You might also like

- What Programmatic Acquirers Do DifferentlyDocument7 pagesWhat Programmatic Acquirers Do DifferentlyMohammed ShalawyNo ratings yet

- Training Session 3Document42 pagesTraining Session 3Nguyễn Như DuyNo ratings yet

- Investment Brief Pro FormaDocument7 pagesInvestment Brief Pro Formadocuments101231No ratings yet

- M&a Advisory Services Brief PresentationDocument21 pagesM&a Advisory Services Brief PresentationAli Gokhan KocanNo ratings yet

- Umbrex Commercial Due Diligence Playbook First EDocument102 pagesUmbrex Commercial Due Diligence Playbook First EAlexandre GoncalvesNo ratings yet

- Biobusines Plan: Ernst & YoungDocument16 pagesBiobusines Plan: Ernst & YoungBeatriz MontaneNo ratings yet

- Capital Budgeting Decisions: Fadi Alkaraan and Trevor HopperDocument32 pagesCapital Budgeting Decisions: Fadi Alkaraan and Trevor Hopperh417d1k4No ratings yet

- Lectures 1 to 4 Financial StrategyDocument55 pagesLectures 1 to 4 Financial StrategyHunal Kumar MautadinNo ratings yet

- Due DiligenceDocument32 pagesDue DiligenceDjomar RabangNo ratings yet

- How To Solve CasesDocument23 pagesHow To Solve CasesLakshay BurmanNo ratings yet

- Mba III Strategic Management (10mba31) Notes (Repaired)Document149 pagesMba III Strategic Management (10mba31) Notes (Repaired)Bhavani B SNo ratings yet

- Buying or Selling A Financial PracticeDocument9 pagesBuying or Selling A Financial PracticeANo ratings yet

- Mature Companies: Corporate Financial Strategy 4th Edition DR Ruth BenderDocument13 pagesMature Companies: Corporate Financial Strategy 4th Edition DR Ruth BenderAmmara NawazNo ratings yet

- Acquisitions and Selling A Business: Corporate Financial Strategy 4th Edition DR Ruth BenderDocument19 pagesAcquisitions and Selling A Business: Corporate Financial Strategy 4th Edition DR Ruth BenderAin roseNo ratings yet

- Transformation in Private Banking enDocument6 pagesTransformation in Private Banking enAchievefit Run clubNo ratings yet

- Accenture Merger Acquisition Divestitureand Alliance ServicesDocument16 pagesAccenture Merger Acquisition Divestitureand Alliance Serviceszmezarina50% (2)

- Introduction To Investment BankingDocument24 pagesIntroduction To Investment BankinglegonaNo ratings yet

- CIE Section 5Document15 pagesCIE Section 5Sagar KumarNo ratings yet

- B Plan WorkshopDocument39 pagesB Plan WorkshopChirag GargNo ratings yet

- Comprehensive ExamDocument27 pagesComprehensive Examkristine dionesNo ratings yet

- Falcon Group Deck for Telekom SlovenijeDocument17 pagesFalcon Group Deck for Telekom SlovenijeRaman SrinivasanNo ratings yet

- Due DiligenceDocument5 pagesDue DiligenceKeith Parker100% (3)

- VALUATIONDocument48 pagesVALUATIONIshika ParasrampuriaNo ratings yet

- Case StudyDocument3 pagesCase StudyArslan AshfaqNo ratings yet

- Change Management in Multinational Corporations: Lectures 5-6Document28 pagesChange Management in Multinational Corporations: Lectures 5-6MariaNo ratings yet

- Class Notes #1Document6 pagesClass Notes #1shalabh_hscNo ratings yet

- Financial ModellingDocument12 pagesFinancial Modellingalokroutray40% (5)

- Strategic Management: Business ObjectivesDocument5 pagesStrategic Management: Business ObjectivesKushalKaleNo ratings yet

