You might also like

- Damodaran On ValuationDocument102 pagesDamodaran On Valuationgioro_mi100% (4)

- Invest in Debt Securities GuideDocument31 pagesInvest in Debt Securities GuideJohn Francis Idanan100% (1)

- Term Loan ProcedureDocument5 pagesTerm Loan ProcedureHardik Sharma100% (1)

- Investment PropertyDocument26 pagesInvestment PropertyKimivy BusaNo ratings yet

- Reporting of Long-Lived Assets/PPE/Fixed AssetsDocument6 pagesReporting of Long-Lived Assets/PPE/Fixed AssetsAnishaSapraNo ratings yet

- Property, Plant and Equipment FundamentalsDocument13 pagesProperty, Plant and Equipment FundamentalsDenmark CabadduNo ratings yet

- P7 - Investment in Debt Securities & Other Non-Current Financial AssetsDocument46 pagesP7 - Investment in Debt Securities & Other Non-Current Financial AssetsNashiel AnneNo ratings yet

- The Merits of An Asset-BasedDocument4 pagesThe Merits of An Asset-Basedanna maeNo ratings yet

- 2.8 Answers To Check Your Proglxess: Compound InterestDocument16 pages2.8 Answers To Check Your Proglxess: Compound InterestTushar SharmaNo ratings yet

- Investment in Debt SecuritiesDocument29 pagesInvestment in Debt SecuritiesDjunah ArellanoNo ratings yet

- Topic 4 - Completing The Accounting CycleDocument52 pagesTopic 4 - Completing The Accounting CycleLA Syamsul100% (1)

- 55 Comparison of Accounting AssumptionsDocument8 pages55 Comparison of Accounting Assumptionsmanoranjan838241No ratings yet

- FAR Handout Investment PropertyDocument4 pagesFAR Handout Investment PropertyPIOLA CAPINANo ratings yet

- IFRS 9 Part 2Document24 pagesIFRS 9 Part 2ErslanNo ratings yet

- 2020 2021 Adv Fin 10 Company Valuation and Financing DecisionsDocument108 pages2020 2021 Adv Fin 10 Company Valuation and Financing DecisionsCharbel HatemNo ratings yet

- Chapter 7 Cashflow ApproachDocument21 pagesChapter 7 Cashflow ApproachINTAN NURLIANA ISMAILNo ratings yet

- Capitalization: Capital Vs Operating LeaseDocument2 pagesCapitalization: Capital Vs Operating Leasejohnsmith12312312312No ratings yet

- SALE AND LEASEBACK TRANSACTIONDocument6 pagesSALE AND LEASEBACK TRANSACTIONJoan BartolomeNo ratings yet

- Cours - 2018Document103 pagesCours - 2018Salahoudini MohamadouNo ratings yet

- Lecture 4 - Accounting analysis 2Document30 pagesLecture 4 - Accounting analysis 2JF FNo ratings yet

- Capital Structure and Leverage ExplainedDocument33 pagesCapital Structure and Leverage Explainedasif rahanNo ratings yet

- #22 Revaluation & Impairment (Notes For 6206)Document5 pages#22 Revaluation & Impairment (Notes For 6206)Claudine DuhapaNo ratings yet

- Initial Measurement at Cost.: Property, Plant and EquipmentDocument5 pagesInitial Measurement at Cost.: Property, Plant and EquipmentCarms St ClaireNo ratings yet

- Tangible NCA V7Document18 pagesTangible NCA V7David JosephNo ratings yet

- Depreciation: Definitions of ValueDocument5 pagesDepreciation: Definitions of ValueRonald Renon QuiranteNo ratings yet

- Unit-Iii, CocDocument37 pagesUnit-Iii, CocSunidhi ChauhanNo ratings yet

- Topic 2. Discounting: Future ValueDocument13 pagesTopic 2. Discounting: Future ValueАндрей ДымовNo ratings yet

- Notes DepreciationDocument6 pagesNotes DepreciationFranshwa SalcedoNo ratings yet

- Payback Period Original Investment Annual Cash Flows Assuming Equal Cashflows)Document1 pagePayback Period Original Investment Annual Cash Flows Assuming Equal Cashflows)Lily HandsNo ratings yet

