You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- November 2020 and February 2021 Strategic Case Study Examination Pre-SeenDocument24 pagesNovember 2020 and February 2021 Strategic Case Study Examination Pre-SeenMuhammad SadiqNo ratings yet

- Chapter 8 Solution Manual of Managerial Accounting Ronald HiltonDocument46 pagesChapter 8 Solution Manual of Managerial Accounting Ronald HiltonMuhammad Sadiq50% (8)

- Chap 001Document17 pagesChap 001redspyderxNo ratings yet

- Understanding Modarabah Companies and Modarabahs in PakistanDocument17 pagesUnderstanding Modarabah Companies and Modarabahs in PakistanMuhammad SadiqNo ratings yet

- Understanding Modarabah Companies and Modarabahs in PakistanDocument17 pagesUnderstanding Modarabah Companies and Modarabahs in PakistanMuhammad SadiqNo ratings yet

- Chap 001Document17 pagesChap 001redspyderxNo ratings yet

- Chap 001Document17 pagesChap 001redspyderxNo ratings yet

- Journal Entries For VariancesDocument7 pagesJournal Entries For VariancesMuhammad SadiqNo ratings yet

- Flexibla BudgetsDocument44 pagesFlexibla BudgetsMuhammad SadiqNo ratings yet

- Financial Statement AnalysisDocument85 pagesFinancial Statement AnalysisMuhammad SadiqNo ratings yet

- MA Study Support Guide: Plan Prepare PassDocument26 pagesMA Study Support Guide: Plan Prepare PassMuhammad SadiqNo ratings yet

- Flexibla BudgetsDocument44 pagesFlexibla BudgetsMuhammad SadiqNo ratings yet

- Chap 001Document17 pagesChap 001redspyderxNo ratings yet

- Income Taxes in Capital Budgeting Decisions: Appendix 13CDocument15 pagesIncome Taxes in Capital Budgeting Decisions: Appendix 13CMuhammad SadiqNo ratings yet

- Study Guide For F5Document19 pagesStudy Guide For F5Muhammad SadiqNo ratings yet

- Financial Statement AnalysisDocument85 pagesFinancial Statement AnalysisMuhammad SadiqNo ratings yet

- Acca F5 Document FileDocument12 pagesAcca F5 Document Filesadiq626No ratings yet

- Financial Management (F9) September 2017 To June 2018Document14 pagesFinancial Management (F9) September 2017 To June 2018Ed TeddyNo ratings yet

- Ma1 Management InformationDocument9 pagesMa1 Management InformationLola0% (1)

- Important Study FileDocument11 pagesImportant Study FileMuhammad SadiqNo ratings yet

- F5-Sg-Sept15-Jun 16Document12 pagesF5-Sg-Sept15-Jun 16ifeeNo ratings yet

- P2 AW Interactive 4966 Study GuideDocument30 pagesP2 AW Interactive 4966 Study GuideMuhammad SadiqNo ratings yet

- P5 Plan of StudyDocument5 pagesP5 Plan of StudyMuhammad SadiqNo ratings yet

- P7 Unit PlanDocument7 pagesP7 Unit PlanMuhammad SadiqNo ratings yet

- P4 Unit PlanDocument4 pagesP4 Unit PlanMuhammad SadiqNo ratings yet

- As and A Level AccountingDocument33 pagesAs and A Level AccountingMuhammad Sadiq80% (5)

- Accountant in Business (FAB:F1) September 2016 To August 2017Document15 pagesAccountant in Business (FAB:F1) September 2016 To August 2017LolaNo ratings yet

- Business Studies 2014Document30 pagesBusiness Studies 2014Muhammad SadiqNo ratings yet

- Principle of Ac 2014Document21 pagesPrinciple of Ac 2014Muhammad SadiqNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- TYPES of TEXT Translation As An Art - MagazineDocument40 pagesTYPES of TEXT Translation As An Art - MagazineasilNo ratings yet

- Admission of A PartnerDocument5 pagesAdmission of A PartnerHigreeve SrudhiNo ratings yet