- Slides1 14 PDFDocument240 pagesSlides1 14 PDFVinay KumarNo ratings yet

- M&A ProcessDocument20 pagesM&A ProcessSweta HansariaNo ratings yet

- 1 Ddim 2019 Slides Gimede PDFDocument105 pages1 Ddim 2019 Slides Gimede PDFfabriNo ratings yet

- Management: PlanningDocument22 pagesManagement: PlanningAkshay BaidNo ratings yet

- Topeka Adhesive - Financial ForecastingDocument25 pagesTopeka Adhesive - Financial ForecastingAlvin Francis Co100% (1)

- The Investment Feasibility StudyDocument9 pagesThe Investment Feasibility StudyBiodun AhmedNo ratings yet

- 1.1 StrategyDocument20 pages1.1 StrategyVarikela GouthamNo ratings yet

- Business Opportunity Thinking: Building a Sustainable, Diversified BusinessFrom EverandBusiness Opportunity Thinking: Building a Sustainable, Diversified BusinessNo ratings yet

- Key Steps Before Talking To Venture Capitalists - Intel Capital PDFDocument7 pagesKey Steps Before Talking To Venture Capitalists - Intel Capital PDFSam100% (1)

- Operational Value Creation An Investors EdgeDocument8 pagesOperational Value Creation An Investors EdgeHichemNo ratings yet

- Chapter 2Document18 pagesChapter 2Yosef KetemaNo ratings yet

- Bain - Mergers & AcquisitionsDocument2 pagesBain - Mergers & AcquisitionsddubyaNo ratings yet

- Projected Financial StatementsDocument16 pagesProjected Financial StatementsRambu MahembaNo ratings yet

- B2B Business To BusinessDocument24 pagesB2B Business To BusinessBhupendra SsharmaNo ratings yet

- Fundamentals of Industrial Management ExamDocument13 pagesFundamentals of Industrial Management ExamKawsar AhmedNo ratings yet

- Review About EntrepreneurshipDocument5 pagesReview About EntrepreneurshipSabina MaxamedNo ratings yet

- Week 4 Lecture FINS3623Document50 pagesWeek 4 Lecture FINS3623826012442qq.comNo ratings yet

- Po MGT Session 4Document14 pagesPo MGT Session 4Tayyaba JamilNo ratings yet

- 3 Keys To Obtain VCDocument40 pages3 Keys To Obtain VCyezdianNo ratings yet

- Mergers and Acquisitions: The Deal Process From An Investment Banker's PerspectiveDocument35 pagesMergers and Acquisitions: The Deal Process From An Investment Banker's Perspectiverachana.bang3967No ratings yet

- Comparison Between Investment in Equity and Mutual Fund - Dissertation Ideas or Thesis Topics PDFDocument4 pagesComparison Between Investment in Equity and Mutual Fund - Dissertation Ideas or Thesis Topics PDFPuneet AgarwalNo ratings yet

- Business Model - 2021 - SCEDocument23 pagesBusiness Model - 2021 - SCESimranjeet KaurNo ratings yet

- Joint Ventures Presentation to Law StudentsDocument36 pagesJoint Ventures Presentation to Law Studentsbigricky taru100% (1)

- Strategizing and Structuring M&A ActivityDocument13 pagesStrategizing and Structuring M&A ActivityNareshNo ratings yet

- Pro M&A and Private Equity: Course OverviewDocument5 pagesPro M&A and Private Equity: Course OverviewTẤN LỘC LouisNo ratings yet

- Business Plan Alchemy: Transforming Ideas Into Successful Business VenturesFrom EverandBusiness Plan Alchemy: Transforming Ideas Into Successful Business VenturesNo ratings yet

- Statistics ManagementDocument37 pagesStatistics Managementfobaf11728No ratings yet

- Marketing For Financial ServicesDocument34 pagesMarketing For Financial ServicesSiddham JainNo ratings yet

