You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5810)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Malcolm & Marie ScriptDocument92 pagesMalcolm & Marie ScriptTHROnline94% (33)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- ConjunctionDocument15 pagesConjunctionAlfian MilitanNo ratings yet

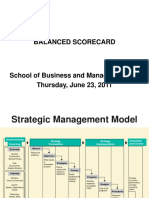

- Balanced Scorecard & EVA - June 23, 2011Document47 pagesBalanced Scorecard & EVA - June 23, 2011aditprasNo ratings yet

- Gilmore Girls 1x01 - PilotDocument57 pagesGilmore Girls 1x01 - PilotRenan Bianco100% (2)

- Menu in A Restaurant Ordering FoodDocument3 pagesMenu in A Restaurant Ordering FoodRoberto C Navarro GNo ratings yet

- Murdoch Books Catalogue 2014-15Document113 pagesMurdoch Books Catalogue 2014-15Allen & Unwin100% (5)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Skin - Roald DahlDocument2 pagesSkin - Roald DahlMax Lee IsboredNo ratings yet

- The Royal Bank of Scotland GroupDocument2 pagesThe Royal Bank of Scotland GroupaditprasNo ratings yet

- Food, Flavour&Ingredients Outlook2012Document140 pagesFood, Flavour&Ingredients Outlook2012Vijita Jain100% (1)

- Maximizing Your Return On PeopleDocument2 pagesMaximizing Your Return On Peopleaditpras100% (1)

- Riza Zakaria: Startup Interpreneurship ProgramDocument1 pageRiza Zakaria: Startup Interpreneurship ProgramaditprasNo ratings yet

- SassDocument17 pagesSassaditprasNo ratings yet

- Laysha Fancam - I'M Coming PMV XXX Part 1 of 3 - by FapmusicDocument1 pageLaysha Fancam - I'M Coming PMV XXX Part 1 of 3 - by FapmusicaditprasNo ratings yet

- Ethics and ReputationDocument1 pageEthics and ReputationaditprasNo ratings yet

- Co Working Space KerangkaDocument1 pageCo Working Space KerangkaaditprasNo ratings yet

- UtiliarismDocument1 pageUtiliarismaditprasNo ratings yet

- The Financial Sector and The Economy: - Walter BagehotDocument62 pagesThe Financial Sector and The Economy: - Walter BagehotaditprasNo ratings yet

- Case: Monte Carlo SimulationDocument3 pagesCase: Monte Carlo SimulationaditprasNo ratings yet

- Prof. Jann Hidajat Tjakratmadja: Executive BandungDocument17 pagesProf. Jann Hidajat Tjakratmadja: Executive BandungaditprasNo ratings yet

- The Asian Financial Crisi Indonesia and The Currency Board ProposalDocument25 pagesThe Asian Financial Crisi Indonesia and The Currency Board ProposaladitprasNo ratings yet

- Permintaan Harga Pendapatan: Regression StatisticsDocument10 pagesPermintaan Harga Pendapatan: Regression StatisticsaditprasNo ratings yet

- Melbourne Trip Itinerary 2019 (311019)Document13 pagesMelbourne Trip Itinerary 2019 (311019)dummy levupaccNo ratings yet

- Original Gaskets Jointings GuideDocument52 pagesOriginal Gaskets Jointings GuideSUBHOMOYNo ratings yet

- Bai See CeremonyDocument7 pagesBai See Ceremonytkaye77320% (1)

- Nestle Ice CreamDocument9 pagesNestle Ice CreamaniNo ratings yet

- BATARA K. - Organizing Meal PreparationDocument4 pagesBATARA K. - Organizing Meal PreparationMark Lester TanguanNo ratings yet

- Placement Test For UndergraduateDocument7 pagesPlacement Test For Undergraduateဂု ရု ကြီးNo ratings yet

- Maresca Kypn HandoutDocument2 pagesMaresca Kypn Handoutapi-266549998No ratings yet

- Food & Beverage Information Project Markets Stream - SingaporeDocument25 pagesFood & Beverage Information Project Markets Stream - SingaporecoriolisresearchNo ratings yet

- 1 Quarterly Examination: Science 6Document16 pages1 Quarterly Examination: Science 6katherine corveraNo ratings yet

- Lemons, Lemons and More Lemons: ObjectivesDocument2 pagesLemons, Lemons and More Lemons: ObjectivesZNo ratings yet

- How Often Does He See His Grandmother. She Sometimes Visits Her GrandmotherDocument11 pagesHow Often Does He See His Grandmother. She Sometimes Visits Her GrandmotherFredy Akenaton ArroyoNo ratings yet

- Surrender by Elana JohnsonDocument98 pagesSurrender by Elana JohnsonSimon and SchusterNo ratings yet

- Subo Pvt. Ltd. Co.: Innovation CIA B PlanDocument36 pagesSubo Pvt. Ltd. Co.: Innovation CIA B PlankhantahavarNo ratings yet

- Dabur Real JuicesDocument7 pagesDabur Real Juicestushar jainNo ratings yet

- Paruolo, E.translating Food in Children's LiteratureDocument22 pagesParuolo, E.translating Food in Children's LiteratureBarış TaşkınNo ratings yet

- Seikima II Akon 21 DallasDocument4 pagesSeikima II Akon 21 DallasCarolina Villena100% (1)

- Ending Jim Crow in America's RestaurantsDocument36 pagesEnding Jim Crow in America's Restaurantsmaria-136299100% (1)

- IntroductionDocument4 pagesIntroductionCeyah Nurr0% (1)

- DigitalShowroom Banned ProductsDocument2 pagesDigitalShowroom Banned ProductsFlexiAds IndiaNo ratings yet

- Manual Analysis Methods For The Brewery Industry Prove 05 2018Document118 pagesManual Analysis Methods For The Brewery Industry Prove 05 2018Ivana NikolicNo ratings yet

- Bdi 03-2 20230330Document302 pagesBdi 03-2 20230330Matema1 - Prof. Marcos José NovakoskiNo ratings yet

- Irish CuisineDocument6 pagesIrish CuisineJohn SmithNo ratings yet

- Clarification of Sugarcane Juice For Syrup ProductDocument7 pagesClarification of Sugarcane Juice For Syrup ProductAnghelo AlcaldeNo ratings yet