You might also like

- Insurtech The Threat That InspiresDocument12 pagesInsurtech The Threat That InspiresSayak ChakrabortyNo ratings yet

- Tech-Enabled TransformationDocument67 pagesTech-Enabled TransformationjhlaravNo ratings yet

- Business Motivation ModelDocument6 pagesBusiness Motivation ModelDAVID KEN DEL MUNDONo ratings yet

- Cultural GlobalizationDocument16 pagesCultural Globalizationee0785No ratings yet

- Brandi Jones-5e-Lesson-Plan 2Document3 pagesBrandi Jones-5e-Lesson-Plan 2api-491136095No ratings yet

- PWC Insurtechs Transforming ReinsurersDocument7 pagesPWC Insurtechs Transforming ReinsurersRezky Naufal PratamaNo ratings yet

- InsurTech StartUp - Lect 10 Amended 5 April 2022Document52 pagesInsurTech StartUp - Lect 10 Amended 5 April 2022HaganNo ratings yet

- The Future of Telecom: A Dual Transformation: Industry Horizons // December 2017Document10 pagesThe Future of Telecom: A Dual Transformation: Industry Horizons // December 2017John100% (1)

- 云计算和机器学习在精算行业中的应用Document9 pages云计算和机器学习在精算行业中的应用meiwanlanjunNo ratings yet

- Cenfri InsurTech For Development Research StudyDocument34 pagesCenfri InsurTech For Development Research StudyMariana F. MaldonadoNo ratings yet

- Oliver Wyman and Policen Dirket InsurTech Caught On The Radar ReportDocument52 pagesOliver Wyman and Policen Dirket InsurTech Caught On The Radar ReportCrowdfundInsider100% (2)

- Chapter 1 - Entrep - Perspectvie On EntreprenuershipDocument2 pagesChapter 1 - Entrep - Perspectvie On EntreprenuershiplulunanjohndellNo ratings yet

- Chapter 1: A Perspective On Entrepreneurship: - Refers To The Discovery or - Which Refers To TheDocument23 pagesChapter 1: A Perspective On Entrepreneurship: - Refers To The Discovery or - Which Refers To TheLouise RonquilloNo ratings yet

- Quarterly Insurtech Briefing q4 2017Document66 pagesQuarterly Insurtech Briefing q4 2017richpageantNo ratings yet

- The Intelligent Enterprise For The Insurance IndustryDocument26 pagesThe Intelligent Enterprise For The Insurance Industryjaved ahamedNo ratings yet

- 9 Debt SecuritiesDocument26 pages9 Debt SecuritiesSenthil Kumar KNo ratings yet

- Insurance in A Box Brochure 10 24 2017Document4 pagesInsurance in A Box Brochure 10 24 2017Markito TrpeskiNo ratings yet

- A New Distribution Model: Finance On-Request InsuranceDocument8 pagesA New Distribution Model: Finance On-Request Insurancenagarajbu031No ratings yet

- Cloud's Trillion-Dollar Prize Is Up For GrabsDocument16 pagesCloud's Trillion-Dollar Prize Is Up For GrabsRishabh DabasNo ratings yet

- Alternative InvestmentsDocument18 pagesAlternative InvestmentsSenthil Kumar KNo ratings yet

- Service Offerings Emerging Technologies Cloud ComputingDocument16 pagesService Offerings Emerging Technologies Cloud ComputingSanjayNo ratings yet

- J Promfg 2020 02 024Document6 pagesJ Promfg 2020 02 024123No ratings yet

- Digital Transformation As A Path To Growth PDFDocument12 pagesDigital Transformation As A Path To Growth PDFBui Hoang GiangNo ratings yet

- Beyond Insurance: Embracing Innovation To Monetize DisruptionDocument17 pagesBeyond Insurance: Embracing Innovation To Monetize Disruption459973No ratings yet

- Questions To Be AskedDocument2 pagesQuestions To Be AskedSakshi ShahNo ratings yet

- BCG Future of Indian ConsumerTechDocument68 pagesBCG Future of Indian ConsumerTechTejas JosephNo ratings yet

- Accenture - India FocusDocument31 pagesAccenture - India FocusDeepak SharmaNo ratings yet

- A Clear Understanding of The Industry: Is Cfa Institute Investment Foundations Right For You?Document17 pagesA Clear Understanding of The Industry: Is Cfa Institute Investment Foundations Right For You?SAHIL GUPTANo ratings yet

- Crisis As Antecedent of InnovationDocument6 pagesCrisis As Antecedent of InnovationSrirang JhaNo ratings yet

- Future of Wealth Management Revisited Winter 2020Document20 pagesFuture of Wealth Management Revisited Winter 2020anujNo ratings yet

- Investment Foundation - DerivativesDocument20 pagesInvestment Foundation - DerivativesSenthil Kumar KNo ratings yet