- Understanding Key Terms Why Bad Deals Happen To Good People Why Do Buyers Buy, and Why Do Sellers Sell?Document8 pagesUnderstanding Key Terms Why Bad Deals Happen To Good People Why Do Buyers Buy, and Why Do Sellers Sell?yasserNo ratings yet

- Mergers Complete Mini CourseDocument7 pagesMergers Complete Mini CoursensalemNo ratings yet

- Critical Understanding of Organizational MarketingDocument28 pagesCritical Understanding of Organizational MarketingWaqas AhmadNo ratings yet

- Only the Paranoid Survive (Review and Analysis of Grove's Book)From EverandOnly the Paranoid Survive (Review and Analysis of Grove's Book)No ratings yet

- London Property Development Project Cost AnalysisDocument2 pagesLondon Property Development Project Cost AnalysisjordenNo ratings yet

- PDocument21 pagesPjordenNo ratings yet

- Pershing Square Sohn PresentationDocument47 pagesPershing Square Sohn Presentationmarketfolly.com100% (2)

- Pershing Square Sohn PresentationDocument47 pagesPershing Square Sohn Presentationmarketfolly.com100% (2)

- Project Name: 3 MALDEN ROAD NW5 3HS: Agent: - Asking Price 4,000,000.00Document3 pagesProject Name: 3 MALDEN ROAD NW5 3HS: Agent: - Asking Price 4,000,000.00jordenNo ratings yet

- Dis 3052Document414 pagesDis 3052ZeeNo ratings yet

- Bible King James Version PDFDocument2,652 pagesBible King James Version PDFjordenNo ratings yet

- VRRRRRRRRRRRRRDocument56 pagesVRRRRRRRRRRRRRjordenNo ratings yet

- Top 4 Investment Banking ChartsDocument36 pagesTop 4 Investment Banking ChartsNarendraSinhaNo ratings yet

- The Yield Curve As A Leading Indicator: Some Practical IssuesDocument8 pagesThe Yield Curve As A Leading Indicator: Some Practical IssuesgilsofuyNo ratings yet

- Insurtech: A Golden Opportunity For Insurers To Innovate: March 2016Document12 pagesInsurtech: A Golden Opportunity For Insurers To Innovate: March 2016jordenNo ratings yet

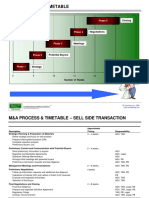

- M&A Process & Timetable: ClosingDocument2 pagesM&A Process & Timetable: ClosingjordenNo ratings yet

- Pe Mathematics Apr2009 Assessing The RiskDocument13 pagesPe Mathematics Apr2009 Assessing The RiskjordenNo ratings yet

- The Art of Film Funding, 2nd EditionDocument23 pagesThe Art of Film Funding, 2nd EditionMichael Wiese Productions71% (7)

- Revision Worksheet - Matrices and DeterminantsDocument2 pagesRevision Worksheet - Matrices and DeterminantsAryaNo ratings yet

- AA ActivitiesDocument4 pagesAA ActivitiesSalim Amazir100% (1)

- Google Earth Learning Activity Cuban Missile CrisisDocument2 pagesGoogle Earth Learning Activity Cuban Missile CrisisseankassNo ratings yet

- How To Text A Girl - A Girls Chase Guide (Girls Chase Guides) (PDFDrive) - 31-61Document31 pagesHow To Text A Girl - A Girls Chase Guide (Girls Chase Guides) (PDFDrive) - 31-61Myster HighNo ratings yet

- Dep 32.32.00.11-Custody Transfer Measurement Systems For LiquidDocument69 pagesDep 32.32.00.11-Custody Transfer Measurement Systems For LiquidDAYONo ratings yet

- The Service Marketing Plan On " Expert Personalized Chef": Presented byDocument27 pagesThe Service Marketing Plan On " Expert Personalized Chef": Presented byA.S. ShuvoNo ratings yet

