You might also like

- Infinite Banking Concept: How to invest in Real Estate with Infinite Banking, #1From EverandInfinite Banking Concept: How to invest in Real Estate with Infinite Banking, #1Rating: 2.5 out of 5 stars2.5/5 (2)

- Financial Basics - Investment OptionsDocument7 pagesFinancial Basics - Investment OptionsSajeed Shaikh100% (1)

- Investments For Section 80CDocument17 pagesInvestments For Section 80CAsħîŞĥLøÝåNo ratings yet

- Equity Linked Savings Scheme (ELSS)Document2 pagesEquity Linked Savings Scheme (ELSS)Anant TutejaNo ratings yet

- All About New Pension SchemeDocument2 pagesAll About New Pension SchemedhirennagareyaNo ratings yet

- Public Provident FundDocument10 pagesPublic Provident FundJubin JainNo ratings yet

- How To Build A Mutual Fund Portfolio: The Debt-Equity RatioDocument10 pagesHow To Build A Mutual Fund Portfolio: The Debt-Equity Ratioparry5000No ratings yet

- Android Training OnlineDocument6 pagesAndroid Training OnlineMindMajix TechnologiesNo ratings yet

- Introduction To AJSDocument44 pagesIntroduction To AJSAmritha SankarNo ratings yet

- A Survey On Methods of Text SummarizationDocument7 pagesA Survey On Methods of Text SummarizationInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Big Data Analytics Question Bank Module 1-5Document3 pagesBig Data Analytics Question Bank Module 1-5Kaushik Kaps100% (1)

- GCC QBDocument16 pagesGCC QBSherril Vincent100% (1)

- Financial For Non Financial CitibanamexDocument147 pagesFinancial For Non Financial CitibanamexRaúl ArellanoNo ratings yet

- ML Question Bank and SolDocument12 pagesML Question Bank and SolPrabhu Prasad DevNo ratings yet

- BDA Lab ManualDocument62 pagesBDA Lab ManualReyansh PerkinNo ratings yet

- Cse-Vii-java and J2EE (10cs753) - Question PaperDocument4 pagesCse-Vii-java and J2EE (10cs753) - Question PaperVrijeshMGNo ratings yet

- Two Mark Questions with AI AnswersDocument14 pagesTwo Mark Questions with AI AnswersAdhithya SrinivasanNo ratings yet

- HCI Foundations SyllabusDocument297 pagesHCI Foundations SyllabusHarshith Kumar ReddyNo ratings yet

- Hci 2mDocument8 pagesHci 2msuganyaNo ratings yet

- Android Lab ProgramsDocument15 pagesAndroid Lab ProgramsSURESHNo ratings yet

- Angular JS: Key Words: - Html5 Course DescriptionDocument7 pagesAngular JS: Key Words: - Html5 Course DescriptiononlineitguruNo ratings yet

- Machinelñearning PDFDocument1,021 pagesMachinelñearning PDFroheru87No ratings yet

- Investment PlanningDocument18 pagesInvestment PlanningNitesh BhaktaNo ratings yet

- UID IT 604 Part ADocument4 pagesUID IT 604 Part Asathyalk81No ratings yet

- Hadoop Online TrainingDocument7 pagesHadoop Online TrainingmsrtrainingsNo ratings yet

- Viii Sem Cs6008 QBDocument12 pagesViii Sem Cs6008 QBGanesh KumarNo ratings yet

- Linear Programming ModelDocument83 pagesLinear Programming ModelYoungsonya JubeckingNo ratings yet

- Tax AuditDocument16 pagesTax AuditArifin FuNo ratings yet

- HCI Lecture 1 Learning Outcomes & ResourcesDocument26 pagesHCI Lecture 1 Learning Outcomes & ResourcesAnila YasmeenNo ratings yet

- Wipro Questions and AnswersDocument3 pagesWipro Questions and AnswerssudharsanankNo ratings yet

- Excel Smart Guide: 80 Tips and Tricks On ExcelDocument41 pagesExcel Smart Guide: 80 Tips and Tricks On ExcelGauri DorbiNo ratings yet

- Ethics of Research in 40 CharactersDocument25 pagesEthics of Research in 40 CharactersDaichi ライアンNo ratings yet

- Activity Based CostingDocument51 pagesActivity Based CostingAbdulyunus AmirNo ratings yet