- Accenture Auto Equipment Servitization Financing ModelsDocument13 pagesAccenture Auto Equipment Servitization Financing ModelsRendy DjunaediNo ratings yet

- 10 Equity SecuritiesDocument26 pages10 Equity SecuritiesSAHIL GUPTANo ratings yet

- ABC Building-Right-Foundation-ServitizationDocument4 pagesABC Building-Right-Foundation-ServitizationDedar HossainNo ratings yet

- 66 Servitisation PMCDocument16 pages66 Servitisation PMCTalha AhmadNo ratings yet

- The New BMW: Business Model Innovation Transforms An Automotive LeaderDocument10 pagesThe New BMW: Business Model Innovation Transforms An Automotive LeaderIzhar IqbalNo ratings yet

- 13 Structure of The Investment IndustryDocument20 pages13 Structure of The Investment IndustrySenthil Kumar KNo ratings yet

- IBM Automotive 2020 Study - Clarity Beyond The ChaosDocument28 pagesIBM Automotive 2020 Study - Clarity Beyond The ChaosKal GyimesiNo ratings yet

- The Customer-Centric Insurer in The Digital EraDocument34 pagesThe Customer-Centric Insurer in The Digital ErawilsonNo ratings yet

- How Insurtech Can Close The Protection Gap in Emerging MarketsDocument8 pagesHow Insurtech Can Close The Protection Gap in Emerging MarketseugeneNo ratings yet

- FinTech Industry ChallengesDocument3 pagesFinTech Industry ChallengesInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Mini CFADocument502 pagesMini CFAMohammed AliNo ratings yet

- Accenture Tech VisionReport 2017Document56 pagesAccenture Tech VisionReport 2017achievingsquad4lifeNo ratings yet

- Building Trusted Customer Experiences in The Metaverse 1687717439Document22 pagesBuilding Trusted Customer Experiences in The Metaverse 1687717439architsomani.tradingNo ratings yet

- Novarica Research Quarterly 2020 Q1Document17 pagesNovarica Research Quarterly 2020 Q1SriramGudimellaNo ratings yet

- Professional Services: Essential Skills PlaybookDocument11 pagesProfessional Services: Essential Skills PlaybookAndrés R BucheliNo ratings yet

- Industri 4.0Document19 pagesIndustri 4.0Maria NatashaNo ratings yet

- IMB - Cognitive EnterpriseDocument64 pagesIMB - Cognitive EnterpriseAnonymous tkGObxd100% (1)

- Constellation's Research Outlook 2011Document11 pagesConstellation's Research Outlook 2011Andromeda NebulaNo ratings yet

- Cloud Considerations Brochure V3Document7 pagesCloud Considerations Brochure V3PafihiNo ratings yet

- 7 Financial StatementsDocument29 pages7 Financial StatementsSAHIL GUPTANo ratings yet

- In Fs Digital India Disruption NoexpDocument36 pagesIn Fs Digital India Disruption Noexpatique mohammedNo ratings yet

- WhatisanIntrapreneur (Intrapreneurship) 1710237333513Document7 pagesWhatisanIntrapreneur (Intrapreneurship) 1710237333513AllenaNo ratings yet

- Kukkamalla, P. K., Bikfalvi, A., & Arbussa, A. (2020) - The New BMW Business Model Innovation Transforms An Automotive Leader. EMPÍRICODocument10 pagesKukkamalla, P. K., Bikfalvi, A., & Arbussa, A. (2020) - The New BMW Business Model Innovation Transforms An Automotive Leader. EMPÍRICOHalison SouzaNo ratings yet

- Creating ValueDocument7 pagesCreating ValueAngelina FitriaaNo ratings yet

- Connected Enterprises ReportDocument27 pagesConnected Enterprises ReportPRABIN ACHARYANo ratings yet

- PWC Report On New Age InsuranceDocument32 pagesPWC Report On New Age InsuranceashishNo ratings yet

- Five Steps To Improve Innovation in The Insurance IndustryDocument8 pagesFive Steps To Improve Innovation in The Insurance IndustryMalikZohaibNazarNo ratings yet

- The Future of The Logistics IndustryDocument20 pagesThe Future of The Logistics IndustryTubagus Donny SyafardanNo ratings yet

- Your Enterprise With Sun Glassfish™ Portfolio: Build A High-Performance, Open Web Platform ForDocument16 pagesYour Enterprise With Sun Glassfish™ Portfolio: Build A High-Performance, Open Web Platform ForrsyngesNo ratings yet

- Summary of Clayton M. Christensen, Jerome H. Grossman & Jason Hwang's The Innovator's PrescriptionFrom EverandSummary of Clayton M. Christensen, Jerome H. Grossman & Jason Hwang's The Innovator's PrescriptionNo ratings yet

- Project Name: 5 The Pavement, Clapham Common, London SW4 0HZDocument2 pagesProject Name: 5 The Pavement, Clapham Common, London SW4 0HZjordenNo ratings yet