- SOP-for RecallDocument3 pagesSOP-for RecallNilove PervezNo ratings yet

- Rubric 5th GradeDocument2 pagesRubric 5th GradeAlbert SantosNo ratings yet

- 02 Slide Pengenalan Dasar MapinfoDocument24 pages02 Slide Pengenalan Dasar MapinfoRizky 'manda' AmaliaNo ratings yet

- Ratio Analysis of PIADocument16 pagesRatio Analysis of PIAMalik Saad Noman100% (5)

- EIRA v0.8.1 Beta OverviewDocument33 pagesEIRA v0.8.1 Beta OverviewAlexQuiñonesNietoNo ratings yet

- CBSE Class 6 Whole Numbers WorksheetDocument2 pagesCBSE Class 6 Whole Numbers WorksheetPriyaprasad PandaNo ratings yet

- Indian Standard: Pla Ing and Design of Drainage IN Irrigation Projects - GuidelinesDocument7 pagesIndian Standard: Pla Ing and Design of Drainage IN Irrigation Projects - GuidelinesGolak PattanaikNo ratings yet

- WindSonic GPA Manual Issue 20Document31 pagesWindSonic GPA Manual Issue 20stuartNo ratings yet

- Financial Analysis of Wipro LTDDocument101 pagesFinancial Analysis of Wipro LTDashwinchaudhary89% (18)

- Mpu 2312Document15 pagesMpu 2312Sherly TanNo ratings yet

- Human Rights Alert: Corrective Actions in Re: Litigation Involving Financial InstitutionsDocument3 pagesHuman Rights Alert: Corrective Actions in Re: Litigation Involving Financial InstitutionsHuman Rights Alert - NGO (RA)No ratings yet

- Peran Dan Tugas Receptionist Pada Pt. Serim Indonesia: Disadur Oleh: Dra. Nani Nuraini Sarah MsiDocument19 pagesPeran Dan Tugas Receptionist Pada Pt. Serim Indonesia: Disadur Oleh: Dra. Nani Nuraini Sarah MsiCynthia HtbNo ratings yet

- !!!Логос - конференц10.12.21 копіяDocument141 pages!!!Логос - конференц10.12.21 копіяНаталія БондарNo ratings yet

- EN 12449 CuNi Pipe-2012Document47 pagesEN 12449 CuNi Pipe-2012DARYONO sudaryonoNo ratings yet

- History of Microfinance in NigeriaDocument9 pagesHistory of Microfinance in Nigeriahardmanperson100% (1)

- Individual Performance Commitment and Review Form (Ipcrf) : Mfos Kras Objectives Timeline Weight Per KRADocument4 pagesIndividual Performance Commitment and Review Form (Ipcrf) : Mfos Kras Objectives Timeline Weight Per KRAChris21JinkyNo ratings yet

- CTR Ball JointDocument19 pagesCTR Ball JointTan JaiNo ratings yet

- PNBONE_mPassbook_134611_6-4-2024_13-4-2024_0053XXXXXXXX00 (1) (1)Document3 pagesPNBONE_mPassbook_134611_6-4-2024_13-4-2024_0053XXXXXXXX00 (1) (1)imtiyaz726492No ratings yet

- 202112fuji ViDocument2 pages202112fuji ViAnh CaoNo ratings yet

- AD Chemicals - Freeze-Flash PointDocument4 pagesAD Chemicals - Freeze-Flash Pointyb3yonnayNo ratings yet

- Ansible Playbook for BeginnersDocument101 pagesAnsible Playbook for BeginnersFelix Andres Baquero Cubillos100% (1)

- eHMI tool download and install guideDocument19 pageseHMI tool download and install guideNam Vũ0% (1)

- France Winckler Final Rev 1Document14 pagesFrance Winckler Final Rev 1Luciano Junior100% (1)

- Oxygen Cost and Energy Expenditure of RunningDocument7 pagesOxygen Cost and Energy Expenditure of Runningnb22714No ratings yet