- IRR, NPV & MIRR Introduction PDFDocument9 pagesIRR, NPV & MIRR Introduction PDFhenryNo ratings yet

- Chapter 4 Introduction To DCFDocument10 pagesChapter 4 Introduction To DCFELVEVIYONA JOOTNo ratings yet

- Cours - 2018Document103 pagesCours - 2018Awalou MohamadNo ratings yet

- Ch3 IAS40 Investment PropertyDocument31 pagesCh3 IAS40 Investment Propertyxu l100% (1)

- Finance PDFDocument136 pagesFinance PDFjariyarasheedNo ratings yet

- Chapter11 PDFDocument25 pagesChapter11 PDFBabuM ACC FIN ECONo ratings yet

- Managerial Economics: An Analysis of Business IssuesDocument25 pagesManagerial Economics: An Analysis of Business IssuesMamta GanatwarNo ratings yet

- SS&C GlobeOp - FA ModuleDocument34 pagesSS&C GlobeOp - FA ModuleAnil Dube100% (1)

- Conceptual Framework and Accounting Standards Q A 4Document5 pagesConceptual Framework and Accounting Standards Q A 4James DetallaNo ratings yet

- Discount RateDocument9 pagesDiscount RateNguyễn PhúcNo ratings yet

- Topic 3 - IAS 36Document15 pagesTopic 3 - IAS 36antran.31201025723No ratings yet

- Property Plant and Equipment (PPE) : Ind AS 16Document31 pagesProperty Plant and Equipment (PPE) : Ind AS 16Himanshu Gaur100% (1)

- Cost of Capital: Hes Gni Icance of C Ca I ADocument15 pagesCost of Capital: Hes Gni Icance of C Ca I AAbbas OmmiiNo ratings yet

- Corporate Finance Equations Notes 5Document13 pagesCorporate Finance Equations Notes 5Sotiris HarisNo ratings yet

- Cash Price Equivalent at The Deferred Beyond Normal CreditDocument5 pagesCash Price Equivalent at The Deferred Beyond Normal CreditSharmin ReulaNo ratings yet

- PPE Acquisition MethodsDocument5 pagesPPE Acquisition MethodsSharmin ReulaNo ratings yet

- 7 - Adjusting EntriesDocument28 pages7 - Adjusting EntriesBianca RoswellNo ratings yet

- ES6 Lec07a Depreciation Straight Line MethodDocument15 pagesES6 Lec07a Depreciation Straight Line MethodIroha IsshikiNo ratings yet

- Chapter 23 - PpeDocument13 pagesChapter 23 - PpeRosee D.No ratings yet

- Revaluation 0Document26 pagesRevaluation 0pam pamNo ratings yet

- Cost of CapitalDocument74 pagesCost of CapitalHarnitNo ratings yet

- Valuation FundamentalsDocument54 pagesValuation FundamentalsMaxNo ratings yet

- Cost of Capital NotesDocument34 pagesCost of Capital Notesyahspal singhNo ratings yet

- CHAPTER 10 - PROPERTY, PLANT AND EQUIPMENT (v2)Document20 pagesCHAPTER 10 - PROPERTY, PLANT AND EQUIPMENT (v2)VerrelyNo ratings yet

- CAPITAL GAINS REVISION (Part 2)Document31 pagesCAPITAL GAINS REVISION (Part 2)Mana SharmaNo ratings yet

- Learning ResourceDocument5 pagesLearning ResourceRemedios Capistrano CatacutanNo ratings yet

- CA Intermediate Solutions for Accounting Nov 2022 ExamDocument31 pagesCA Intermediate Solutions for Accounting Nov 2022 ExamSUMANTO BARMANNo ratings yet

- Solution CMA December 2019 ExamDocument10 pagesSolution CMA December 2019 ExamF A Saffat RahmanNo ratings yet

- Comparison of IAS 7 and PAS 7Document2 pagesComparison of IAS 7 and PAS 7Julia Villanueva100% (1)

- CH 09Document37 pagesCH 09Gaurav KarkiNo ratings yet

- Lesson 12Document6 pagesLesson 12Jamaica bunielNo ratings yet

- State Wise Police Awardees ListDocument2 pagesState Wise Police Awardees ListHeaven ViewsNo ratings yet

