You might also like

- Let's Practise: Maths Workbook Coursebook 4From EverandLet's Practise: Maths Workbook Coursebook 4No ratings yet

- Additional Mathematics Form 5 ProjectDocument34 pagesAdditional Mathematics Form 5 ProjectphosphosaurusNo ratings yet

- Additional Mathematics Form 5 Project WoDocument34 pagesAdditional Mathematics Form 5 Project WoTANG POH YAP KPM-GuruNo ratings yet

- Practical System ArchitectureDocument8 pagesPractical System Architectureh00444687No ratings yet

- Aaliya Ali Add Maths SBA 2021Document40 pagesAaliya Ali Add Maths SBA 2021AALIYA ALINo ratings yet

- Resource 5e85c2740f5e5963197435 PDFDocument133 pagesResource 5e85c2740f5e5963197435 PDFTooniNo ratings yet

- Risk Assessment of The City Bank Limited.Document15 pagesRisk Assessment of The City Bank Limited.MdRuhulRAfinNo ratings yet

- 2020 - Class 10 - Revision - Q - For StudentsDocument4 pages2020 - Class 10 - Revision - Q - For StudentsCartieNo ratings yet

- Handstar Case AnalysisDocument4 pagesHandstar Case AnalysisarchaonscribdNo ratings yet

- PPME 102 Assignment Due 23rd deDocument9 pagesPPME 102 Assignment Due 23rd desipanjegivenNo ratings yet

- Ued 102 E-PortfolioDocument16 pagesUed 102 E-Portfoliosofiafarhanis1978No ratings yet

- Memo Template 1 1Document5 pagesMemo Template 1 1api-673590583No ratings yet

- Batch14 Contact2 OM Assign39Document4 pagesBatch14 Contact2 OM Assign39pranjal92pandeyNo ratings yet

- FIN3120 Exam Paper May 2022Document4 pagesFIN3120 Exam Paper May 2022Risvana RizzNo ratings yet

- Module 9 Time Value of Money: Present Value (PV) - This Is Your Current Starting Amount. It Is TheDocument4 pagesModule 9 Time Value of Money: Present Value (PV) - This Is Your Current Starting Amount. It Is ThePaul Anthony AspuriaNo ratings yet

- Report MST699 CS241Document18 pagesReport MST699 CS241hazirah azaharNo ratings yet

- Rating Scale Evaluation Form For FS Students Revised 2Document3 pagesRating Scale Evaluation Form For FS Students Revised 2Apollos Jason S. OjaoNo ratings yet

- Group 3 MGT314 Case StudyDocument8 pagesGroup 3 MGT314 Case StudyMunjaber Kashem PrantoNo ratings yet

- Project Report On KKKKKKDocument16 pagesProject Report On KKKKKKAnupam GhoshNo ratings yet

- It or Make A Copy To Your Own Google Drive To Edit ItDocument10 pagesIt or Make A Copy To Your Own Google Drive To Edit Itusi tausiahNo ratings yet

- It or Make A Copy To Your Own Google Drive To Edit ItDocument10 pagesIt or Make A Copy To Your Own Google Drive To Edit Itusi tausiahNo ratings yet

- Founders Data AnalysisDocument18 pagesFounders Data AnalysisMaira Rixvi50% (2)

- BS Architecture & BS Environmental Planning Graduate School For Architecture Research Center For The Design and Built Environment StudiesDocument63 pagesBS Architecture & BS Environmental Planning Graduate School For Architecture Research Center For The Design and Built Environment StudiesJoshua RodilNo ratings yet

- Assignment Module-9 Coefficient of CorrelationDocument4 pagesAssignment Module-9 Coefficient of CorrelationFranchesca CuraNo ratings yet

- Session 7.4 Present Value Formula in Excel - AsyncDocument12 pagesSession 7.4 Present Value Formula in Excel - AsyncAnyone SomeoneNo ratings yet

- AFM Class Notes PDFDocument154 pagesAFM Class Notes PDFSiddharth NarayananNo ratings yet

- Annuities K. RaghunandanDocument18 pagesAnnuities K. RaghunandanShubhankar ShuklaNo ratings yet

- A2a - 4 - Present Value Formula in ExcelDocument12 pagesA2a - 4 - Present Value Formula in ExcelShubhankar ShuklaNo ratings yet

- Section 2 0 Current Carrying Capacity of BusbarsDocument13 pagesSection 2 0 Current Carrying Capacity of BusbarsCarlos ChalcoNo ratings yet

- Key AnswersDocument7 pagesKey AnswersMaybelyn de los ReyesNo ratings yet

- Mathematics - WS - 4 (Answer Key)Document2 pagesMathematics - WS - 4 (Answer Key)William LeonardNo ratings yet

- Online EndSemExam Stats - 20apr21Document4 pagesOnline EndSemExam Stats - 20apr21Tanuj SinghNo ratings yet

