You might also like

- Kurt Weill Songs PDFDocument3 pagesKurt Weill Songs PDFMatilda Jackson20% (25)

- BioPharma Case StudyDocument4 pagesBioPharma Case StudyNaman Chhaya100% (3)

- Summit Versus Calypso - The Big FightDocument4 pagesSummit Versus Calypso - The Big Fightsosn100% (2)

- Swaps Made Available To Trade: Fixed-to-Floating Interest Rate Swap (USD)Document3 pagesSwaps Made Available To Trade: Fixed-to-Floating Interest Rate Swap (USD)sosnNo ratings yet

- Product Eligibility USDDocument4 pagesProduct Eligibility USDnormanNo ratings yet

- Eris CME Deliverable Swaps.7Document24 pagesEris CME Deliverable Swaps.7sss1453No ratings yet

- Term Sheet Accrual Swap: Counterpart A PaysDocument3 pagesTerm Sheet Accrual Swap: Counterpart A PaysererererrrrrrNo ratings yet

- Ratchet Note 20041020Document3 pagesRatchet Note 20041020ererererrrrrrNo ratings yet

- BMS - International Finance Seme gdXuREtDocument4 pagesBMS - International Finance Seme gdXuREtishaNo ratings yet

- TVM Spreadsheet With Excel FunctionsDocument8 pagesTVM Spreadsheet With Excel FunctionsFaith AllenNo ratings yet

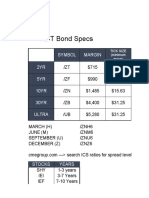

- ADT Bond Specs: T Symbol Margin 2YR 5YR 10YR 30YR UltraDocument4 pagesADT Bond Specs: T Symbol Margin 2YR 5YR 10YR 30YR UltraMax LiNo ratings yet

- CQG SymbolsDocument32 pagesCQG SymbolsCyril HoneyStars ChiaNo ratings yet

- Semester Registration Fees Semester Registration Fees Semester Registration Fees Semester Registration FeesDocument1 pageSemester Registration Fees Semester Registration Fees Semester Registration Fees Semester Registration FeesRam kripa shaNo ratings yet

- Calendar 06 26 2011Document5 pagesCalendar 06 26 2011Tarek NabilNo ratings yet

- Semester Registration Fees (Regular) Semester Registration Fees (Regular) Semester Registration Fees (Regular) Semester Registration Fees (Regular)Document2 pagesSemester Registration Fees (Regular) Semester Registration Fees (Regular) Semester Registration Fees (Regular) Semester Registration Fees (Regular)hemanta beheraNo ratings yet

- Global Edition: Interest-Rate Swaps, Caps, and FloorsDocument32 pagesGlobal Edition: Interest-Rate Swaps, Caps, and FloorskerenkangNo ratings yet

- Life Test CasesDocument23 pagesLife Test CasesPaul_Payne_9962No ratings yet

- Systematic Transfer Plan Enrollement Form (Please Fill in Block Letters)Document3 pagesSystematic Transfer Plan Enrollement Form (Please Fill in Block Letters)Ankur KaushikNo ratings yet

- Otc Sofr Swaps Product Overview 10 18Document12 pagesOtc Sofr Swaps Product Overview 10 18sholmstrNo ratings yet

- Downloads 090714125152 PDFDocument1 pageDownloads 090714125152 PDFLennyNo ratings yet

- Word Problems Interest Rate 27032021 074311pmDocument10 pagesWord Problems Interest Rate 27032021 074311pmsimraNo ratings yet

- PNB 250821Document1 pagePNB 250821P K MahatoNo ratings yet

- Fortune Guarantee Plus - 2021-03-26T180943.267Document3 pagesFortune Guarantee Plus - 2021-03-26T180943.267sk3146No ratings yet

- Interest Rate Risk ManagementDocument15 pagesInterest Rate Risk ManagementLiontiniNo ratings yet

- Daily Trading Stance - 2009-06-29Document2 pagesDaily Trading Stance - 2009-06-29Trading FloorNo ratings yet

- FFR 2 FormatDocument12 pagesFFR 2 FormatMukeshKataraNo ratings yet

- STP FormDocument1 pageSTP FormLamar Wealth solutionsNo ratings yet

- Portofolio BPFDocument33 pagesPortofolio BPFlae laNo ratings yet

- Multi Scheme SIP Facility Appl Form SIP With Micro SIP V 1Document6 pagesMulti Scheme SIP Facility Appl Form SIP With Micro SIP V 1rohan ladeNo ratings yet

- (KCP PAINAN) Pipeline Giro Dan Deposito Non PeroranganDocument5 pages(KCP PAINAN) Pipeline Giro Dan Deposito Non PeroranganJENNY ANDREANo ratings yet

- J Smythe Shell FileDocument2 pagesJ Smythe Shell FileAnkita DasNo ratings yet

- Amount at Year End (Double Investment) YEAR Initial Principal Amount at Year END (Double Investment) Year Initial PrincipalDocument2 pagesAmount at Year End (Double Investment) YEAR Initial Principal Amount at Year END (Double Investment) Year Initial PrincipalTunde AdeniyiNo ratings yet

