You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- BankruptcyDocument56 pagesBankruptcycharlesayres83100% (1)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Credit Risk - Standardised ApproachDocument78 pagesCredit Risk - Standardised Approachleyla_lit100% (2)

- Insurance Broking BusinessDocument56 pagesInsurance Broking Businesshardikpawar100% (4)

- Questions On Noting & DraftingDocument1 pageQuestions On Noting & DraftingKuldeepDeswal100% (1)

- 16 Gaisano Cagayan Inc. vs. Insurance Company of North America G.R. No. 147839 June 8 2006 ScraDocument17 pages16 Gaisano Cagayan Inc. vs. Insurance Company of North America G.R. No. 147839 June 8 2006 ScraJNo ratings yet

- d.2.4.1. Geagonia vs. Court of Appeals PDFDocument16 pagesd.2.4.1. Geagonia vs. Court of Appeals PDFShien TumalaNo ratings yet

- 16 Gaisano Cagayan Inc. vs. Insurance Company of North America G.R. No. 147839 June 8 2006Document6 pages16 Gaisano Cagayan Inc. vs. Insurance Company of North America G.R. No. 147839 June 8 2006JNo ratings yet

- 10 Enriquez vs. Sun Life Insurance of Canada G.R. No. 15895 Nov. 29 1920 ScraDocument5 pages10 Enriquez vs. Sun Life Insurance of Canada G.R. No. 15895 Nov. 29 1920 ScraJNo ratings yet

- 14 Geagonia vs. CA G.R. No. 114427 February 6 1995Document5 pages14 Geagonia vs. CA G.R. No. 114427 February 6 1995JNo ratings yet

- 08 Federal Express Corporation vs. American Home Assurance Company and Phil Am Insurance Company Inc. PDFDocument8 pages08 Federal Express Corporation vs. American Home Assurance Company and Phil Am Insurance Company Inc. PDFJNo ratings yet

- 09-Eternal Gardens Memorial Park Corporation vs. Phil. American Life Insurance Co., GR No. 166245, 09 April 2008 - EscraDocument13 pages09-Eternal Gardens Memorial Park Corporation vs. Phil. American Life Insurance Co., GR No. 166245, 09 April 2008 - EscraJNo ratings yet

- 07 Manila Mahogany vs. CA 154 SCRA 650 ScraDocument6 pages07 Manila Mahogany vs. CA 154 SCRA 650 ScraJNo ratings yet

- 06-Gulf Resorts Inc. vs. Philippine Charter Insurance Corp. GR No. 155167, 16 May 2005Document9 pages06-Gulf Resorts Inc. vs. Philippine Charter Insurance Corp. GR No. 155167, 16 May 2005JNo ratings yet

- 08 Federal Express Corporation vs. American Home Assurance Company and Phil Am Insurance Company Inc. G.R. No. 150094 18 August 2004 ScraDocument9 pages08 Federal Express Corporation vs. American Home Assurance Company and Phil Am Insurance Company Inc. G.R. No. 150094 18 August 2004 ScraJNo ratings yet

- 07 Manila Mahogany vs. CA 154 SCRA 650Document2 pages07 Manila Mahogany vs. CA 154 SCRA 650JNo ratings yet

- 05-Fortune Insurance and Surety Co., Inc. vs. CA (244 SCRA 308) - EscraDocument12 pages05-Fortune Insurance and Surety Co., Inc. vs. CA (244 SCRA 308) - EscraJNo ratings yet

- 09 Pimentel v. Office of The Executive Secretary, G.R. No. 158088, July 6, 2005 - ScraDocument16 pages09 Pimentel v. Office of The Executive Secretary, G.R. No. 158088, July 6, 2005 - ScraJNo ratings yet

- Republic of The Philippines Manila Third DivisionDocument3 pagesRepublic of The Philippines Manila Third DivisionJNo ratings yet

- 04-Philamcare Health Systems Inc. vs. CA (379 SCRA 356) - EscraDocument12 pages04-Philamcare Health Systems Inc. vs. CA (379 SCRA 356) - EscraJNo ratings yet

- 05-Fortune Insurance and Surety Co., Inc. vs. CA (244 SCRA 308)Document4 pages05-Fortune Insurance and Surety Co., Inc. vs. CA (244 SCRA 308)JNo ratings yet

- 03-Rizal Surety and Insurance Co. vs. CA (336 SCRA 12)Document4 pages03-Rizal Surety and Insurance Co. vs. CA (336 SCRA 12)JNo ratings yet

- 01-White Gold Marine Services vs. Pioneer Insurance, Et Al. (GR No. 154514, 28 July 2005) - EscraDocument10 pages01-White Gold Marine Services vs. Pioneer Insurance, Et Al. (GR No. 154514, 28 July 2005) - EscraJ100% (1)

- 02-Verendia vs. CA (217 SCRA 417) - EscraDocument8 pages02-Verendia vs. CA (217 SCRA 417) - EscraJNo ratings yet

