You might also like

- AdjustmentsDocument3 pagesAdjustmentsapi-417927166No ratings yet

- AdjustmentDocument8 pagesAdjustmentBibin SavioNo ratings yet

- Final-Accounts-Q - A P&L ACCDocument31 pagesFinal-Accounts-Q - A P&L ACCNikhil PrasannaNo ratings yet

- Adobe Scan 20-Apr-2023Document6 pagesAdobe Scan 20-Apr-2023Notes GlobeNo ratings yet

- Partnership Firms Part 2 Appropriation of ProfitDocument14 pagesPartnership Firms Part 2 Appropriation of ProfitDeepti BistNo ratings yet

- 1 - Accounting For Partnership Firms - FundamentalsDocument12 pages1 - Accounting For Partnership Firms - FundamentalsAnkit RoyNo ratings yet

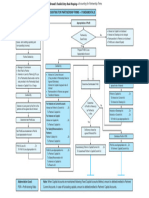

- Flow Chart (L-2)Document1 pageFlow Chart (L-2)JazaNo ratings yet

- Advanced Accounts PDFDocument29 pagesAdvanced Accounts PDFmettutejaNo ratings yet

- Poa FormatDocument4 pagesPoa FormatSumithaNo ratings yet

- Adjustments at A GlanceDocument1 pageAdjustments at A GlanceMuhammad UmarNo ratings yet

- Flow Chart-1Document1 pageFlow Chart-1Pankaj MahajanNo ratings yet

- Final Account Adjusment EntryDocument1 pageFinal Account Adjusment Entrykhanpur88822No ratings yet

- Dissolution Notes 2Document16 pagesDissolution Notes 2bhosaleparth97No ratings yet

- Accounting For Partnership Firms - FundamentalsDocument5 pagesAccounting For Partnership Firms - FundamentalsPainNo ratings yet

- Tally Ledger GroupDocument1 pageTally Ledger GroupArpit GaurNo ratings yet

- Final Accounts AdjustmentsDocument2 pagesFinal Accounts Adjustmentskarthikdsk1810No ratings yet

- Final AccountsDocument61 pagesFinal AccountsvimalaNo ratings yet

- FlowCharts 9Document2 pagesFlowCharts 9sopandebnath03No ratings yet

- 2 Fundamentals of PartnershipDocument11 pages2 Fundamentals of PartnershipKartik JainNo ratings yet

- CH - 04 Dissolution of Partnership FirmDocument10 pagesCH - 04 Dissolution of Partnership FirmMahathi AmudhanNo ratings yet

- Underwriting of Shares and DebenturesDocument5 pagesUnderwriting of Shares and Debenturesharsh singhNo ratings yet

- Flow Chart (L-8)Document2 pagesFlow Chart (L-8)Simer preet kaurNo ratings yet

- Ilovepdf MergedDocument10 pagesIlovepdf MergedDivyam RohillaNo ratings yet

- Set 1 Test No.1 Answer KeyDocument4 pagesSet 1 Test No.1 Answer KeyJOHAN JOJONo ratings yet

- Dissolution Notes FullDocument4 pagesDissolution Notes FullVansh BarsaiyanNo ratings yet

- Important Questions For Class 11 Accountancy Chapter 10 - Financial Statements IIDocument16 pagesImportant Questions For Class 11 Accountancy Chapter 10 - Financial Statements IIABHISHEK SINGHNo ratings yet

- Interest On Drawings 1Document10 pagesInterest On Drawings 1giennachemparathyNo ratings yet

- Accounts Class 12Document12 pagesAccounts Class 12Bhanu PratapNo ratings yet

- Dear Students, Good MorningDocument11 pagesDear Students, Good Morningtara nath acharyaNo ratings yet

- Fundamentals PDFDocument103 pagesFundamentals PDFDhairya JainNo ratings yet

- Advanced Accounting - IDocument74 pagesAdvanced Accounting - Igopikakalai60No ratings yet

- Company Accounts - Issue of DebenturesDocument11 pagesCompany Accounts - Issue of DebenturesHarsh MishraNo ratings yet

