You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- UK - Introducing The Integrated Operating Concept 2025Document20 pagesUK - Introducing The Integrated Operating Concept 2025nelson duringNo ratings yet

- Integrated ReviewDocument120 pagesIntegrated ReviewChristianNo ratings yet

- US DEA 2020 National Drug Threat AssessmentDocument100 pagesUS DEA 2020 National Drug Threat Assessmentnelson during100% (1)

- 2020 Dod China Military Power Report Final PDFDocument200 pages2020 Dod China Military Power Report Final PDF蔡娪嫣100% (1)

- DIA Chinese Military Power ReportDocument140 pagesDIA Chinese Military Power ReportJared Keller100% (6)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Silent Ruin - Army Cyber InstituteDocument10 pagesSilent Ruin - Army Cyber Institutenelson during50% (2)

- List of Pharmaceutical Companies in INDIA (Address and Phone NO) - PharmexcelDocument22 pagesList of Pharmaceutical Companies in INDIA (Address and Phone NO) - PharmexcelKarthikeyan radhakrishnan67% (3)

- The Times 17 March 2021 UK Defense ReviewDocument4 pagesThe Times 17 March 2021 UK Defense Reviewnelson duringNo ratings yet

- SIPRI - Trends in International Arms Transfer 2019Document12 pagesSIPRI - Trends in International Arms Transfer 2019nelson duringNo ratings yet

- UNESCO Alerta para Aumento Dos Ataques Contra Jornalistas Que Cobrem ProtestosDocument17 pagesUNESCO Alerta para Aumento Dos Ataques Contra Jornalistas Que Cobrem Protestosnelson duringNo ratings yet

- SASC SOUTHCOM Posture StatementDocument17 pagesSASC SOUTHCOM Posture Statementnelson during100% (1)

- Secret Service Attack ReportDocument20 pagesSecret Service Attack Reportepraetorian100% (1)

- UN Human Rights Report Chile 2019Document33 pagesUN Human Rights Report Chile 2019nelson duringNo ratings yet

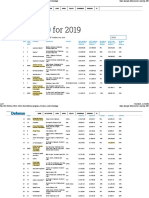

- Top 100 DefenseNews 2019Document7 pagesTop 100 DefenseNews 2019nelson duringNo ratings yet

- 2019 Army Modernization Strategy - FinalDocument14 pages2019 Army Modernization Strategy - FinalBreakingDefenseNo ratings yet

- Anistia Internaional - Informe Anual 2019Document96 pagesAnistia Internaional - Informe Anual 2019nelson duringNo ratings yet

- Gen Townsend Us AfricomDocument19 pagesGen Townsend Us Africomnelson duringNo ratings yet

- Vladimir Putin Presidential Address To Nation 15 Jan 2020Document30 pagesVladimir Putin Presidential Address To Nation 15 Jan 2020nelson duringNo ratings yet

- Trends in International Arms Transfers, 2018: SIPRI Fact SheetDocument12 pagesTrends in International Arms Transfers, 2018: SIPRI Fact Sheetjoel enciso enekeNo ratings yet

- Landmine Monitor 2018Document118 pagesLandmine Monitor 2018nelson duringNo ratings yet

- NL MoD RussianOperationOPCWDocument35 pagesNL MoD RussianOperationOPCWnelson duringNo ratings yet

- A - HRC - 41 - 18 Human Rights in The Bolivarian Republic of VenezuelaDocument16 pagesA - HRC - 41 - 18 Human Rights in The Bolivarian Republic of Venezuelanelson duringNo ratings yet

- USNORTHCOM FaithfulPatriotDocument33 pagesUSNORTHCOM FaithfulPatriotnelson duringNo ratings yet

- JapanDocument10 pagesJapannelson duringNo ratings yet

- UNODC - World Drug Report 2018Document41 pagesUNODC - World Drug Report 2018nelson duringNo ratings yet

- Sipri - Trends in World Military Expenditure, 2017Document8 pagesSipri - Trends in World Military Expenditure, 2017nelson duringNo ratings yet

- Improving Security of United Nations Peacekeepers ReportDocument43 pagesImproving Security of United Nations Peacekeepers Reportnelson duringNo ratings yet

- REVIEW OF MARITIME TRANSPORT 50 YearsDocument116 pagesREVIEW OF MARITIME TRANSPORT 50 Yearsnelson duringNo ratings yet