- Chapter 6: Foreign Currency Translation: International Accounting, 6/eDocument29 pagesChapter 6: Foreign Currency Translation: International Accounting, 6/eSylvia Al-a'maNo ratings yet

- Timber Sell Business PlanDocument34 pagesTimber Sell Business PlanNaomi NyongesaNo ratings yet

- Copeland 1968Document17 pagesCopeland 1968Aningtyas RatriNo ratings yet

- Hyperion Master Sheet NL 2013 FinalDocument22 pagesHyperion Master Sheet NL 2013 Finalannemarie van zadelhoffNo ratings yet

- Chapter 2 National IncomeDocument29 pagesChapter 2 National Incomeliyayudi0% (1)

- (ToA) Liabilities - Finance LeaseDocument15 pages(ToA) Liabilities - Finance Leaselooter198No ratings yet

- Understanding Accounting PrinciplesDocument35 pagesUnderstanding Accounting Principlessteven_c22003No ratings yet

- Business EnglishDocument29 pagesBusiness EnglishFabiana Costa100% (2)

- TRAINING ON AUDIT OF CFC ACCOUNTSDocument33 pagesTRAINING ON AUDIT OF CFC ACCOUNTSjaya prakashNo ratings yet

- 2 Conceptual FrameworkDocument29 pages2 Conceptual FrameworkNila FreesiaNo ratings yet

- ICAI - ICMAI - ICSI - Branch Accounting PDFDocument5 pagesICAI - ICMAI - ICSI - Branch Accounting PDFRowdy RahulNo ratings yet

- MaharlikaDocument4 pagesMaharlikaJamiel Andrei GarciaNo ratings yet

- Presentation of FS & Its' AuditingDocument27 pagesPresentation of FS & Its' AuditingTeamAudit Runner GroupNo ratings yet

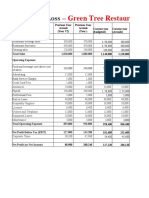

- Restaurant Financial HistoryDocument4 pagesRestaurant Financial HistoryStacy ParkerNo ratings yet

- Chapter 1Document9 pagesChapter 1craig52292No ratings yet

- Fringe Benefits in The PhilippinesDocument4 pagesFringe Benefits in The PhilippinesMarivie Uy100% (1)

- Adjustingtheaccount 1#$Document49 pagesAdjustingtheaccount 1#$mukesh697100% (1)

- Institute of Chartered Accountants of Bangladesh Class Test-1 (Knowledge Level (Accounting) ) About Financial Statements Sl. Topic List TextDocument41 pagesInstitute of Chartered Accountants of Bangladesh Class Test-1 (Knowledge Level (Accounting) ) About Financial Statements Sl. Topic List TextPonkoj Sarker TutulNo ratings yet

- Vouching & Verification: Ms. Fleur Dsouza Asst. Prof., BMS SIES CollegeDocument44 pagesVouching & Verification: Ms. Fleur Dsouza Asst. Prof., BMS SIES Collegesagar kasalkarNo ratings yet

- Step by Step TallyDocument39 pagesStep by Step TallyKakara Surya Nageswarao67% (3)

- Tax Alert - 2005 - FebDocument11 pagesTax Alert - 2005 - FebzhanleriNo ratings yet

- Accounting For non-CPADocument7 pagesAccounting For non-CPAJim OctavoNo ratings yet

- Model Answers to SAS ExamsDocument125 pagesModel Answers to SAS ExamsVishal GoelNo ratings yet

- Download More Slides, Ebook, Solutions and Test BankDocument17 pagesDownload More Slides, Ebook, Solutions and Test BankIndra Pramana50% (2)

- Cash Flow Problems and SolutionsDocument23 pagesCash Flow Problems and SolutionsSangetaSinghNo ratings yet

- Saet Work AnsDocument5 pagesSaet Work AnsSeanLejeeBajan89% (27)

- Acct Project Question 2Document14 pagesAcct Project Question 2grace100% (1)

- Chapter 16 Cash FlowsDocument4 pagesChapter 16 Cash Flowsjou20220354No ratings yet