- LLP Full NotesDocument15 pagesLLP Full NotesJay Desai100% (1)

- Fundamentals of Partnership FirmDocument15 pagesFundamentals of Partnership Firmaayush.verma2105No ratings yet

- Joint 2 VentureDocument13 pagesJoint 2 VentureMAGOMU DAN DAVIDNo ratings yet

- Abhinav Adjustment HardDocument5 pagesAbhinav Adjustment HardakashNo ratings yet

- Depreciation of AssetDocument2 pagesDepreciation of AssetWelcome 1995No ratings yet

- Retirement or Death of Partner NewDocument5 pagesRetirement or Death of Partner NewAnkit Roy100% (1)

- Ad Acc As QusDocument196 pagesAd Acc As QusRadhika GargNo ratings yet

- Partnership Firms - Part5 Guarantee and Past AdjustmentDocument15 pagesPartnership Firms - Part5 Guarantee and Past AdjustmentDeepti BistNo ratings yet

- 12 AccountancyDocument4 pages12 AccountancyAbhishek DhillonNo ratings yet

- Notes To Diss 12Document3 pagesNotes To Diss 12Kartikay UpadhyayNo ratings yet

- CA CPT Fast Track Revision Notes - CaCmaCsGuru PDFDocument111 pagesCA CPT Fast Track Revision Notes - CaCmaCsGuru PDFSatish Kumar SahuNo ratings yet

- 61dfcmodule IIDocument14 pages61dfcmodule IIyogesh607No ratings yet

- Debit and CreditDocument21 pagesDebit and Credityogesh607No ratings yet

- Accounting For Leases - F7 Financial Reporting - ACCA Qualification - Students - ACCA GlobalDocument7 pagesAccounting For Leases - F7 Financial Reporting - ACCA Qualification - Students - ACCA GlobalInga ȚîgaiNo ratings yet

- Admission of A PartnerDocument5 pagesAdmission of A PartnerHigreeve SrudhiNo ratings yet

- Dissolution of Partnership FirmDocument17 pagesDissolution of Partnership FirmRenu Bala JainNo ratings yet

- AFAR TestbanksDocument165 pagesAFAR TestbanksbognadonhazelNo ratings yet

- Faa PDFDocument17 pagesFaa PDFshubham kumarNo ratings yet

- Insurance Accounting TerminologiesDocument16 pagesInsurance Accounting Terminologieskumaryashwant1984No ratings yet

- 2 Final Accounts - Sole Proprietor - Format - AdjustmentsDocument14 pages2 Final Accounts - Sole Proprietor - Format - AdjustmentsSudha Agarwal100% (1)

- Corrected File Unit 2 Final AccountDocument19 pagesCorrected File Unit 2 Final AccountUtkarsh SharmaNo ratings yet

- Partnership Accounts.Document24 pagesPartnership Accounts.Bilal AhmedNo ratings yet

- Financial Accounting AssignentDocument8 pagesFinancial Accounting AssignentHitesh LodayaNo ratings yet

- CH 01 Accounting For Partnership - Basic ConceptsDocument11 pagesCH 01 Accounting For Partnership - Basic ConceptsMahathi AmudhanNo ratings yet

- Accounts Full ConceptsDocument91 pagesAccounts Full ConceptsAnmol BehalNo ratings yet

- Interest On DrawingsDocument2 pagesInterest On DrawingsWelcome 1995No ratings yet

- Notes 2, April 30, 2021 Send To StudentsDocument3 pagesNotes 2, April 30, 2021 Send To StudentsShubham BhaiNo ratings yet

- Assignment 1Document6 pagesAssignment 1Kristo Febrian Suwena -No ratings yet

- Understanding Financial StatementsDocument103 pagesUnderstanding Financial StatementsLawa LopezNo ratings yet

- Ecc Gen MathDocument26 pagesEcc Gen MathloidaNo ratings yet

- Faraj Adayev: Career ObjectiveDocument4 pagesFaraj Adayev: Career ObjectiveAnonymous VCJRrpxNNo ratings yet