- Business Information Systems Discipline Assignment Submission Form Module: MS802Document14 pagesBusiness Information Systems Discipline Assignment Submission Form Module: MS802anirudh kashyapNo ratings yet

- Practice Problems, CH 9 10 (MCQ)Document5 pagesPractice Problems, CH 9 10 (MCQ)scridNo ratings yet

- Rounding To The Nearest Whole NumberDocument4 pagesRounding To The Nearest Whole NumbersghwsryNo ratings yet

- Las.m5. q2w1 Melc3 FinalDocument7 pagesLas.m5. q2w1 Melc3 FinalMr. BatesNo ratings yet

- Case Analysis StudyDocument15 pagesCase Analysis StudyVyl CebrerosNo ratings yet

- Population: Variables: Parameters: SampleDocument15 pagesPopulation: Variables: Parameters: SampleAbdu AbdoulayeNo ratings yet

- Edited - L. - Ass. - Mod. - 9-11. - DocxDocument18 pagesEdited - L. - Ass. - Mod. - 9-11. - DocxArboleda, Mark Kenneth F.No ratings yet

- TRADE PROJECT JacintaDocument34 pagesTRADE PROJECT Jacintareuben simiyuNo ratings yet

- Group I - Day CareDocument48 pagesGroup I - Day CareMaria SoomroNo ratings yet

- Eleot Technical BriefDocument17 pagesEleot Technical BriefMohamed ElsharkawyNo ratings yet

- APM Class Notes Sep 2021 As at 24 February 2021 FINALDocument156 pagesAPM Class Notes Sep 2021 As at 24 February 2021 FINAL3bbas Al-3bbasNo ratings yet

- Employee EngagementDocument100 pagesEmployee EngagementPankaj PawarNo ratings yet

- Internship Electrical Form-1Document2 pagesInternship Electrical Form-1YousafzaiNo ratings yet

- Dseu HandbookDocument77 pagesDseu Handbookwejepe1452No ratings yet

- Final Artifacts Data Driven II JGDocument5 pagesFinal Artifacts Data Driven II JGapi-634262150No ratings yet

- Practice ProblemsDocument3 pagesPractice ProblemsVibhuti BatraNo ratings yet

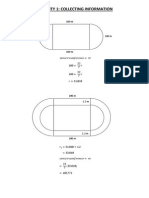

- Activity 1: Collecting InformationDocument15 pagesActivity 1: Collecting InformationVaradan K RajendranNo ratings yet

- Data Mining PortfolioDocument19 pagesData Mining PortfolioJohnMaynardNo ratings yet

- Assessment 2Document11 pagesAssessment 2Researchpro GlobalNo ratings yet

- Numeracy Assessment Tool (Numat) S.Y: 2021 - 2022 Grade 4 Task 1: Number IdentificationDocument4 pagesNumeracy Assessment Tool (Numat) S.Y: 2021 - 2022 Grade 4 Task 1: Number IdentificationABEGAIL ALCANTARA100% (4)

- The BAT Case-: Answer 1) Givens: Calling Period 6 Hours Per Weekday Arrival Rate 22.5 Per Hour Avg TimeDocument4 pagesThe BAT Case-: Answer 1) Givens: Calling Period 6 Hours Per Weekday Arrival Rate 22.5 Per Hour Avg TimeMine SayracNo ratings yet

- ACABAR-Business Plan-FinancialsDocument7 pagesACABAR-Business Plan-FinancialsSolomon KiyagaNo ratings yet

- Mathematics 5 Q2 - M7 For PrintingDocument13 pagesMathematics 5 Q2 - M7 For PrintingKHENLAN MATANo ratings yet

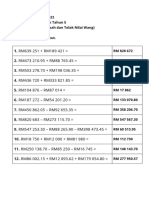

- Tambah Dan Tolak Wang Tahun 5 2022Document9 pagesTambah Dan Tolak Wang Tahun 5 2022Clara Doo Siew WeeNo ratings yet

- C02 BUAD555 DSB BTCN ChienTM ENDocument10 pagesC02 BUAD555 DSB BTCN ChienTM ENTruong Minh ChienNo ratings yet

- STPCalculator8 - 27 - 2021 3 - 30 - 42 PMDocument7 pagesSTPCalculator8 - 27 - 2021 3 - 30 - 42 PMipo formNo ratings yet

- Planning Planers Repeat CaseDocument9 pagesPlanning Planers Repeat CaseMayur MahajanNo ratings yet

- Kyle Ramsay IADocument20 pagesKyle Ramsay IANick FullerNo ratings yet

- Practical TemplateDocument4 pagesPractical TemplateMin KookieNo ratings yet

- 4.is It Suitable For Diagnosing Hypoglycemia 4mDocument2 pages4.is It Suitable For Diagnosing Hypoglycemia 4mMin KookieNo ratings yet

