You might also like

- Thank You For Using Xoom!: Transfer SummaryDocument2 pagesThank You For Using Xoom!: Transfer SummaryChethan WizNo ratings yet

- Unit 1 Comprehensive ProjectDocument21 pagesUnit 1 Comprehensive ProjectJanet Rosario13% (8)

- Campus Deli Case 4Document15 pagesCampus Deli Case 4Ash RamirezNo ratings yet

- Manual For Finance QuestionsDocument56 pagesManual For Finance QuestionssamiraZehra85% (13)

- Unit 1 - QuestionsDocument4 pagesUnit 1 - QuestionsMohanNo ratings yet

- Cases For Insurance Law - Atty. ZarahDocument153 pagesCases For Insurance Law - Atty. ZarahcH3RrY1007No ratings yet

- Dividend Policy QuestionDocument3 pagesDividend Policy Questionraju kumarNo ratings yet

- Tabulation FinalDocument20 pagesTabulation FinalcoolchethanNo ratings yet

- Sushil KumatDocument33 pagesSushil Kumat123456789OOOOOONo ratings yet

- July - September Jobs ReportDocument8 pagesJuly - September Jobs Reportapi-366691262No ratings yet

- NJTC X Alliance BernsteinDocument62 pagesNJTC X Alliance BernsteinAna MazumdarNo ratings yet

- Occupation: No. of Respondent Respondent %Document3 pagesOccupation: No. of Respondent Respondent %keerthanasubramaniNo ratings yet

- China Economic WatchDocument6 pagesChina Economic WatchFabian ChahinNo ratings yet

- Factors Affecting Consumer's Brand Preference of Small Cars: K. Anandh, Dr. K. Shyama SundarDocument5 pagesFactors Affecting Consumer's Brand Preference of Small Cars: K. Anandh, Dr. K. Shyama SundarJhon RayNo ratings yet

- Data Analysis Mutual FundDocument9 pagesData Analysis Mutual Fundjayswalhiralal899No ratings yet

- Fund Flow Statement WorksheetDocument3 pagesFund Flow Statement WorksheetAnish AroraNo ratings yet

- Frequencies: StatisticsDocument24 pagesFrequencies: StatisticsAmelia FitrianiNo ratings yet

- Data 13 QuestionsDocument17 pagesData 13 QuestionsEiksha SunejaNo ratings yet

- Mridul Tiwari - Mridul Tiwari - PGPGM03 - 13 - IE - FMDocument4 pagesMridul Tiwari - Mridul Tiwari - PGPGM03 - 13 - IE - FMekta agarwalNo ratings yet

- Appendix 1Document10 pagesAppendix 1Krishna ShresthaNo ratings yet

- Road Map For The Near Term Performance of The Economy: 50 South Lasalle Chicago, Illinois 60603Document7 pagesRoad Map For The Near Term Performance of The Economy: 50 South Lasalle Chicago, Illinois 60603International Business TimesNo ratings yet

- Traditional Theory Approach: Illustrations 1Document7 pagesTraditional Theory Approach: Illustrations 1PRAMOD VNo ratings yet

- UntitledDocument235 pagesUntitledQuynh VoNo ratings yet

- Ratio Analysis AssignmentDocument3 pagesRatio Analysis Assignmentasinha_30No ratings yet

- Chapter 2Document21 pagesChapter 2JeganNo ratings yet

- Portfolio Management ProblemDocument12 pagesPortfolio Management Problemanisasheikh83No ratings yet

- AF4S31N 2016-17 Assignment 1 V2 CDocument4 pagesAF4S31N 2016-17 Assignment 1 V2 CRegina AtkinsNo ratings yet

- OldvsnewDocument2 pagesOldvsnewda MNo ratings yet

- Accont Dalmia - For MergeDocument8 pagesAccont Dalmia - For Mergesaikatdn555No ratings yet

- Tax Incidence On Partnership Fi RMDocument12 pagesTax Incidence On Partnership Fi RMTejas DesaiNo ratings yet

- Employees' Provident Fund Organization, India: Challan SummaryDocument1 pageEmployees' Provident Fund Organization, India: Challan SummaryAshish ParmarNo ratings yet

- CS Professional DT Revision For Dec 19Document117 pagesCS Professional DT Revision For Dec 19Vineela Srinidhi DantuNo ratings yet

- Iet 603 Assignment 5Document11 pagesIet 603 Assignment 5Poule LipouNo ratings yet