- AI Unit 1 NotesDocument16 pagesAI Unit 1 NotesYuddhveer SinghNo ratings yet

- Assessment 1 BriefDocument6 pagesAssessment 1 BriefLabiba FarooqNo ratings yet

- Ifrs 9 (Psak 71)Document21 pagesIfrs 9 (Psak 71)Revanty IryaniNo ratings yet

- QB Students DMDocument12 pagesQB Students DMVinay GopalNo ratings yet

- Operations Research: Text Book: Operations Research: An Introduction by Hamdy A.Taha (Pearson Education) 8 EditionDocument34 pagesOperations Research: Text Book: Operations Research: An Introduction by Hamdy A.Taha (Pearson Education) 8 Editionaditya balaNo ratings yet

- Cognizant Java Wrapper Classes Exercise OutputDocument7 pagesCognizant Java Wrapper Classes Exercise OutputJeevan Sai MaddiNo ratings yet

- Financialplanning PresentationDocument24 pagesFinancialplanning PresentationusmanivNo ratings yet

- What Is Social Return On Investment (SROI) and How Do You Apply It?Document4 pagesWhat Is Social Return On Investment (SROI) and How Do You Apply It?Rizwan TayabaliNo ratings yet

- ToC PowerpointDocument21 pagesToC Powerpointhammouda25No ratings yet

- Hci 2 Mark Question Bank Unit 1Document10 pagesHci 2 Mark Question Bank Unit 1Sathya MNo ratings yet

- Cse-Vii-java and J2EE (10cs753) - Question PaperDocument4 pagesCse-Vii-java and J2EE (10cs753) - Question PaperAbhinav JhaNo ratings yet

- Blue Ocean Quick IntroductionDocument26 pagesBlue Ocean Quick IntroductionJohn WaweruNo ratings yet

- Cs9251 Mobile Computing 2marks 16marks Question PapersDocument11 pagesCs9251 Mobile Computing 2marks 16marks Question PapersNivithaNo ratings yet

- Mobile Computing FundamentalsDocument3 pagesMobile Computing FundamentalsMunish RaghavanNo ratings yet

- It6702 Data Warehousing and Data Mining Two Marks With Answer Unit-1 Data Warehousing - Priya Dharsnee - Academia - EduDocument16 pagesIt6702 Data Warehousing and Data Mining Two Marks With Answer Unit-1 Data Warehousing - Priya Dharsnee - Academia - EduLOICE HAZVINEI KUMIRENo ratings yet

- Well House Consultants Samples Notes From Well House Consultants 1Document24 pagesWell House Consultants Samples Notes From Well House Consultants 1ashtikar_prabodh3313100% (1)

- 9872 - Intro To LPP and Its FormulationDocument26 pages9872 - Intro To LPP and Its FormulationSwati Sucharita DasNo ratings yet

- Fundamentals of Business and OrganizationDocument34 pagesFundamentals of Business and OrganizationNoor M Rana100% (1)

- Web Technology Notes DownloadDocument139 pagesWeb Technology Notes DownloadPreet BhattNo ratings yet

- Active Portfolio ManagementDocument7 pagesActive Portfolio ManagementAbhishek KumarNo ratings yet

- BDO PSAK71 Financial Inst RevisiDocument6 pagesBDO PSAK71 Financial Inst RevisiNico Hadi GelianNo ratings yet

- Topic 6 - Linear Programming - Graphical Method 2Document52 pagesTopic 6 - Linear Programming - Graphical Method 2wongh ka manNo ratings yet

- Tax Saving SchemesDocument12 pagesTax Saving Schemesshashikumarb2277No ratings yet

- Tax efficiency of bank deposits vs investments in debt and equity mutual fundsDocument19 pagesTax efficiency of bank deposits vs investments in debt and equity mutual fundsKaruppiah ARNo ratings yet

- Traditional Investing Options for Senior CitizensDocument3 pagesTraditional Investing Options for Senior CitizensIndranilGhoshNo ratings yet

- Why Mutual Funds Beat InflationDocument30 pagesWhy Mutual Funds Beat InflationPuneet SinghNo ratings yet

- Security Analysis and Portfolio Management: - Prof. Samidha AngneDocument44 pagesSecurity Analysis and Portfolio Management: - Prof. Samidha AngneSudhir Kumar AgarwalNo ratings yet

- Initial Appln Format by Seller and BuyerDocument2 pagesInitial Appln Format by Seller and BuyerSukhdarshan Singh BrarNo ratings yet

- Formats - Where Flat Is Regd in Single Name PDFDocument12 pagesFormats - Where Flat Is Regd in Single Name PDFSukhdarshan Singh BrarNo ratings yet

- Check List To Be Referred Before SubmissionDocument2 pagesCheck List To Be Referred Before SubmissionSukhdarshan Singh BrarNo ratings yet

- Check List To Be Referred Before SubmissionDocument2 pagesCheck List To Be Referred Before SubmissionSukhdarshan Singh BrarNo ratings yet

