Test Bank PDFbenboydr8pl100% (12)

- Solved Assignment Online - 5Document18 pagesSolved Assignment Online - 5Prof Olivia0% (1)

- BUS101 Final Exam Summer - FTHE - 2020 (Ver B) - QuestionsDocument16 pagesBUS101 Final Exam Summer - FTHE - 2020 (Ver B) - QuestionsSHAMRAIZKHAN0% (1)

- Sce Application FormDocument4 pagesSce Application Formsegolame.kelatlhilwe9750% (2)

- Ms-8 Solved PapersDocument6 pagesMs-8 Solved Papersexsonu0% (1)

- 1cecoOD 13 11 2023Document1 page1cecoOD 13 11 2023corraljaNo ratings yet

- Data Interpretation Guide For All Competitive and Admission ExamsFrom EverandData Interpretation Guide For All Competitive and Admission ExamsRating: 2.5 out of 5 stars2.5/5 (6)

- Assignment #3 - Asset AllocationDocument1 pageAssignment #3 - Asset AllocationMaria KianiNo ratings yet

- $R1R10S7Document16 pages$R1R10S7aaaawfdwaedNo ratings yet

- Betting on Horses - Utilising Price Changes for ProfitFrom EverandBetting on Horses - Utilising Price Changes for ProfitRating: 1 out of 5 stars1/5 (1)

- Textile industry import export questionnaireDocument5 pagesTextile industry import export questionnaireAteeq Ur RehmanNo ratings yet

- Sero We 2024Document4 pagesSero We 2024keorapetsemorengerwa00No ratings yet

- Pre-Algebra - 2, 3, 4, and 5 Periods Schedule and AssignmentsDocument4 pagesPre-Algebra - 2, 3, 4, and 5 Periods Schedule and AssignmentsgregmcginnisNo ratings yet

- Fina ManDocument20 pagesFina ManhurtlangNo ratings yet

- STA228418BTe 2022 ks2 Mathematics Braille Transcript Paper2 ReasoningDocument20 pagesSTA228418BTe 2022 ks2 Mathematics Braille Transcript Paper2 ReasoningYakshrajsinh JadejaNo ratings yet

- Paper 2007-08 (1) (11.29)Document19 pagesPaper 2007-08 (1) (11.29)Kasun CostaNo ratings yet

- Assignment Business AnalyticsDocument2 pagesAssignment Business Analyticskartikeys271No ratings yet

- 1a. Ielts Practice Tests - Listening Quarter 2.2021 - Halo Language CenterDocument55 pages1a. Ielts Practice Tests - Listening Quarter 2.2021 - Halo Language CenteraiyuhenNo ratings yet

- Analytical Tools - End Term - Tri 3 Set 1Document9 pagesAnalytical Tools - End Term - Tri 3 Set 1wikiSoln blogNo ratings yet

- JAIIB AFB Sample Questions by Murugan For May 2015 PDFDocument188 pagesJAIIB AFB Sample Questions by Murugan For May 2015 PDFGoutham RajanNo ratings yet

- Get Answers InstantlyDocument187 pagesGet Answers InstantlyLets DiscussNo ratings yet

- First Mid-Term P09Document11 pagesFirst Mid-Term P09Ashok Kumar DondatiNo ratings yet

- The Education System in the Russian Federation: Education Brief 2012From EverandThe Education System in the Russian Federation: Education Brief 2012No ratings yet

- BUS101 Final - Answer BookletDocument6 pagesBUS101 Final - Answer BookletMUSTAFANo ratings yet

- CM SampleExam 2Document10 pagesCM SampleExam 2sarahjohnsonNo ratings yet

- Assig 2Document7 pagesAssig 2Katie CookNo ratings yet

- English A Revision NotesDocument36 pagesEnglish A Revision NotesKay100% (1)

- Surprise Test: Silicon Institute of TechnologyDocument1 pageSurprise Test: Silicon Institute of Technologysushant_pattnaikNo ratings yet

- Big V Telecom BrochureDocument4 pagesBig V Telecom BrochurejericvazNo ratings yet

- Eco100y1 Wolfson Tt2 2012fDocument12 pagesEco100y1 Wolfson Tt2 2012fexamkillerNo ratings yet

- Application Form 2012 10735Document3 pagesApplication Form 2012 10735sweetypie_arpitaNo ratings yet