- Financial AccountingDocument8 pagesFinancial AccountingAstridNo ratings yet

- Home Loan Testing FileDocument2 pagesHome Loan Testing Filejitendra tirthyaniNo ratings yet

- TUTORIAL 2 - Hadil TlijaniDocument5 pagesTUTORIAL 2 - Hadil TlijaniHadyl tlijaniNo ratings yet

- FEM PresentationDocument15 pagesFEM PresentationInnocent BhaikwaNo ratings yet

- ATPL10060 - Kolli Sravani - JUNE - 2018 PDFDocument1 pageATPL10060 - Kolli Sravani - JUNE - 2018 PDFsravani kolliNo ratings yet

- MGT 489 100 Global Brands MNQDocument5 pagesMGT 489 100 Global Brands MNQRoseNo ratings yet

- Eacc506 23241 1Document2 pagesEacc506 23241 1Yadav. Vanshika1612No ratings yet

- Future of Us BankingDocument19 pagesFuture of Us Banking5o455999No ratings yet

- EBITDADocument2 pagesEBITDAAshraf Rabie AhmedNo ratings yet

- A Study On Customers' Satisfaction Towards: Lakmé Cosmetics at Ambegaon, PuneDocument25 pagesA Study On Customers' Satisfaction Towards: Lakmé Cosmetics at Ambegaon, PuneMome SinhaNo ratings yet

- Module 2 - StudentsDocument42 pagesModule 2 - StudentsflaviniflaviniNo ratings yet

- AE 111 Midterm Summative Assessment 3 SolutionsDocument12 pagesAE 111 Midterm Summative Assessment 3 SolutionsDjunah ArellanoNo ratings yet

- Ratio AnalysisDocument3 pagesRatio AnalysisYash AgarwalNo ratings yet

- Abhisheksingh - PGDM 2021 - 2023 Bi LabDocument5 pagesAbhisheksingh - PGDM 2021 - 2023 Bi LabAßhïšhëķ ŞiñghNo ratings yet

- 21 Useful Chart - 2020Document40 pages21 Useful Chart - 2020Kiran KudtarkarNo ratings yet

- Employees' Provident Fund Organization, India: Challan SummaryDocument1 pageEmployees' Provident Fund Organization, India: Challan SummaryAshish ParmarNo ratings yet

- Business Model: Expenditure Amount Income AmountDocument2 pagesBusiness Model: Expenditure Amount Income AmountAnkur DharodNo ratings yet

- Market Complacency: The Risk of InactionDocument6 pagesMarket Complacency: The Risk of InactionThinh DoNo ratings yet

- Data Analysis and Interpretation: CH Apter IvDocument35 pagesData Analysis and Interpretation: CH Apter IvDeepak KumarNo ratings yet

- Data AnalysisDocument22 pagesData AnalysisSwyam DuggalNo ratings yet

- Case Study 2Document2 pagesCase Study 2Anil NagarajNo ratings yet

- Project Report For: Royal StarDocument14 pagesProject Report For: Royal StarSUREMAN FINANCIAL SERVICESNo ratings yet

- Wahid Elazhary - Quants 1st AssignmentDocument13 pagesWahid Elazhary - Quants 1st Assignmentwahid.azharyNo ratings yet

- Financial Statement Analysis-2Document12 pagesFinancial Statement Analysis-2Glaidel Rodenas PeñaNo ratings yet

- I II III: in Millions of USD (Year 2013)Document6 pagesI II III: in Millions of USD (Year 2013)Karen May AlonsagayNo ratings yet

- Asia Small and Medium-Sized Enterprise Monitor 2020: Volume II: COVID-19 Impact on Micro, Small, and Medium-Sized Enterprises in Developing AsiaFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2020: Volume II: COVID-19 Impact on Micro, Small, and Medium-Sized Enterprises in Developing AsiaNo ratings yet

- Analysis and InterpretationDocument13 pagesAnalysis and InterpretationSukanya SarmaNo ratings yet

- Analysis and Data Interpretation: Issue1: Value of The Opinions Put Forward by The CustomersDocument14 pagesAnalysis and Data Interpretation: Issue1: Value of The Opinions Put Forward by The CustomersSukanya SarmaNo ratings yet

- Presentation ON Retail Marketing: TopicDocument27 pagesPresentation ON Retail Marketing: TopicSukanya SarmaNo ratings yet