- BERK FIT L05-1 IFI - Terminske Pog 20-05-12Document26 pagesBERK FIT L05-1 IFI - Terminske Pog 20-05-12Slobodanka AngelovaNo ratings yet

- Eco 2 D Chapter 3Document16 pagesEco 2 D Chapter 3PatriciaNo ratings yet

- KR Valuation 28 Sept 2019Document54 pagesKR Valuation 28 Sept 2019ket careNo ratings yet

- Form IiiDocument2 pagesForm Iiianon_370144No ratings yet

- YN YN YN Customer Id Customer Id YN: Personal and Employment DetailsDocument8 pagesYN YN YN Customer Id Customer Id YN: Personal and Employment Detailsmadhukar sahayNo ratings yet

- Icap Interest Rates DocsDocument34 pagesIcap Interest Rates DocsPuthpura PuthNo ratings yet

- SIP Investment With 15% Return: Monthly Investment Time Period Invested Amount Approx Return ValueDocument1 pageSIP Investment With 15% Return: Monthly Investment Time Period Invested Amount Approx Return ValueKamal RastogiNo ratings yet

- PROBLEM Set 3 AnswerDocument5 pagesPROBLEM Set 3 AnswerAmalia RosadiNo ratings yet

- Daily Trading Stance - 2010-01-08Document3 pagesDaily Trading Stance - 2010-01-08Trading FloorNo ratings yet

- Bonds - January 6 2017Document6 pagesBonds - January 6 2017Tiso Blackstar GroupNo ratings yet

- Jss Tripler SpreadsheetDocument25 pagesJss Tripler SpreadsheetReena Ravello Dela ViñaNo ratings yet

- ITR Form AY 20-21Document59 pagesITR Form AY 20-21Anurag Kumar ReloadedNo ratings yet

- RevisionInterestRates CircularDocument5 pagesRevisionInterestRates CircularK NkNo ratings yet

- Fortune Guarantee PlusDocument3 pagesFortune Guarantee PlusRenju GeorgeNo ratings yet

- MSFT Valuation 28 Sept 2019Document51 pagesMSFT Valuation 28 Sept 2019ket careNo ratings yet

- Informe Del Credit Suisse Sobre Oferta Argentina de DeudaDocument6 pagesInforme Del Credit Suisse Sobre Oferta Argentina de DeudaUrgente24No ratings yet

- Mon Pay 5pay Deferred 5 With Rop - With Ga & Death Benefit & Surrender ValueDocument3 pagesMon Pay 5pay Deferred 5 With Rop - With Ga & Death Benefit & Surrender ValueRamesh SharmaNo ratings yet

- Guidelines: TipsDocument28 pagesGuidelines: TipsAndi SedanaNo ratings yet

- Reserve Bank of India - NSDP Display 16 JunDocument1 pageReserve Bank of India - NSDP Display 16 JunSwatiNo ratings yet

- Trading Journal Template 04Document1 pageTrading Journal Template 04Mustakim HossainNo ratings yet

- LIC's New Money Back Plan - 20 Years (T-920) : Benefit IllustrationDocument3 pagesLIC's New Money Back Plan - 20 Years (T-920) : Benefit IllustrationSài TejaNo ratings yet

- Commodity Futures Trading Commission: Office of Public AffairsDocument3 pagesCommodity Futures Trading Commission: Office of Public AffairsMarketsWikiNo ratings yet

- Question Exercise 1 26102020Document2 pagesQuestion Exercise 1 26102020azwanni zulkarnainNo ratings yet

- Uttaranchal Gramin BankDocument1 pageUttaranchal Gramin BankcsashikumarNo ratings yet

- Pensford Rate Sheet - 02.25.13Document1 pagePensford Rate Sheet - 02.25.13Pensford FinancialNo ratings yet

- Dear Mr. Akhil E G: Key FeaturesDocument4 pagesDear Mr. Akhil E G: Key FeaturesAkhil GirijanNo ratings yet

- SIS With LSPO and Regular PayDocument3 pagesSIS With LSPO and Regular PayJyoti PandeyNo ratings yet

- S2-3 FisDocument37 pagesS2-3 FisMayank SinghNo ratings yet

- Bond Basics Forward Rate Agreements, Eurodollars, and HedgingDocument25 pagesBond Basics Forward Rate Agreements, Eurodollars, and HedgingZhuangKaKitNo ratings yet

- Krakatau A CGAR BUMN DupontDocument27 pagesKrakatau A CGAR BUMN DupontFirdausNo ratings yet

- Economic and Business Forecasting: Analyzing and Interpreting Econometric ResultsFrom EverandEconomic and Business Forecasting: Analyzing and Interpreting Econometric ResultsNo ratings yet

- FIX-5.0 SP2 VOL-1 W Errata 20110818Document158 pagesFIX-5.0 SP2 VOL-1 W Errata 20110818sosnNo ratings yet

- ESMA MiFIDII MiFIR Transactionreporting Refdata Nov20Document15 pagesESMA MiFIDII MiFIR Transactionreporting Refdata Nov20sosnNo ratings yet