- Philips HeartStart MRXDocument1 pagePhilips HeartStart MRXPaulinaNo ratings yet

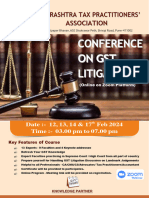

- Conference On GST Litigation-2024Document6 pagesConference On GST Litigation-2024tsdhameliya1No ratings yet

- HPSSC Junior Draughtsman Recruitment AddendumDocument1 pageHPSSC Junior Draughtsman Recruitment Addendumvj_negiNo ratings yet

- Business Plan Template For AfterSchool ProgramsDocument6 pagesBusiness Plan Template For AfterSchool Programsshelana BarzeyNo ratings yet

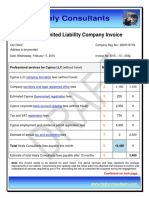

- Draft Invoice Cyprus LLC MigrationDocument7 pagesDraft Invoice Cyprus LLC MigrationShehryar KhanNo ratings yet

- JudaismDocument42 pagesJudaismDhyna TabinNo ratings yet

- FSA Midterm Exam FormattedDocument8 pagesFSA Midterm Exam Formattedkarthikmaddula007_66No ratings yet

- Epson Surecolor S30670: Quick Reference Guide Guía de Referencia Rápida Guia de Referência RápidaDocument111 pagesEpson Surecolor S30670: Quick Reference Guide Guía de Referencia Rápida Guia de Referência RápidaVinicius MeversNo ratings yet

- Black Experience Final Exam Cheat SheetDocument8 pagesBlack Experience Final Exam Cheat SheetHannah LeeNo ratings yet

- 9146-TRAFI 12134 03 04 01 00 2011 EN ReittisuunnitteluDocument4 pages9146-TRAFI 12134 03 04 01 00 2011 EN ReittisuunnitteluMihaela Dma0% (1)

- Intermediate Accounting 1 - InventoriesDocument9 pagesIntermediate Accounting 1 - InventoriesLien LaurethNo ratings yet

- Authorization To Use and Charge Credit Card 1 1Document1 pageAuthorization To Use and Charge Credit Card 1 1Raine Nathalia Cruzat0% (1)

- Subsea Connectivity Leaders GatherDocument7 pagesSubsea Connectivity Leaders GatherAnonymous TVdKmkNo ratings yet

- Subanon Tribe Question Set.Document1 pageSubanon Tribe Question Set.MARK BRIAN FLORESNo ratings yet

- (CPR) Collantes v. MabutiDocument5 pages(CPR) Collantes v. MabutiChristian Edward Coronado50% (2)

- Andres V. MajaduconDocument2 pagesAndres V. MajaduconLeidi Chua BayudanNo ratings yet

- Burning The HouseDocument47 pagesBurning The HouseAnny AunNo ratings yet

- Gable Shed Plan: Free Streamlined VersionDocument9 pagesGable Shed Plan: Free Streamlined VersionjesusdoliNo ratings yet

- Course PlanDocument3 pagesCourse PlannurNo ratings yet

- Crash Course: Wolf Girl 7 by Anh Do Chapter SamplerDocument10 pagesCrash Course: Wolf Girl 7 by Anh Do Chapter SamplerAllen & UnwinNo ratings yet

- PDFDocument9 pagesPDFRajendra Patil26% (31)

- Business LettersDocument15 pagesBusiness Lettersgzel07No ratings yet

- Attachment B - MSDS Fibagel UV LV ResinDocument4 pagesAttachment B - MSDS Fibagel UV LV ResinAlam MD SazidNo ratings yet

- COL Syllabus - 17-18 - Senchi VersionDocument9 pagesCOL Syllabus - 17-18 - Senchi VersionTimore FrancisNo ratings yet

- Chapter 5 - Books of Accounts & Double-Entry SystemDocument16 pagesChapter 5 - Books of Accounts & Double-Entry SystemhiroNo ratings yet

- Lea 2Document2 pagesLea 2Rosaly Bontia100% (1)

- Red670 1.2Document1,232 pagesRed670 1.2André SuzukiNo ratings yet

- Week 7-Virtue Ethics of AristotleDocument27 pagesWeek 7-Virtue Ethics of AristotleNikki MallariNo ratings yet