- Sept 21 FWM 11 Pstorey Course Syllabus 2016Document2 pagesSept 21 FWM 11 Pstorey Course Syllabus 2016api-286302284No ratings yet

- 2 25 EcnomicsDocument4 pages2 25 Ecnomicssharathk916No ratings yet

- Cash Flow: MonthlyDocument4 pagesCash Flow: MonthlyMitch LimNo ratings yet

- NCERT Grade 09 Mathematics Statistics1Document21 pagesNCERT Grade 09 Mathematics Statistics1sonu7sadotraNo ratings yet

- Important Instructions: Points To Remember While Filling The Application FormDocument2 pagesImportant Instructions: Points To Remember While Filling The Application FormPriyanka AgarwalNo ratings yet

- Statistiek 1920 HER ENG CovDocument8 pagesStatistiek 1920 HER ENG CovThe PrankfellasNo ratings yet

- SAP FINANCE SYSTEM - Departmental User GuideDocument126 pagesSAP FINANCE SYSTEM - Departmental User Guidesteinfatt1No ratings yet

- 177 Studymat 2 Final Morning SolutionDocument8 pages177 Studymat 2 Final Morning SolutionsenthilprabhumkNo ratings yet

- HADM 2250 Prelim I ExamDocument6 pagesHADM 2250 Prelim I ExamtrollingandstalkingNo ratings yet

- Monash University: Semester One Examination 2008Document19 pagesMonash University: Semester One Examination 2008MichelleNo ratings yet

- Assignment PDFDocument1 pageAssignment PDFsurangabongaNo ratings yet

- Models For Financial Economics - July 2015: Normal Distribution Calculator Prometric Web SiteDocument3 pagesModels For Financial Economics - July 2015: Normal Distribution Calculator Prometric Web SitelolNo ratings yet

- Second Midterm Solutions 2010 EconDocument14 pagesSecond Midterm Solutions 2010 EconJordanVeroNo ratings yet

- AttachmentDocument9 pagesAttachmentgabriellaNo ratings yet

- SOP (With Proper Detail & Examples) PDFDocument7 pagesSOP (With Proper Detail & Examples) PDFMuhammadMansoorGoharNo ratings yet

- University of Toronto - ECO 204 - 2011 - 2012 - : Department of Economics Ajaz HussainDocument20 pagesUniversity of Toronto - ECO 204 - 2011 - 2012 - : Department of Economics Ajaz HussainexamkillerNo ratings yet

- Prestentation Europe Statistics CommerceDocument15 pagesPrestentation Europe Statistics CommercePetter AndreassonNo ratings yet

- VT18 Ekonometri 1 180425Document34 pagesVT18 Ekonometri 1 180425Petter AndreassonNo ratings yet

- Exam170218 PDFDocument4 pagesExam170218 PDFPetter AndreassonNo ratings yet

- PoliticalDocument4 pagesPoliticalPetter AndreassonNo ratings yet

- Asian Emerging Markets Exam With AnswersDocument6 pagesAsian Emerging Markets Exam With AnswersPetter AndreassonNo ratings yet

- Exam170218 PDFDocument4 pagesExam170218 PDFPetter AndreassonNo ratings yet

- PoliticalDocument4 pagesPoliticalPetter AndreassonNo ratings yet

- Qualitative Methods LibreDocument19 pagesQualitative Methods LibrePetter AndreassonNo ratings yet

- Renault Nissan S09Document15 pagesRenault Nissan S09Petter AndreassonNo ratings yet

- K 30Document295 pagesK 30Petter AndreassonNo ratings yet

- Case30 GhosnDocument15 pagesCase30 GhosnPetter Andreasson100% (1)

- Bric S Assignment 10Document5 pagesBric S Assignment 10Petter AndreassonNo ratings yet

- GM0105 - SyllabusDocument3 pagesGM0105 - SyllabusPetter AndreassonNo ratings yet

- Emerging Banking ServicesDocument3 pagesEmerging Banking ServicesAashika AgNo ratings yet

- Chapter 25 ABCDocument6 pagesChapter 25 ABCKathleen Joi MontezaNo ratings yet

- FIN ZG 518: Multinational Finance: BITS PilaniDocument30 pagesFIN ZG 518: Multinational Finance: BITS PilaniMohana KrishnaNo ratings yet