- ProblemsDocument46 pagesProblemsDan Andrei BongoNo ratings yet

- Charles P. Jones, Investments: Analysis and Management, Eleventh Edition, John Wiley & SonsDocument23 pagesCharles P. Jones, Investments: Analysis and Management, Eleventh Edition, John Wiley & SonsReza CahyaNo ratings yet

- Ibbl Midaraba Bond Final Report 20.08.06Document8 pagesIbbl Midaraba Bond Final Report 20.08.06Miran shah chowdhury100% (2)

- Final ExamDocument5 pagesFinal ExamSultan LimitNo ratings yet

- George Robbins Considers Himself An Aggressive Investor He S Thinking AboutDocument1 pageGeorge Robbins Considers Himself An Aggressive Investor He S Thinking AboutAmit PandeyNo ratings yet

- Job Costing SampleDocument56 pagesJob Costing SampleFiroz EngineerNo ratings yet

- The Home DepotDocument7 pagesThe Home DepotWawire WycliffeNo ratings yet

- Sources of FinanceDocument28 pagesSources of FinanceShalini Jain0% (1)

- Introduction To Mutual Funds: What Is Mutual Fund? 2. What Are Different Types of Mutual Funds?Document2 pagesIntroduction To Mutual Funds: What Is Mutual Fund? 2. What Are Different Types of Mutual Funds?Rajeev BabuNo ratings yet

- Paul Daugerdas IndictmentDocument79 pagesPaul Daugerdas IndictmentBrian Willingham100% (2)

- Collector of Internal Revenue v. Club Filipino, Inc. de Cebu, GRN-L 12719, May 31, 1962Document2 pagesCollector of Internal Revenue v. Club Filipino, Inc. de Cebu, GRN-L 12719, May 31, 1962Al Jay MejosNo ratings yet

- Merger AcquistionDocument37 pagesMerger AcquistionManjari KumariNo ratings yet

- Zaggle Prepaid Ocean Services Limited - Red Herring Prospectus Dated September 8, 2023Document363 pagesZaggle Prepaid Ocean Services Limited - Red Herring Prospectus Dated September 8, 2023FAIZAL RAZINo ratings yet

- Designing Capital StructureDocument13 pagesDesigning Capital StructuresiddharthdileepkamatNo ratings yet

- Financial Analysis FundamentalsDocument12 pagesFinancial Analysis FundamentalsAni Dwi Rahmanti RNo ratings yet

- Mergers and The Market For Corporate Control - Henry G. ManneDocument11 pagesMergers and The Market For Corporate Control - Henry G. MannedanielNo ratings yet

- Ia 1BDocument553 pagesIa 1BTipsywinkieNo ratings yet

- UITFDocument145 pagesUITFJay Lloyd Banis Domogma100% (1)

- An Error of Collateral Why Selling SPX Put Options May Not Be ProfitableDocument29 pagesAn Error of Collateral Why Selling SPX Put Options May Not Be ProfitableSeaSeaNo ratings yet

- Managing ExpectationsDocument400 pagesManaging Expectationsswaroopr8100% (8)

- (R.A.No. 11232 Revised Corporation Code of The Philippines) Title I General Provisions Definitions and ClassificationsDocument46 pages(R.A.No. 11232 Revised Corporation Code of The Philippines) Title I General Provisions Definitions and ClassificationsGladys De Guzman100% (1)

- TIA Bullet Proof 2022 - NotesDocument27 pagesTIA Bullet Proof 2022 - NotesRohan ShahNo ratings yet

- Entrepreneurial Exit As A Critical Component of The Entrepreneurial ProcessDocument13 pagesEntrepreneurial Exit As A Critical Component of The Entrepreneurial Processaknithyanathan100% (2)

- Caterpillar Presentation Firm AnalysisDocument29 pagesCaterpillar Presentation Firm AnalysisMuhammad Bilal KhanNo ratings yet

- Equities Cllase 1 Junio 2020Document209 pagesEquities Cllase 1 Junio 2020NGOC NHINo ratings yet

- ZLNC 9 ZUQer Ya BBwsu NM NDocument4 pagesZLNC 9 ZUQer Ya BBwsu NM NashibhallauNo ratings yet