- WORLDWIDE THREAT ASSESSMENT of The US INTELLIGENCE COMMUNITYDocument28 pagesWORLDWIDE THREAT ASSESSMENT of The US INTELLIGENCE COMMUNITYnelson duringNo ratings yet

- DMBD 14 September 2022 Siang Per Jam 9Document65 pagesDMBD 14 September 2022 Siang Per Jam 9DikNo ratings yet

- List of Multinational CorporationsDocument19 pagesList of Multinational CorporationsniviphNo ratings yet

- 00000875Document178 pages00000875giovanebalzaniNo ratings yet

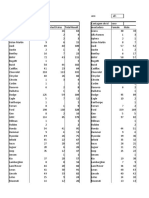

- Fleet DataDocument38 pagesFleet DataBOC ClaimsNo ratings yet

- DBDocument454 pagesDBJefferson Acacio Rocha MirandaNo ratings yet

- Thermoflow GTGsDocument8 pagesThermoflow GTGsJalal GhelichzadehNo ratings yet

- BalinerasDocument18 pagesBalinerasgaelNo ratings yet

- ApplicationsDocument450 pagesApplicationsSantiago Sanchez CobosNo ratings yet

- Hair Removers Bleaches in Asia Pacific DatagraphicsDocument3 pagesHair Removers Bleaches in Asia Pacific Datagraphicsanup.bobdeNo ratings yet

- Manteminientos 2013-2021 JorgeDocument659 pagesManteminientos 2013-2021 JorgeJosue fernando bravo garcia100% (1)

- Beverages Supplier ListDocument2 pagesBeverages Supplier ListAbhishek PattanshetterNo ratings yet

- Filtros Combustible FamelDocument9 pagesFiltros Combustible Famelrichard44927No ratings yet

- BOSCH FR8DCX+ - Cross Reference PDFDocument1 pageBOSCH FR8DCX+ - Cross Reference PDFMauricio LisboaNo ratings yet

- Company Name Name Designation Location Mobile NoDocument4 pagesCompany Name Name Designation Location Mobile NoAbhijit BarmanNo ratings yet

- PT. CG Power Systems Indonesia - Ref. ListDocument31 pagesPT. CG Power Systems Indonesia - Ref. Listbakrie46No ratings yet

- Timing Belt: Tensioners / IdlersDocument52 pagesTiming Belt: Tensioners / IdlersAdamNo ratings yet

- Indian Pharmaceutical IndustryDocument25 pagesIndian Pharmaceutical IndustryVijaya enterprisesNo ratings yet

- Obd MapDocument52 pagesObd MapMagalhaes DedecoNo ratings yet

- Pcat1632GKN Driveline Universal Joints 2005 - 2006 PDFDocument102 pagesPcat1632GKN Driveline Universal Joints 2005 - 2006 PDFdanielhcdsNo ratings yet

- SolidWorks Education Detailed Drawing ExercisesDocument51 pagesSolidWorks Education Detailed Drawing ExercisesLeonardo AlexNo ratings yet

- PhilipsCodeListAB v8Document16 pagesPhilipsCodeListAB v8Daniel GrunfeldNo ratings yet

- Mitsubishi Canter LocksDocument13 pagesMitsubishi Canter LocksDavid AliNo ratings yet

- Comparison of HUL P GDocument8 pagesComparison of HUL P GMia KhalifaNo ratings yet

- MetroCast Remote UR5U-8700L 8720LDocument2 pagesMetroCast Remote UR5U-8700L 8720LPierre BarkettNo ratings yet

- AliExpress Guide to Perfume, Sunglasses, Shirts & More Under 40 CharactersDocument39 pagesAliExpress Guide to Perfume, Sunglasses, Shirts & More Under 40 CharactersPedroAlvaresNo ratings yet

- Sleeve Cross Reference GuideDocument76 pagesSleeve Cross Reference GuideDenis Vasquez50% (2)

- All Makes Filters Cross Reference GuidesDocument5 pagesAll Makes Filters Cross Reference GuidesJafet Israel RojasNo ratings yet

- Compressors, High PressureDocument42 pagesCompressors, High PressureBEN100% (2)

- Recorder Approval 2Document7 pagesRecorder Approval 2fhm143No ratings yet