- Additional Mathematics Project Work 2013 StatisticsDocument31 pagesAdditional Mathematics Project Work 2013 StatisticsMin KookieNo ratings yet

- NO ContentDocument33 pagesNO ContentMin KookieNo ratings yet

- SmashDocument1 pageSmashMin KookieNo ratings yet

- SmashDocument1 pageSmashMin KookieNo ratings yet

- MDocument2 pagesMMin KookieNo ratings yet

- Assessment of Financial Statement of Nestle IndiaDocument16 pagesAssessment of Financial Statement of Nestle IndiaDivyasreeNo ratings yet

- Interest Rate Risk AuditDocument4 pagesInterest Rate Risk AuditpascaruionNo ratings yet

- PADD Loan Calculator Tool: Payment Amount (Monthly) : $ 6,055.81Document1 pagePADD Loan Calculator Tool: Payment Amount (Monthly) : $ 6,055.81c_b_umashankarNo ratings yet

- Study Unit 5 - Spreadsheet Formulas and FunctionsDocument46 pagesStudy Unit 5 - Spreadsheet Formulas and FunctionsShane GowerNo ratings yet

- Must Do Sample Paper Solved and Un Solved With Pre Board PaperDocument47 pagesMust Do Sample Paper Solved and Un Solved With Pre Board PaperBhangu PreetNo ratings yet

- Subsale (Part 2)Document34 pagesSubsale (Part 2)Alisya TajularifinNo ratings yet

- Field Warehouse Receipt FinancingDocument18 pagesField Warehouse Receipt FinancingYashveer ChoudharyNo ratings yet

- NHB Guidelines On RMLDocument8 pagesNHB Guidelines On RMLsreejit.mohanty4016No ratings yet

- Alifia Farradita Fedli / 119410006 1.2. The Accumulation and Amount FunctionDocument9 pagesAlifia Farradita Fedli / 119410006 1.2. The Accumulation and Amount Functionfarra dita fedliNo ratings yet

- Final PartDocument52 pagesFinal PartFauzul Azim100% (1)

- Sworn Statement of Assets, Liabilities and Net Worth (Saln) : Joint Filing Separate Filing Not ApplicableDocument4 pagesSworn Statement of Assets, Liabilities and Net Worth (Saln) : Joint Filing Separate Filing Not ApplicableDanivieNo ratings yet

- Chapter 4 Capitalized CostDocument11 pagesChapter 4 Capitalized CostUpendra ReddyNo ratings yet

- Fixed Income - AnswersDocument6 pagesFixed Income - AnswersNeerajNo ratings yet

- Mathematics of Finance 8th Edition Brown Test BankDocument112 pagesMathematics of Finance 8th Edition Brown Test BankLarryHicksetdrb100% (18)

- 14 Comm 308 Final Exam (Summer 2, 2012) SolutionsDocument18 pages14 Comm 308 Final Exam (Summer 2, 2012) SolutionsAfafe ElNo ratings yet

- Konkan RailwayDocument20 pagesKonkan Railwayashutosh1202No ratings yet

- Mas DRILL 2Document10 pagesMas DRILL 2ROMAR A. PIGANo ratings yet

- Cooperative Movements in India: CommentaryDocument3 pagesCooperative Movements in India: Commentarysivaramanlb100% (1)

- GR 182722Document2 pagesGR 182722Jenny Diaz100% (1)

- UP LAE Review 09 Final Diagnostic Exam Sans AbstractDocument47 pagesUP LAE Review 09 Final Diagnostic Exam Sans AbstractVen Mark Borbon100% (3)

- 2016 No Bull Review AP Econ (Published)Document196 pages2016 No Bull Review AP Econ (Published)ManasNo ratings yet

- Tender Document GSM1Document78 pagesTender Document GSM1Varsha Vaishali KotharyNo ratings yet

- Education Loans For Higher StudiesDocument7 pagesEducation Loans For Higher StudiesSREYANo ratings yet

- ANSI STD C57.120-1991 (IEEE Loss Evaluation Guide ForDocument28 pagesANSI STD C57.120-1991 (IEEE Loss Evaluation Guide Forsorry2qaz100% (1)

- Gumabon V PNBDocument5 pagesGumabon V PNBGennard Michael Angelo AngelesNo ratings yet

- SCM-4-Master Budget PDFDocument21 pagesSCM-4-Master Budget PDFChin FiguraNo ratings yet

- Cash Management-ProblemsDocument2 pagesCash Management-ProblemsNagma ParmarNo ratings yet

- Equipment Economics Ch04DDocument12 pagesEquipment Economics Ch04DMahmoud A. YousefNo ratings yet

- c6 Question BankDocument25 pagesc6 Question BankWaseem Ahmad QurashiNo ratings yet

- Statement 602048 45624011 12 Jan 2024Document4 pagesStatement 602048 45624011 12 Jan 2024aemeraziz1No ratings yet