You might also like

- Sterilized Intervention As A Complementary Macroprudential MeasureDocument21 pagesSterilized Intervention As A Complementary Macroprudential MeasureADBI EventsNo ratings yet

- Highlights of Monitary Policy 2020Document15 pagesHighlights of Monitary Policy 2020Raushan KumarNo ratings yet

- Personal Financial Planning: End-Term ProjectDocument12 pagesPersonal Financial Planning: End-Term ProjectPoloJ20No ratings yet

- FY 2021-22 State Planning Document SummaryDocument18 pagesFY 2021-22 State Planning Document SummaryVivek Vishal GiriNo ratings yet

- Statement Showing The Demand Collection and Balance Upto July 2021Document3 pagesStatement Showing The Demand Collection and Balance Upto July 2021Ponnam VenkateshamNo ratings yet

- Announced by The Bank From Time To Time. Current Accounts Will Be Based On Qard. Saving Accounts and Islamic Term Deposits Will Be Based On MudarabahDocument2 pagesAnnounced by The Bank From Time To Time. Current Accounts Will Be Based On Qard. Saving Accounts and Islamic Term Deposits Will Be Based On Mudarabahhussainchotto75No ratings yet

- Budget Presentation: Budget For The Year 2018Document15 pagesBudget Presentation: Budget For The Year 2018Arif IslamNo ratings yet

- Philbin Financial Group: To Provide A Graphical Summary of The Portfolio Prospectus For The Sunrise FundDocument13 pagesPhilbin Financial Group: To Provide A Graphical Summary of The Portfolio Prospectus For The Sunrise FundTTV TimeKpRNo ratings yet

- Financial Analysis Reveals Canara Bank's StrugglesDocument13 pagesFinancial Analysis Reveals Canara Bank's StrugglesSattwik rathNo ratings yet

- VIX Jan 1991 - Jan 2020Document10 pagesVIX Jan 1991 - Jan 2020kuky6549369No ratings yet

- Mutual FundDocument5 pagesMutual FundMunaj AzharNo ratings yet

- SchwartzMoon (2000) Rational Pricing Internet CpyDocument14 pagesSchwartzMoon (2000) Rational Pricing Internet Cpyapi-3763138No ratings yet

- Where Is The World Economy Heading?Document56 pagesWhere Is The World Economy Heading?Paresh Pabaria100% (1)

- KFS HBL Islamic Saving Account Bilingual June22Document4 pagesKFS HBL Islamic Saving Account Bilingual June22Tatheer ZeeshanNo ratings yet

- Key Fact Statement For Deposit Accounts: To OpenDocument4 pagesKey Fact Statement For Deposit Accounts: To OpenMaqsood akhtarNo ratings yet

- AChawla AUS Practice Set Education - Profit and LossDocument1 pageAChawla AUS Practice Set Education - Profit and Losssimran chawlaNo ratings yet

- KPI - Nov 2019 - Area164Document9 pagesKPI - Nov 2019 - Area164AAKP Law FirmNo ratings yet

- fm1 Assi GraphDocument1 pagefm1 Assi GraphVanishree KamarajeeNo ratings yet

- Philbin Financial Group: To Provide A Graphical Summary of The Portfolio Prospectus For The Sunrise FundDocument13 pagesPhilbin Financial Group: To Provide A Graphical Summary of The Portfolio Prospectus For The Sunrise FundSALIL SHANKARNo ratings yet

- Bridgewater ReportDocument12 pagesBridgewater Reportw_fibNo ratings yet

- Nikkei Average 1989-2008Document15 pagesNikkei Average 1989-2008api-26172897No ratings yet

- Financial CalculatorDocument58 pagesFinancial CalculatorAngela HarringtonNo ratings yet

- Home Budget PlannerDocument137 pagesHome Budget Plannerjiguparmar1516No ratings yet

- Onthly Utlook: U.S. Overview International OverviewDocument6 pagesOnthly Utlook: U.S. Overview International OverviewInternational Business TimesNo ratings yet

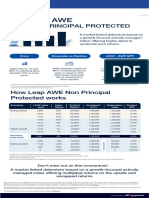

- LEAP AWE NPP - FinalDocument1 pageLEAP AWE NPP - Finalvikyraj0420No ratings yet

- 1Q2020 Fullbook enDocument53 pages1Q2020 Fullbook enVincentNo ratings yet

- Quality Valuation: Update Harga: Real-TimeDocument13 pagesQuality Valuation: Update Harga: Real-TimeambarNo ratings yet