- Swaps Made Available To Trade: Fixed-to-Floating Interest Rate Swap (USD)Document3 pagesSwaps Made Available To Trade: Fixed-to-Floating Interest Rate Swap (USD)sosnNo ratings yet

- Agile TestingDocument4 pagesAgile Testingsosn100% (1)

- Agile TestingDocument4 pagesAgile Testingsosn100% (1)

- Interest Rate Derivatives - An Indispensable Prerequisite: Monika GoelDocument5 pagesInterest Rate Derivatives - An Indispensable Prerequisite: Monika GoelsosnNo ratings yet

- Africa Mining 2012 AgendaDocument8 pagesAfrica Mining 2012 AgendaJuan Luis BerrioNo ratings yet

- PBL20 Project Compal Confidential: LA-6772P Schematic REV 1.0Document45 pagesPBL20 Project Compal Confidential: LA-6772P Schematic REV 1.0Ramdas KambleNo ratings yet

- The Effect of Globalisation On A Hotels Marketing StrategyDocument10 pagesThe Effect of Globalisation On A Hotels Marketing StrategyAslam Abdullah MarufNo ratings yet

- Reservists Retirees Affairs ProgramDocument35 pagesReservists Retirees Affairs ProgramSweet Holy Jean DamasoleNo ratings yet

- 73 Disinfecting Acid BR Cleaner Sell Sheet PDFDocument2 pages73 Disinfecting Acid BR Cleaner Sell Sheet PDFMarie Kris NogaNo ratings yet

- Roble Arrastre Vs VillaflorDocument16 pagesRoble Arrastre Vs VillaflorMyra MyraNo ratings yet

- Configuration For NeoBip - (Black) V1.1 BF 30STDocument1 pageConfiguration For NeoBip - (Black) V1.1 BF 30STTECHMED REPAIRS TECHMED SALESNo ratings yet

- Ls 33600 DatasheetDocument2 pagesLs 33600 DatasheetSilviu TeodoruNo ratings yet

- 338-Article Text-909-1-10-20180827Document11 pages338-Article Text-909-1-10-20180827Gil Randey Anak'e Mama'keNo ratings yet

- Measuring Temperature - Platinum Resistance ThermometersDocument3 pagesMeasuring Temperature - Platinum Resistance Thermometersdark*nightNo ratings yet

- BiyDaalt2+OpenMP - Ipynb - ColaboratoryDocument3 pagesBiyDaalt2+OpenMP - Ipynb - ColaboratoryAngarag G.No ratings yet

- Making Sense of VoluDocument44 pagesMaking Sense of VoluImprovingSupportNo ratings yet

- Ting Ho, Jr. v. Teng Gui, GR 130115, July 16, 2008, 558 SCRA 421Document1 pageTing Ho, Jr. v. Teng Gui, GR 130115, July 16, 2008, 558 SCRA 421Gia DimayugaNo ratings yet

- Titus Villanueva vs. Emma Rosqueta: G.R. No. 180764, January 19, 2010Document3 pagesTitus Villanueva vs. Emma Rosqueta: G.R. No. 180764, January 19, 2010Raziel Xyrus FloresNo ratings yet

- Gpcdoc Tds Darina R 2Document2 pagesGpcdoc Tds Darina R 2nutchai2538No ratings yet

- Datasheet Solis 110K 5GDocument2 pagesDatasheet Solis 110K 5GAneeq TahirNo ratings yet

- AGRD04B-15 Guide To Road Design Part 4B Roundabouts Ed3.1Document97 pagesAGRD04B-15 Guide To Road Design Part 4B Roundabouts Ed3.1fbturaNo ratings yet

- Attach and DetachDocument2 pagesAttach and DetachMaksRockNo ratings yet

- Info Lec 3Document2 pagesInfo Lec 3mostafa abdoNo ratings yet

- Application LetterDocument5 pagesApplication Lettersdguillermo928No ratings yet

- (IBM) System Storage SAN Volume Controller Version 6.4.0Document350 pages(IBM) System Storage SAN Volume Controller Version 6.4.0hiehie272No ratings yet

- Operation Manual: Inmarsat-C Mobile Earth StationDocument203 pagesOperation Manual: Inmarsat-C Mobile Earth StationPaul Lucian VentelNo ratings yet

- International Business DirectoryDocument1 pageInternational Business DirectoryIvy Michelle HabagatNo ratings yet

- Industrial Visit On SEBIDocument4 pagesIndustrial Visit On SEBIDrPreeti JindalNo ratings yet

- Unit 4 Reading 1 1Document1 pageUnit 4 Reading 1 1601-24-Narit NitjapanNo ratings yet

- Meidner (1992) - Rise and Fall of The Swedish ModelDocument13 pagesMeidner (1992) - Rise and Fall of The Swedish ModelmarceloscarvalhoNo ratings yet

- HydraulicDocument10 pagesHydraulicDewan VidanageNo ratings yet

- Gitam UniversityDocument100 pagesGitam UniversityvicterpaulNo ratings yet