- Presentation On Demografic FactorDocument19 pagesPresentation On Demografic FactorSukanya SarmaNo ratings yet

- Framework of Analysis:: Issue1: Value of The Opinions Put Forward by The CustomersDocument19 pagesFramework of Analysis:: Issue1: Value of The Opinions Put Forward by The CustomersSukanya SarmaNo ratings yet

- Special Thanks To-Mr. Himangshu Tamuly Spectrum Honda, D: IbrugarhDocument1 pageSpecial Thanks To-Mr. Himangshu Tamuly Spectrum Honda, D: IbrugarhSukanya SarmaNo ratings yet

- Honda Motor CompanyDocument8 pagesHonda Motor CompanySukanya SarmaNo ratings yet

- Payroll Direct DepositDocument1 pagePayroll Direct Depositumang parmarNo ratings yet

- Debit CardDocument16 pagesDebit CardAvinash Sahu100% (2)

- Philippine Manufacturing Co. vs. Union InsuranceDocument2 pagesPhilippine Manufacturing Co. vs. Union InsuranceAnny YanongNo ratings yet

- FB - JPM Research Report - Oct 2012Document17 pagesFB - JPM Research Report - Oct 2012ishfaque10No ratings yet

- Presentation On Analysis of Annual Report of State Bank of IndiaDocument18 pagesPresentation On Analysis of Annual Report of State Bank of IndiaRudra PratapNo ratings yet

- A Ibanez Ruling Jdsupra AnalysisDocument2 pagesA Ibanez Ruling Jdsupra AnalysisKelly L. HansenNo ratings yet

- January 2018Document4 pagesJanuary 2018kristel jane caldozaNo ratings yet

- Consortium AdvancesDocument10 pagesConsortium Advancesmedhekar_renukaNo ratings yet

- Actuarial 2Document33 pagesActuarial 2Rochana RamanayakaNo ratings yet

- At.1609 - Audit Planning - An OverviewDocument6 pagesAt.1609 - Audit Planning - An Overviewnaztig_017No ratings yet

- Environmental AnalysisDocument7 pagesEnvironmental Analysisprantik420No ratings yet

- FA1Document11 pagesFA1Ali ParasNo ratings yet

- Chapter 17.ijarahDocument12 pagesChapter 17.ijarahObaid AyubNo ratings yet

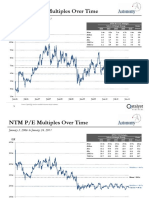

- NTM Revenue Multiples Over Time: January 3, 2006 To January 24, 2011Document3 pagesNTM Revenue Multiples Over Time: January 3, 2006 To January 24, 2011mittleNo ratings yet

- Bharti AXA Policy Document Elite AdvantageDocument12 pagesBharti AXA Policy Document Elite AdvantageSandeepNayakNo ratings yet

- Broking Project Malaysia (Recovered)Document34 pagesBroking Project Malaysia (Recovered)goldhazyyNo ratings yet

- SAP FICO06 General Ledger Accounting Level 2Document61 pagesSAP FICO06 General Ledger Accounting Level 2Jhoanna Mary PescasioNo ratings yet

- The Loans For Agricultural, Commercial and IndustrialDocument5 pagesThe Loans For Agricultural, Commercial and IndustrialShahidHussainBashoviNo ratings yet

- The Indian Internet Banking JourneyDocument4 pagesThe Indian Internet Banking JourneySandeep MishraNo ratings yet

- PPP Client Form 2Document8 pagesPPP Client Form 2prekyNo ratings yet

- Thesis On Mutual FundDocument185 pagesThesis On Mutual Fundsidhantha83% (6)

- Fieldmen Insurance v. Vda. de SongcoDocument2 pagesFieldmen Insurance v. Vda. de SongcoMariella Grace AllanicNo ratings yet

- Financial Institution of BangladeshDocument7 pagesFinancial Institution of BangladeshPranto BaruaNo ratings yet

- Product Liability Insurance Application FormDocument2 pagesProduct Liability Insurance Application FormMd. Rakibul IslamNo ratings yet

- 8D Template Hussey Schnaider FormatDocument37 pages8D Template Hussey Schnaider FormatJuan Carlos Lekuona-Muñoz CarrilloNo ratings yet

- World Bank Data CatalogDocument42 pagesWorld Bank Data CatalogRaoNo ratings yet

- ISDA Collateral Glossary Chinese TransDocument23 pagesISDA Collateral Glossary Chinese TransWei Wang100% (2)