- Wind Power Valuation ModelDocument9 pagesWind Power Valuation ModelManoj AswaniNo ratings yet

- KFS HBL Islamic Saving Account Bilingual Jan-2022Document4 pagesKFS HBL Islamic Saving Account Bilingual Jan-2022Tatheer ZeeshanNo ratings yet

- Eicher Motors LTD: DCF Analysis Valuation Date: 13 March, 2019Document60 pagesEicher Motors LTD: DCF Analysis Valuation Date: 13 March, 2019CharanjitNo ratings yet

- HDFC Asset Allocator Fund of Funds - NFO LeafletDocument4 pagesHDFC Asset Allocator Fund of Funds - NFO LeafletJignesh PatelNo ratings yet

- 4.1 Consumer FinanceDocument11 pages4.1 Consumer Financeyodhraj_sharmaNo ratings yet

- (Company) : Basic Exit Multiples Cash SweepDocument26 pages(Company) : Basic Exit Multiples Cash Sweepw_fibNo ratings yet

- Home Loan Emi - How Much Your Home Loan EMI Will Increase After RBI's 40 Bps Repo Rate Hike - The Economic VDocument2 pagesHome Loan Emi - How Much Your Home Loan EMI Will Increase After RBI's 40 Bps Repo Rate Hike - The Economic VRaktim dattaNo ratings yet

- Bond Yields and Prices: Reference: Chapter 17Document30 pagesBond Yields and Prices: Reference: Chapter 17RosaNo ratings yet

- Understanding The Recent Monetary Policy and What It Entails For The Nigerian Economy - Ugochukwu AnthonyDocument10 pagesUnderstanding The Recent Monetary Policy and What It Entails For The Nigerian Economy - Ugochukwu Anthonyabdulbasitabdulazeez30No ratings yet

- KPI Green EnergyDocument34 pagesKPI Green EnergyRJNo ratings yet

- Finance Part ADocument3 pagesFinance Part ASmita ShresthaNo ratings yet

- Formato EnglishDocument3 pagesFormato EnglishArgenis VaraNo ratings yet

- CCIM Financial Calculator V 6.0Document63 pagesCCIM Financial Calculator V 6.0Wade KellyNo ratings yet

- CAW's Jim Stanford: Canada 2020 Pre-Budget Debate 2011Document20 pagesCAW's Jim Stanford: Canada 2020 Pre-Budget Debate 2011Canada 2020 - Canada's Progressive CentreNo ratings yet

- Aviva UK: One Aviva Twice The ValueDocument17 pagesAviva UK: One Aviva Twice The ValueAviva GroupNo ratings yet

- Cap+TableDocument1 pageCap+TableexamatchNo ratings yet

- Investment ValuationDocument11 pagesInvestment Valuationcontact7809No ratings yet

- Advance Financial Accounting Assignment AliDocument36 pagesAdvance Financial Accounting Assignment AliFarjad AliNo ratings yet

- Financial Risk ManagementDocument30 pagesFinancial Risk ManagementVarun Kumar ChalotraNo ratings yet

- Q322 Earnings SummaryDocument1 pageQ322 Earnings Summaryashokdb2kNo ratings yet

- Five Key QuestionsDocument12 pagesFive Key QuestionsInternational Business TimesNo ratings yet

- PrudentialDocument3 pagesPrudentialGiaKhươngTrầnNo ratings yet

- CCIM Financial Calculator V 7 1Document60 pagesCCIM Financial Calculator V 7 1rclemente01No ratings yet

- FM TemplateDocument40 pagesFM TemplateDishani MaityNo ratings yet

- Tracking How Small Finance Banks Advance Financial InclusionDocument30 pagesTracking How Small Finance Banks Advance Financial InclusionNeelanjan MaitiNo ratings yet

- PNRA Panera Bread 2016 Annual Shareholder PresentationDocument46 pagesPNRA Panera Bread 2016 Annual Shareholder PresentationAla BasterNo ratings yet

- S&P Default Rates and Recovery Jan07Document9 pagesS&P Default Rates and Recovery Jan07gimy2010No ratings yet

- Managing Interest Rate RiskDocument25 pagesManaging Interest Rate RiskIqrä QurëshìNo ratings yet

- GAP Interest Rate Change in Interest Income in Relation With Change in Interest ExpenseDocument5 pagesGAP Interest Rate Change in Interest Income in Relation With Change in Interest ExpenseTACN-4TC-19ACN Nguyen Thu HienNo ratings yet

- Mutual Funds Monthly February 2023 - YESSDocument6 pagesMutual Funds Monthly February 2023 - YESSAnkit PandeNo ratings yet