- The M&A Process and The Role of A Financial AdvisorDocument17 pagesThe M&A Process and The Role of A Financial AdvisorjordenNo ratings yet

- Project Name: 3 MALDEN ROAD NW5 3HS: Agent: - Asking Price 4,000,000.00Document3 pagesProject Name: 3 MALDEN ROAD NW5 3HS: Agent: - Asking Price 4,000,000.00jordenNo ratings yet

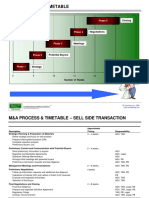

- M&A Process & Timetable: ClosingDocument2 pagesM&A Process & Timetable: ClosingjordenNo ratings yet

- 21st Cent Lit DLP KimDocument7 pages21st Cent Lit DLP KimKim BandolaNo ratings yet

- Disneyland (Manish N Suraj)Document27 pagesDisneyland (Manish N Suraj)Suraj Kedia0% (1)

- Prelim Examination in Logic DesignDocument5 pagesPrelim Examination in Logic Designdj_eqc7227No ratings yet

- MRP Configuration GuideDocument12 pagesMRP Configuration Guideofaofa1No ratings yet

- Stepping Stones Grade 4 ScopeDocument2 pagesStepping Stones Grade 4 ScopeGretchen BensonNo ratings yet

- Leadership Competencies Paper 2Document5 pagesLeadership Competencies Paper 2api-297379255No ratings yet

- Fidelizer Pro User GuideDocument12 pagesFidelizer Pro User GuidempptritanNo ratings yet

- Kaizen Idea - Sheet: Suitable Chairs To Write Their Notes Faster & Easy Method While TrainingDocument1 pageKaizen Idea - Sheet: Suitable Chairs To Write Their Notes Faster & Easy Method While TrainingWahid AkramNo ratings yet

- 27 EtdsDocument29 pages27 EtdsSuhag PatelNo ratings yet

- The Iron Warrior: Volume 25, Issue 11Document8 pagesThe Iron Warrior: Volume 25, Issue 11The Iron WarriorNo ratings yet

- Shape The Future Listening Practice - Unit 3 - Without AnswersDocument1 pageShape The Future Listening Practice - Unit 3 - Without Answersleireleire20070701No ratings yet

- Agents SocializationDocument4 pagesAgents Socializationinstinct920% (1)

- Manage Your Nude PhotosDocument14 pagesManage Your Nude PhotosRick80% (5)

- Limitations of The Study - Docx EMDocument1 pageLimitations of The Study - Docx EMthreeNo ratings yet

- For Purposeful and Meaningful Technology Integration in The ClassroomDocument19 pagesFor Purposeful and Meaningful Technology Integration in The ClassroomVincent Chris Ellis TumaleNo ratings yet

- Types of Dance Steps and Positions PDFDocument11 pagesTypes of Dance Steps and Positions PDFRather NotNo ratings yet

- Policy Analysis ReportDocument16 pagesPolicy Analysis ReportGhelvin Auriele AguirreNo ratings yet

- BeginnersGuide AndroidonOmapZoomDocument10 pagesBeginnersGuide AndroidonOmapZoomm13marleNo ratings yet

- Sika Bro - E - Sikadur-Combiflex SG System - High Performance Joint - Crack Waterproofing System (09.2010)Document8 pagesSika Bro - E - Sikadur-Combiflex SG System - High Performance Joint - Crack Waterproofing System (09.2010)Joh SongthamNo ratings yet

- Vertical Axis Wind Turbine ProjDocument2 pagesVertical Axis Wind Turbine Projmacsan sanchezNo ratings yet

- Gower SlidesCarnivalDocument28 pagesGower SlidesCarnivalBình PhạmNo ratings yet

- Cee 2005 - 06Document129 pagesCee 2005 - 06iloveeggxPNo ratings yet

- A Modified Newton's Method For Solving Nonlinear Programing ProblemsDocument15 pagesA Modified Newton's Method For Solving Nonlinear Programing Problemsjhon jairo portillaNo ratings yet

- DSpace Configuration PDFDocument1 pageDSpace Configuration PDFArshad SanwalNo ratings yet

- CBSE Class 10 Science Sample Paper-08 (For 2013)Document11 pagesCBSE Class 10 Science Sample Paper-08 (For 2013)cbsesamplepaperNo ratings yet

- BC-2800 Maintenance Manual For EngineersDocument3 pagesBC-2800 Maintenance Manual For EngineersIslam AdelNo ratings yet

- Penawaran AC LG - GD Checkup Laborat RS PHCDocument1 pagePenawaran AC LG - GD Checkup Laborat RS PHCaisyahbrillianaNo ratings yet

- Mmims5elesson BiomesDocument3 pagesMmims5elesson Biomesapi-490524730100% (1)