- Carter's LBO ModelDocument1 pageCarter's LBO ModelNoah100% (1)

- ABC Company Current Assets and LiabilitiesDocument9 pagesABC Company Current Assets and LiabilitiesChristine Joy LanabanNo ratings yet

- Economics and Management AS501T Syllabus Ver1 - 19082023Document1 pageEconomics and Management AS501T Syllabus Ver1 - 19082023fasiwad871No ratings yet

- Liquidity of Short-Term AssetsDocument23 pagesLiquidity of Short-Term AssetsRoy Navarro VispoNo ratings yet

- Financial Analysis Model:: Enter Data in Black Cells Are Computer GeneratedDocument2 pagesFinancial Analysis Model:: Enter Data in Black Cells Are Computer GeneratedAnkit ChaudharyNo ratings yet

- IasDocument229 pagesIasPeter Apollo Latosa100% (1)

- B326 MTA REVISION Summer 2019 - Third UpdateDocument27 pagesB326 MTA REVISION Summer 2019 - Third UpdatemjlNo ratings yet

- Amk 1Document4 pagesAmk 1rykaNo ratings yet

- A Critical Examination of Mineral Valuation Methods in Current Use - Hoskold and Morkill PDFDocument5 pagesA Critical Examination of Mineral Valuation Methods in Current Use - Hoskold and Morkill PDFRenzo Murillo100% (3)

- The Impact of Working Capital Management On The Performance of Food and Beverages IndustryDocument6 pagesThe Impact of Working Capital Management On The Performance of Food and Beverages IndustrySaheed NureinNo ratings yet

- Fin Mar Script TineDocument3 pagesFin Mar Script TineChristine RepuldaNo ratings yet

- Portfolio Return MeasurementDocument7 pagesPortfolio Return Measurementkusi786No ratings yet

- Secrets of A Forex Millionaire TraderDocument61 pagesSecrets of A Forex Millionaire TraderEric PlottPalmTrees.Com75% (12)

- Chapter-1-Marketing-ChannelDocument43 pagesChapter-1-Marketing-ChannelSrushti GadgeNo ratings yet

- Balance Sheet: Notes 2010 Taka 2009 TakaDocument5 pagesBalance Sheet: Notes 2010 Taka 2009 TakaThushara SilvaNo ratings yet

- Companies Act - SI 62 - 1996Document35 pagesCompanies Act - SI 62 - 1996CourageNo ratings yet

- Cambridge IGCSE™: Accounting 0452/23 October/November 2020Document14 pagesCambridge IGCSE™: Accounting 0452/23 October/November 2020ATTIQ UR REHMANNo ratings yet

- Cost of Capital Reviewer For Financial Management IDocument56 pagesCost of Capital Reviewer For Financial Management Ikimjoonmyeon22No ratings yet

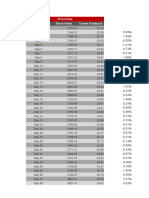

- Price Data Date Stock Index Turner FastbuckDocument14 pagesPrice Data Date Stock Index Turner FastbuckRampraveen ChamarthiNo ratings yet

- Capital Budgeting: Project Life-CycleDocument31 pagesCapital Budgeting: Project Life-CycleaauaniNo ratings yet

- Chapter-11 Stock Return and ValuationDocument7 pagesChapter-11 Stock Return and ValuationAnushrut MNo ratings yet

- Auditing ElementsDocument25 pagesAuditing ElementsBWAMBALE SALVERI MUZANANo ratings yet

- IRM Chapter 2 Concept ReviewsDocument6 pagesIRM Chapter 2 Concept ReviewsJustine Belle FryorNo ratings yet

- Frozen chicken nugget demand shift effect on price and quantityDocument7 pagesFrozen chicken nugget demand shift effect on price and quantityKwabena Obeng-FosuNo ratings yet

- Corporate Level StrategyDocument33 pagesCorporate Level StrategyDave NamakhwaNo ratings yet

- Financial Statement Analysis: Principles of Managerial AccountingDocument101 pagesFinancial Statement Analysis: Principles of Managerial AccountingLucy UnNo ratings yet

- Boot Camp Part 2: Volatility, Directional Trading, and SpreadingDocument48 pagesBoot Camp Part 2: Volatility, Directional Trading, and SpreadingVineet Vidyavilas PathakNo ratings yet