- GS Inflation Implementation 10-20Document20 pagesGS Inflation Implementation 10-20bobmezzNo ratings yet

- Request ListDocument13 pagesRequest ListRizky FadilahNo ratings yet

- Financial Soundness Indicators for Financial Sector Stability in BangladeshFrom EverandFinancial Soundness Indicators for Financial Sector Stability in BangladeshNo ratings yet

- IMP Indicators BEARDocument1 pageIMP Indicators BEARsandipktNo ratings yet

- Essentials of Horary Astrology or Prasnapadavi - R. BhatDocument456 pagesEssentials of Horary Astrology or Prasnapadavi - R. BhatJyotish Freedom93% (14)

- Vedic Astrology Remedies For Hurdles in Professional SuccesDocument38 pagesVedic Astrology Remedies For Hurdles in Professional Succesimabhinav19738No ratings yet

- Vol 8 The Book of Ayurveda and Astrology Ayurvedajyotishgranthamala by Kavyakantha Ganapati MuniDocument133 pagesVol 8 The Book of Ayurveda and Astrology Ayurvedajyotishgranthamala by Kavyakantha Ganapati MunisandipktNo ratings yet

- Vedic Astrology Remedies For Hurdles in Professional SuccesDocument38 pagesVedic Astrology Remedies For Hurdles in Professional Succesimabhinav19738No ratings yet

- The Use of Fixed Stars in AstrologyDocument319 pagesThe Use of Fixed Stars in AstrologyANTHONY WRITER90% (29)

- IMP Indicators BEARDocument1 pageIMP Indicators BEARsandipktNo ratings yet

- Palmistry Lines of Hand Part3Document249 pagesPalmistry Lines of Hand Part3rameshctlatpNo ratings yet

- A Note On The Five Year Yuga of The Vedanta Jyotisa PDFDocument8 pagesA Note On The Five Year Yuga of The Vedanta Jyotisa PDFsathyam66No ratings yet

- Past Life YogaDocument17 pagesPast Life YogaViditJain100% (9)

- Nakshatras GurmeetsinghDocument7 pagesNakshatras GurmeetsinghKishan VarshneyNo ratings yet

- Which Way NowDocument10 pagesWhich Way NowJm2345234029No ratings yet

- Asset Allocator Fund KotakDocument79 pagesAsset Allocator Fund KotaksandipktNo ratings yet

- Investors - Mutual FundDocument27 pagesInvestors - Mutual FundSandip KunduNo ratings yet

- Election Poll Place LocationsDocument92 pagesElection Poll Place LocationssandipktNo ratings yet

- Primer On Universal Basic IncomeDocument7 pagesPrimer On Universal Basic IncomeSamarth MathurNo ratings yet

- India AMCDocument1 pageIndia AMCsandipktNo ratings yet

- Expat TaxationDocument91 pagesExpat TaxationsandipktNo ratings yet

- CRISIL Insights Into India's Growing Corporate Bond MarketDocument108 pagesCRISIL Insights Into India's Growing Corporate Bond Marketafaque khanNo ratings yet

- Fund Formation Attracting Global InvestorsDocument82 pagesFund Formation Attracting Global InvestorssandipktNo ratings yet

- Nvesting in Pandemic Markets: Montgomery Investment ManagementDocument9 pagesNvesting in Pandemic Markets: Montgomery Investment ManagementsandipktNo ratings yet

- Ares Investor Presentation: March 2018Document37 pagesAres Investor Presentation: March 2018sandipktNo ratings yet

- Expat TaxationDocument91 pagesExpat TaxationsandipktNo ratings yet

- Dave Rosenberg 2018 Economic OutlookDocument9 pagesDave Rosenberg 2018 Economic OutlooksandipktNo ratings yet

- The Great Financial Crisis of 1914 - What Can WeDocument10 pagesThe Great Financial Crisis of 1914 - What Can Wehunghl9726No ratings yet

- Lumber: Worth Its Weight in Gold: Offense and DefenseDocument6 pagesLumber: Worth Its Weight in Gold: Offense and DefensesandipktNo ratings yet

- Key Things To Know When Registering A LLP - The Economic Times PDFDocument2 pagesKey Things To Know When Registering A LLP - The Economic Times PDFsandipktNo ratings yet

- FR (Final) PDFDocument264 pagesFR (Final) PDFfabrignani@yahoo.com100% (1)

- How To Dissolve An LLC in Texas - NoloDocument6 pagesHow To Dissolve An LLC in Texas - NolosandipktNo ratings yet