- 10 Saguisag v. Executive Secretary, G.R. No. 212426, January 12, 2016 - ScraDocument299 pages10 Saguisag v. Executive Secretary, G.R. No. 212426, January 12, 2016 - ScraJNo ratings yet

- 09 Pimentel v. Office of The Executive Secretary, G.R. No. 158088, July 6, 2005Document12 pages09 Pimentel v. Office of The Executive Secretary, G.R. No. 158088, July 6, 2005JNo ratings yet

- 08 Tanada v. Angara 1997 - ScraDocument60 pages08 Tanada v. Angara 1997 - ScraJNo ratings yet

- 07 Gonzales v. Hechanova, G.R. No. L-21897, October 2, 1963 - ScraDocument22 pages07 Gonzales v. Hechanova, G.R. No. L-21897, October 2, 1963 - ScraJNo ratings yet

- 06 Ichong v. Hernandez, G.R. No. L-7995 1957Document10 pages06 Ichong v. Hernandez, G.R. No. L-7995 1957JNo ratings yet

- 5th - Ganga - Term 1 - TM - 5-In-1Document312 pages5th - Ganga - Term 1 - TM - 5-In-1Thirumanthira YogaNo ratings yet

- Print Order # 100272865Document1 pagePrint Order # 100272865sayan biswasNo ratings yet

- Cancellation of Real Estate MortgageDocument2 pagesCancellation of Real Estate MortgageapbacaniNo ratings yet

- Objectives of AuditDocument4 pagesObjectives of AuditSana ShafiqNo ratings yet

- A Study On Various Deposit Schemes, Retail Banking and Internet Banking With Reference To Syndicate BankDocument67 pagesA Study On Various Deposit Schemes, Retail Banking and Internet Banking With Reference To Syndicate BanklalsinghNo ratings yet

- Banking System in CambodiaDocument41 pagesBanking System in CambodiaYuthea Em100% (3)

- ANK Redit Esearch: Eekly Atings ISTDocument118 pagesANK Redit Esearch: Eekly Atings ISTegutman1No ratings yet

- Financial Performance of Commercial BanksDocument34 pagesFinancial Performance of Commercial BanksbagyaNo ratings yet

- Credit CardDocument15 pagesCredit Cardsrdagpnt100% (1)

- AsdadasDocument13 pagesAsdadasSwindlerNo ratings yet

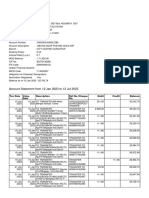

- Account Statement From 12 Jan 2023 To 12 Jul 2023Document10 pagesAccount Statement From 12 Jan 2023 To 12 Jul 2023SouravDeyNo ratings yet

- Definition and Explanation:: (1) - Adjusting Entries That Convert Assets To ExpensesDocument8 pagesDefinition and Explanation:: (1) - Adjusting Entries That Convert Assets To ExpensesKae Abegail GarciaNo ratings yet

- Summary of Preferred Hedge Fund Terms: OverviewDocument4 pagesSummary of Preferred Hedge Fund Terms: OverviewsmasarikNo ratings yet

- Membership Application FormDocument1 pageMembership Application FormProutist Universal MaltaNo ratings yet

- Asit Baran Pati MoneyControlDocument4 pagesAsit Baran Pati MoneyControlShibnath SadhukhanNo ratings yet

- Vip ReceiptDocument16 pagesVip Receiptvanita kunnoNo ratings yet

- Account StatementDocument12 pagesAccount StatementPRABHAKAR REDDY TBSF - TELANGANANo ratings yet

- (EDUCBA) Finance Analyst Courses PDFDocument12 pages(EDUCBA) Finance Analyst Courses PDFMudit NawaniNo ratings yet

- Marketing Strategy of Bharti Axa Life Insurance - 191468884Document36 pagesMarketing Strategy of Bharti Axa Life Insurance - 191468884Jammu & kashmir story catcherNo ratings yet

- Merger and Acquisition in Bank Sector in IndiaDocument63 pagesMerger and Acquisition in Bank Sector in IndiaOmkar Chavan0% (1)

- Alpha PDFDocument13 pagesAlpha PDFWARWICKJNo ratings yet

- Project by Vidhi Seth and Nandini KediaDocument19 pagesProject by Vidhi Seth and Nandini KediavidhisethNo ratings yet

- Industry Profile: Banking Sector in IndiaDocument15 pagesIndustry Profile: Banking Sector in Indiasri1031No ratings yet

- Mande Morisho What Do You Know About Depository InstitutionsDocument2 pagesMande Morisho What Do You Know About Depository InstitutionsMand'e MorishoNo ratings yet

- AICPA - Develops Standards For Audits ofDocument3 pagesAICPA - Develops Standards For Audits ofAngela PaduaNo ratings yet

- Executive Order No 172Document9 pagesExecutive Order No 172Merceditas PlamerasNo ratings yet