- Guide To Adulting 101 by Paps MDDocument2 pagesGuide To Adulting 101 by Paps MDBen Paolo Cecilia Rabara0% (1)

- Total Amount (In Word) : Rupees Four Hundred Only Total Amount (In Word) : Rupees Four Hundred Only Total Amount (In Word) : Rupees Four Hundred OnlyDocument1 pageTotal Amount (In Word) : Rupees Four Hundred Only Total Amount (In Word) : Rupees Four Hundred Only Total Amount (In Word) : Rupees Four Hundred Onlysaurabhdabas7No ratings yet

- AT05-Planning An Audit of Financial StatementsDocument11 pagesAT05-Planning An Audit of Financial StatementsZyrelle DelgadoNo ratings yet

- World Bank Operations Manual ProceduresDocument12 pagesWorld Bank Operations Manual ProceduresMikhael Yah-Shah Dean: VeilourNo ratings yet

- Organizational Environment of LICDocument9 pagesOrganizational Environment of LICAshok VermaNo ratings yet

- Plane 01Document2 pagesPlane 01kanchan kurmi100% (1)

- S.No Location Building Name Unit No. Floor Unit Status DirectionDocument5 pagesS.No Location Building Name Unit No. Floor Unit Status Directionvijay kumar anantNo ratings yet

- Research MethodologyDocument45 pagesResearch MethodologyDinesh Phadtare100% (6)

- Creditcard StatementDocument3 pagesCreditcard StatementPadma NayakNo ratings yet

- Auto InsuranceDocument5 pagesAuto InsuranceAkshay AggarwalNo ratings yet

- Audit NotesDocument6 pagesAudit NotesJesnyfNo ratings yet

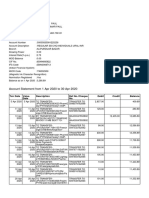

- Account Statement From 1 Apr 2020 To 30 Apr 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Apr 2020 To 30 Apr 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSubham PaulNo ratings yet

- Manzana Insurance FinalDocument11 pagesManzana Insurance Finalratcfc100% (12)

- Bank ManagementDocument198 pagesBank ManagementSooraj Kallooppara0% (1)

- A Study On Home Loans of ICICI bANKDocument57 pagesA Study On Home Loans of ICICI bANKneonradhika77% (31)

- NRB Bank Bangladesh Deposit RateDocument2 pagesNRB Bank Bangladesh Deposit RateAlamin AlexNo ratings yet

- Bill of SaleDocument2 pagesBill of SalefurrbertNo ratings yet

- Add-on Card Application FormDocument2 pagesAdd-on Card Application FormPunitGoNo ratings yet

- AgencyDocument20 pagesAgencyalsamixersNo ratings yet

- How Has HSBC Adapted Its Global Strategy To Operate in China, Both Before and After China's WTO Accession?Document12 pagesHow Has HSBC Adapted Its Global Strategy To Operate in China, Both Before and After China's WTO Accession?Timothy VincentNo ratings yet

- Business Level Strategy of BRAC BankDocument14 pagesBusiness Level Strategy of BRAC BankNavedNo ratings yet

- Goldman Sachs Sample Pitch BookDocument3 pagesGoldman Sachs Sample Pitch BookJesse0% (2)

- Depositories AN:: TopicDocument10 pagesDepositories AN:: TopicMichael PetersonNo ratings yet

- Presented By-Ranjeet Kumar YadavDocument23 pagesPresented By-Ranjeet Kumar YadavSaify Shaik100% (1)

- Broker Service AgreementDocument6 pagesBroker Service AgreementBowie SukphanNo ratings yet

- Non-Life Insurance Net Income 2020Document2 pagesNon-Life Insurance Net Income 2020Ron CatalanNo ratings yet

- Credit Cards in India: A Study of Trends and ImpactsDocument8 pagesCredit Cards in India: A Study of Trends and Impactsrohit100% (1)

- Wire Inst Form 5-07Document1 pageWire Inst Form 5-071291323No ratings yet

- Annexure_V_Version_3_RBI_guidline_CA_opening_29.11.21 Signed Supreme Constructions PartnershipDocument2 pagesAnnexure_V_Version_3_RBI_guidline_CA_opening_29.11.21 Signed Supreme Constructions PartnershipSharath N YaleNo ratings yet

- Procurement of Hexagonal Drill Rod 22 M.M. Dia X 1800 M.M. Length As Per NIT Specification.Document28 pagesProcurement of Hexagonal Drill Rod 22 M.M. Dia X 1800 M.M. Length As Per NIT Specification.sharang shankerNo ratings yet