- 189-Article Text-732-1-10-20230322Document5 pages189-Article Text-732-1-10-20230322Brian GiriNo ratings yet

- Chapter Five: The Financial Statements of Banks and Their Principal CompetitorsDocument35 pagesChapter Five: The Financial Statements of Banks and Their Principal CompetitorsmskskkdNo ratings yet

- Revision Test 1 2021Document3 pagesRevision Test 1 2021Gragnor PrideNo ratings yet

- 6 Main Investment Types & Mutual Fund BasicsDocument7 pages6 Main Investment Types & Mutual Fund BasicsSuneranirav DonNo ratings yet

- 8549 18097 1 PBDocument9 pages8549 18097 1 PBfahranyNo ratings yet

- The Term Structure of Interest RatesDocument34 pagesThe Term Structure of Interest RatesCarlos QuinteroNo ratings yet

- Money Universidad de GuanajuatoDocument2 pagesMoney Universidad de GuanajuatoAbraham Morales FloresNo ratings yet

- Black Scholes Option Pricing Model For Selected StocksDocument12 pagesBlack Scholes Option Pricing Model For Selected StocksAyushmaan ChatterjeeNo ratings yet

- Exchange RatesDocument10 pagesExchange RatesMinhaj TariqNo ratings yet

- IDFC Factsheet April 2021 - 3Document70 pagesIDFC Factsheet April 2021 - 3completebhejafryNo ratings yet

- Derivatives As Risk Management Tool For CorporatesDocument86 pagesDerivatives As Risk Management Tool For CorporatesCharu ModiNo ratings yet

- Question: AMH Co: EquityDocument19 pagesQuestion: AMH Co: EquityShamsuzzaman SunNo ratings yet

- Risk Management Surveillance at Ludhiana Stock ExchangeDocument99 pagesRisk Management Surveillance at Ludhiana Stock Exchangepritpal singhNo ratings yet

- Communiques - DP - DP 668 Securities Admitted With CDSL 15112023Document10 pagesCommuniques - DP - DP 668 Securities Admitted With CDSL 15112023Mudit NawaniNo ratings yet

- Monetary Policy: Name: Avinash Roll No. 2K18Bfs04Document18 pagesMonetary Policy: Name: Avinash Roll No. 2K18Bfs04Avinash Gogu100% (1)

- Chapter 16 (29) Practice Test: The Monetary System: Multiple ChoiceDocument11 pagesChapter 16 (29) Practice Test: The Monetary System: Multiple ChoiceRaymund GatocNo ratings yet

- Wise Transaction Invoice Transfer 587693945 799370523 enDocument3 pagesWise Transaction Invoice Transfer 587693945 799370523 enIstiak DeveloperNo ratings yet

- AS-20 QuestionDocument7 pagesAS-20 QuestionDeepthi R TejurNo ratings yet

- 6Document1 page6akbar cuakkNo ratings yet

- Mba Finance Project TopicsDocument10 pagesMba Finance Project TopicsAbhishek M Mumbai0% (1)

- Bitcoin - Review of LiteratureDocument27 pagesBitcoin - Review of LiteratureNeha ChhabdaNo ratings yet

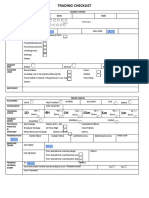

- Trading Checklist BH v2Document2 pagesTrading Checklist BH v2Tong SepamNo ratings yet

- A Complete Guide To Amazon For VendorsDocument43 pagesA Complete Guide To Amazon For Vendorsnissay99No ratings yet

- FINANCIAL STATEMENT ANALYSIS - Practice Set PDFDocument4 pagesFINANCIAL STATEMENT ANALYSIS - Practice Set PDFDwight Manikan EchagueNo ratings yet

- Glacier Funding V CDO Term SheetDocument2 pagesGlacier Funding V CDO Term Sheetthe_akinitiNo ratings yet

- BCIfactsheet Nov 10Document2 pagesBCIfactsheet Nov 10Daplet ChrisNo ratings yet

- You're Welcome Planet Earth The Most Powerful Trading System PDFDocument44 pagesYou're Welcome Planet Earth The Most Powerful Trading System PDFLibert YoungNo ratings yet

- Template 01 Customer Relationship ManagementDocument17 pagesTemplate 01 Customer Relationship ManagementFahmi AriyadiNo ratings yet

- Case FubukiDocument1 pageCase FubukiSumayya ChughtaiNo ratings yet

- Trade The Pool - EbookDocument21 pagesTrade The Pool - EbookFelipe VeritaNo ratings yet